|

市场调查报告书

商品编码

1684720

自行车机械碟式煞车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Bicycle Mechanical Disc Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

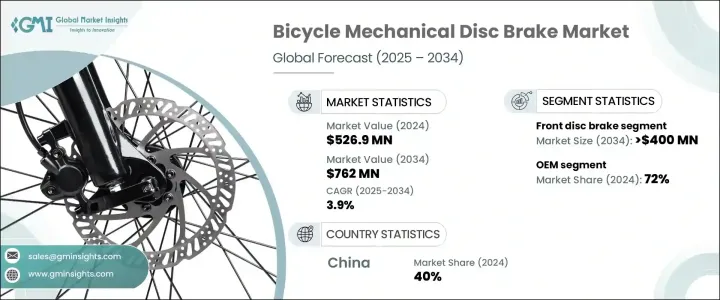

2024 年全球自行车机械碟式煞车市场规模达到 5.269 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 3.9%。日益转向永续交通是推动该市场向前发展的主要因素。世界各国政府都在投资自行车基础设施,推广自行车作为汽车的可行替代品。专用自行车道、对骑自行车者的税收优惠以及对电动自行车的补贴使骑自行车变得更加容易,最终推动了对机械碟式煞车的需求。随着城市化进程的加速和人们对环境问题的日益关注,自行车已经成为人们日常旅行的首选方式。随着越来越多的人开始骑自行车,对可靠煞车系统的需求也随之增长。

越来越多的消费者选择配备机械式碟式煞车的自行车,因为它们高效、耐用、经济实惠。与液压煞车不同,机械式碟式煞车需要的维护较少,并且在各种地形和天气条件下提供一致的性能。这种可靠性使其成为休閒和通勤骑乘者的理想选择。骑自行车健身和休閒的日益普及也促进了市场的扩张,因为骑士们寻求能够确保安全和控制的煞车系统。此外,轻质材料和改进的煞车片复合材料等煞车技术的进步提高了性能,进一步推动了煞车片的采用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5.269 亿美元 |

| 预测值 | 7.62亿美元 |

| 复合年增长率 | 3.9% |

电动自行车在推动自行车机械碟式煞车市场方面发挥着重要作用。机械式碟式煞车是电动自行车的首选,因为它们能在不同的速度和负载下提供可靠的煞车力道。许多政府,特别是欧洲政府,都将电动自行车的普及作为绿色交通计画的一部分。这些激励措施加上人们对电动车的日益青睐,推动了对机械碟式煞车的需求。随着电动自行车成为主流交通工具,製造商不断整合先进的煞车系统,确保骑乘者的安全和性能。

市场根据煞车类型分为前碟式煞车和后碟式煞车。前碟式煞车在 2024 年占据了 60% 的市场份额,预计到 2034 年将创造 4 亿美元的市场价值。消费者对高性能自行车的需求推动了这一成长,因为前碟式煞车在具有挑战性的条件下提供了卓越的煞车力道和更好的控制。无论是在陡峭的地形上行驶还是在潮湿的天气骑行,这些煞车都能增强骑乘者的稳定性和安全性。山地自行车和越野自行车的兴起进一步推动了对确保耐用性和控制力的高精度煞车技术的需求。

自行车机械碟式煞车的分销管道分为OEM和售后市场,其中 OEM 到 2024 年占据 72% 的主导份额。自行车製造商越来越多地与OEM煞车供应商合作,为其车型配备来自工厂的最新煞车技术。这些合作关係使品牌能够将高性能机械碟式煞车整合到其生产线中,确保新自行车符合现代安全和效率标准。随着消费者对高级自行车的期望不断提高, OEM销售预计将保持强劲势头,巩固市场成长。

中国仍然是全球自行车机械碟式煞车市场的主导者,到 2024 年将占 40% 的份额。中国对可持续出行和减少车辆排放的重视导致了自行车的广泛采用,尤其是在城市地区。中国有着强大的自行车文化,无论是通勤还是休閒,都推动着对高品质煞车系统的持续需求。政府推行的环保运输解决方案的政策进一步支持了这个市场,使中国成为机械碟式煞车生产和创新的重要枢纽。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 组件提供者

- 製造商

- 技术提供者

- 最终客户

- 供应商概况

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻及倡议

- 监管格局

- 定价分析

- 衝击力

- 成长动力

- 全球自行车普及率上升

- 环保意识推动人们转向环保交通

- 煞车部件的技术进步

- 政府推出措施支持自行车基础建设

- 产业陷阱与挑战

- 竞争激烈,价格敏感

- 转向液压碟式煞车

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按制动器,2021 - 2034 年

- 主要趋势

- 前碟式煞车

- 后碟式煞车

第六章:市场估计与预测:按供应量,2021 - 2034 年

- 主要趋势

- 单活塞

- 双活塞

- 四活塞

- 多活塞

第 7 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 公路自行车

- 登山车

- 赛车

- 砾石自行车

第 8 章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 9 章:市场估计与预测:按地区,2021 - 2034 年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Box Components

- Campagnolo

- Cane Creek

- Clarks Cycle Systems

- Formula

- Funn Components

- Hayes

- Hope Technology

- Jagwire

- KMC

- Magura

- Nutt

- Promax

- RockShox

- Shimano

- SRAM

- SunRace

- Tektro

- XLC

- Zoom

The Global Bicycle Mechanical Disc Brake Market reached USD 526.9 million in 2024 and is set to grow at a CAGR of 3.9% between 2025 and 2034. The increasing shift toward sustainable transportation is a major factor driving this market forward. Governments worldwide are investing in cycling infrastructure, promoting bicycles as a viable alternative to cars. Dedicated bike lanes, tax incentives for cyclists, and subsidies for electric bicycles are making cycling more accessible, ultimately boosting demand for mechanical disc brakes. With urbanization accelerating and environmental concerns on the rise, bicycles have become a preferred mode of daily travel. As more people turn to cycling, the need for reliable braking systems continues to grow.

