|

市场调查报告书

商品编码

1684715

汽车变数排气量帮浦市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Variable Displacement Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

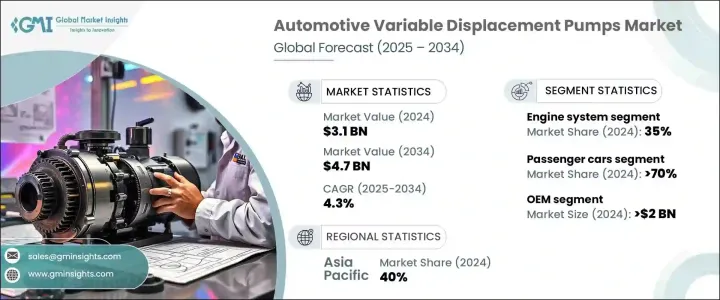

2024 年全球汽车可变排气量帮浦市场价值 31 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 4.3%。世界各国政府都在执行更严格的法律,以降低碳足迹并推广节能交通,迫使汽车製造商将先进技术融入他们的汽车中。变数排气量帮浦正在成为关键的解决方案,可优化引擎性能、提高燃油经济性并最大限度地减少能量损失。

随着汽车製造商专注于实现永续发展目标,混合动力和省油汽车越来越受欢迎,进一步推动了对这些系统的需求。消费者越来越重视燃油经济性,这使得製造商必须采用符合监管标准的节能组件。能源优化的需求也加速了汽车设计的创新,鼓励製造商探索提高性能的新方法,同时满足全球永续发展基准。随着燃料价格的上涨以及混合动力和电动车的普及,可变排气量帮浦将在现代汽车工程中发挥关键作用。对燃油效率的持续重视为行业参与者提供了巨大的成长机会,确保了未来几年对这些帮浦的持续市场需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 31亿美元 |

| 预测值 | 47亿美元 |

| 复合年增长率 | 4.3% |

市场按车辆类型细分为乘用车和商用车,其中乘用车在 2024 年占总市场份额的 70%。可变排量泵浦对于优化混合动力汽车性能、减少非液压应用中不必要的流体排气量以及增强整体燃料管理至关重要。这些泵浦有助于调节能源消耗,使汽车製造商能够满足更严格的燃油效率要求,同时又不影响车辆性能。

根据应用,市场还分为引擎系统、传动系统、动力转向系统、燃料管理系统和煞车系统等。 2024 年,引擎系统占据了 35% 的市场份额,其中可变排气量帮浦在优化内燃机性能方面发挥关键作用。这些帮浦可调节流体流量来调节燃料消耗,提高整体效率,同时确保符合严格的排放法规。汽车製造商正在利用这项技术来设计更省油的发动机,让他们在这个日益注重永续性和高性能的行业中占据竞争优势。

2024 年,亚太地区汽车可变排气量帮浦市场占有 40% 的主导份额,中国引领该地区的成长。对省油商用车的需求不断增长,推动了这些泵浦的采用,特别是在降低燃料消耗是首要任务的运输和物流领域。由于该地区拥有大量商用车辆,对先进的引擎优化解决方案的需求比以往任何时候都更加强烈。製造商正在大力投资创新泵浦技术,以帮助车辆符合燃油效率法规,同时确保高运行性能。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 零件供应商

- 製造商

- 技术提供者

- 最终用户

- 供应商概况

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻及倡议

- 监管格局

- 定价分析

- 成本明细分析

- 衝击力

- 成长动力

- 燃料成本上涨和环境问题

- 全球严格的排放和燃油经济性法规

- 新兴经济体汽车产量提高,可支配所得增加

- 泵浦设计和控制系统的技术进步

- 产业陷阱与挑战

- 初始成本高

- 与所有车型的兼容性有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按泵浦分类,2021 - 2034 年

- 主要趋势

- 油泵

- 变速箱泵

- 动力方向机帮浦

- 水泵浦

- 燃油帮浦

- 冷却液帮浦

第六章:市场估计与预测:依技术,2021 - 2034 年

- 主要趋势

- 电子的

- 油压

- 机械的

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 其他的

- 商用车

- 轻型商用车 (LCV)

- 重型商用车 (HCV)

第 8 章:市场估计与预测:按材料,2021 - 2034 年

- 主要趋势

- 铝

- 钢

- 铸铁

- 复合材料

第 9 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 引擎系统

- 传动系统

- 动力转向系统

- 燃料管理系统

- 煞车系统

- 其他的

第 10 章:市场估计与预测:按销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 11 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 12 章:公司简介