Consumers are increasingly opting for bicycles equipped with mechanical disc brakes due to their efficiency, durability, and cost-effectiveness. Unlike hydraulic brakes, mechanical disc brakes require less maintenance and offer consistent performance across various terrains and weather conditions. This reliability makes them an ideal choice for both recreational and commuter cyclists. The growing popularity of cycling for fitness and leisure also contributes to market expansion, as riders seek braking systems that ensure safety and control. Additionally, advancements in brake technology, such as lightweight materials and improved pad compounds, enhance performance, further driving adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $526.9 Million |

| Forecast Value | $762 Million |

| CAGR | 3.9% |

Electric bicycles are playing a significant role in propelling the bicycle mechanical disc brake market. Mechanical disc brakes are the preferred choice for e-bikes because they deliver dependable stopping power under varying speeds and loads. Many governments, particularly in Europe, are incentivizing e-bike adoption as part of their green transportation initiatives. These incentives, coupled with an increasing preference for electric mobility, are fueling demand for mechanical disc brakes. As e-bikes transition into mainstream transportation, manufacturers continue to integrate advanced braking systems, ensuring safety and performance for riders.

The market is segmented by brake type into front and rear disc brakes. Front disc brakes accounted for 60% of the market share in 2024 and are projected to generate USD 400 million by 2034. Consumer demand for high-performance bicycles is driving this growth, as front disc brakes provide superior stopping power and better control in challenging conditions. Whether navigating steep terrain or cycling in wet weather, these brakes enhance rider stability and safety. The rise in mountain biking and off-road cycling further fuels the demand for high-precision braking technology that ensures durability and control.

Distribution channels for bicycle mechanical disc brakes are divided into OEM and aftermarket, with OEMs capturing a dominant 72% share in 2024. Bicycle manufacturers are increasingly collaborating with OEM brake suppliers to equip their models with the latest braking technology straight from the factory. These partnerships allow brands to integrate high-performance mechanical disc brakes into their production lines, ensuring that new bicycles meet modern safety and efficiency standards. With rising consumer expectations for premium bicycles, OEM sales are expected to maintain strong momentum, solidifying market growth.

China remains a dominant player in the global bicycle mechanical disc brake market, accounting for 40% of the share in 2024. The country's emphasis on sustainable mobility and reducing vehicle emissions has led to widespread bicycle adoption, particularly in urban areas. China's strong cycling culture, both for commuting and recreation, drives consistent demand for high-quality braking systems. Government policies promoting eco-friendly transport solutions further support this market, positioning China as a critical hub for mechanical disc brake production and innovation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Pricing analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increase in bicycle adoption across the world

- 3.9.1.2 Environmental awareness encourages the shift to eco-friendly transport

- 3.9.1.3 Technological advancements in brake components

- 3.9.1.4 Government initiatives supporting cycling infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High competition and price sensitivity

- 3.9.2.2 Shift toward hydraulic disc brakes

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Brake, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front disc brake

- 5.3 Rear disc brake

Chapter 6 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Single piston

- 6.3 Dual piston

- 6.4 Four piston

- 6.5 Multi-piston

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Road bike

- 7.3 Mountain bike

- 7.4 Racing bike

- 7.5 Gravel bikes

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Russia

- 9.2.7 Nordics

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.5 MEA

- 9.5.1 UAE

- 9.5.2 South Africa

- 9.5.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Box Components

- 10.2 Campagnolo

- 10.3 Cane Creek

- 10.4 Clarks Cycle Systems

- 10.5 Formula

- 10.6 Funn Components

- 10.7 Hayes

- 10.8 Hope Technology

- 10.9 Jagwire

- 10.10 KMC

- 10.11 Magura

- 10.12 Nutt

- 10.13 Promax

- 10.14 RockShox

- 10.15 Shimano

- 10.16 SRAM

- 10.17 SunRace

- 10.18 Tektro

- 10.19 XLC

- 10.20 Zoom

汽车煞车碟盘市场:依产品类型、材料、车辆类型、销售通路、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

汽车煞车碟盘市场:依产品类型、材料、车辆类型、销售通路、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 汽车碟式煞车市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年)

汽车碟式煞车市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年) 汽车碟式煞车市场分析及预测(至2034年):类型、产品、技术、组件、材料类型、应用、最终用户、能力、安装类型、解决方案

汽车碟式煞车市场分析及预测(至2034年):类型、产品、技术、组件、材料类型、应用、最终用户、能力、安装类型、解决方案 2032 年汽车碟式煞车市场预测:按类型、材料、车辆类型、技术、销售管道、应用和地区进行的全球分析

2032 年汽车碟式煞车市场预测:按类型、材料、车辆类型、技术、销售管道、应用和地区进行的全球分析 全球汽车碟式煞车市场

全球汽车碟式煞车市场 自行车液压碟式煞车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

自行车液压碟式煞车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测 开槽煞车盘的全球市场:实际成果与预测(2019年~2030年)到 2030 年湿式多碟式煞车的市场预测:按类型、材料、设备、最终用户和地区进行的全球分析到 2030 年气动多碟式煞车的全球市场预测:按类型、应用和地区分析

开槽煞车盘的全球市场:实际成果与预测(2019年~2030年)到 2030 年湿式多碟式煞车的市场预测:按类型、材料、设备、最终用户和地区进行的全球分析到 2030 年气动多碟式煞车的全球市场预测:按类型、应用和地区分析