- AISIN SEIKI

- Bosch

- Bucher Industries

- Continental

- Danfoss

- Denso Corporation

- Eaton Corporation

- GKN Automotive

- HELLA GmbH

- Hitachi Automotive Systems

- HUSCO Automotive

- Johnson Electric

- JTEKT Corporation

- Magna International

- Mikuni Corporation

- Parker Hannifin

- Rheinmetall Automotive

- Schaeffler AG

- Valeo

- ZF Friedrichshafen

The Global Automotive Variable Displacement Pumps Market was valued at USD 3.1 billion in 2024 and is projected to grow at a CAGR of 4.3% between 2025 and 2034. The demand for fuel-efficient and environmentally friendly vehicles is increasing, driven by stringent emission regulations and evolving consumer preferences. Governments worldwide are enforcing stricter laws to lower carbon footprints and promote energy-efficient transportation, compelling automakers to integrate advanced technologies into their vehicles. Variable displacement pumps are emerging as a key solution, optimizing engine performance, enhancing fuel economy, and minimizing energy losses.

As automakers focus on achieving sustainability goals, hybrid and fuel-efficient vehicles are gaining traction, further boosting demand for these systems. Consumers are increasingly prioritizing fuel economy, making it imperative for manufacturers to adopt energy-efficient components that comply with regulatory standards. The need for energy optimization is also accelerating innovation in vehicle design, encouraging manufacturers to explore new ways to enhance performance while meeting global sustainability benchmarks. With rising fuel prices and a shift towards hybrid and electric vehicle adoption, variable displacement pumps are poised to play a crucial role in modern automotive engineering. The continued emphasis on fuel efficiency presents significant growth opportunities for industry players, ensuring sustained market demand for these pumps in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 4.3% |

The market is segmented by vehicle type into passenger and commercial vehicles, with passenger cars accounting for 70% of the total market share in 2024. This segment is expected to generate USD 3 billion by 2034. The increasing adoption of hybrid and fuel-efficient vehicles is propelling the demand for advanced automotive components that improve efficiency and functionality. Variable displacement pumps are crucial in optimizing hybrid vehicle performance, reducing unnecessary fluid displacement in non-hydraulic applications, and enhancing overall fuel management. These pumps help regulate energy consumption, allowing automakers to meet stricter fuel efficiency requirements without compromising vehicle performance.

The market is also classified by application into engine systems, transmission systems, power steering systems, fuel management systems, and brake systems, among others. Engine systems held a 35% market share in 2024, with variable displacement pumps playing a critical role in optimizing internal combustion engine performance. These pumps adjust fluid flow to regulate fuel consumption, improving overall efficiency while ensuring compliance with stringent emissions regulations. Automakers are leveraging this technology to design more fuel-efficient engines, giving them a competitive edge in an industry increasingly focused on sustainability and high performance.

The Asia Pacific automotive variable displacement pumps market held a dominant 40% share in 2024, with China leading the region's growth. The rising demand for fuel-efficient commercial vehicles is driving the adoption of these pumps, particularly in transportation and logistics sectors where reducing fuel consumption is a top priority. With an extensive fleet of commercial vehicles operating in the region, the need for advanced engine optimization solutions is stronger than ever. Manufacturers are heavily investing in innovative pump technologies to help vehicles comply with fuel efficiency regulations while ensuring high operational performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising fuel costs and environmental concerns

- 3.10.1.2 Strict global regulations on emissions and fuel economy

- 3.10.1.3 Higher automotive production in emerging economies and rising disposable incomes

- 3.10.1.4 Technological advancements in pump design and control systems

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial costs

- 3.10.2.2 Limited compatibility with all vehicle types

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Pump, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Oil pump

- 5.3 Transmission pump

- 5.4 Power steering pump

- 5.5 Water pump

- 5.6 Fuel pump

- 5.7 Coolant pump

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Electronic

- 6.3 Hydraulic

- 6.4 Mechanical

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUVs

- 7.2.4 Others

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCVs)

- 7.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Aluminum

- 8.3 Steel

- 8.4 Cast Iron

- 8.5 Composite material

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Engine systems

- 9.3 Transmission systems

- 9.4 Power steering systems

- 9.5 Fuel management systems

- 9.6 Brake systems

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn,Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 AISIN SEIKI

- 12.2 Bosch

- 12.3 Bucher Industries

- 12.4 Continental

- 12.5 Danfoss

- 12.6 Denso Corporation

- 12.7 Eaton Corporation

- 12.8 GKN Automotive

- 12.9 HELLA GmbH

- 12.10 Hitachi Automotive Systems

- 12.11 HUSCO Automotive

- 12.12 Johnson Electric

- 12.13 JTEKT Corporation

- 12.14 Magna International

- 12.15 Mikuni Corporation

- 12.16 Parker Hannifin

- 12.17 Rheinmetall Automotive

- 12.18 Schaeffler AG

- 12.19 Valeo

- 12.20 ZF Friedrichshafen