|

市场调查报告书

商品编码

1684758

丙烯酸乳液市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Acrylic Emulsion Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

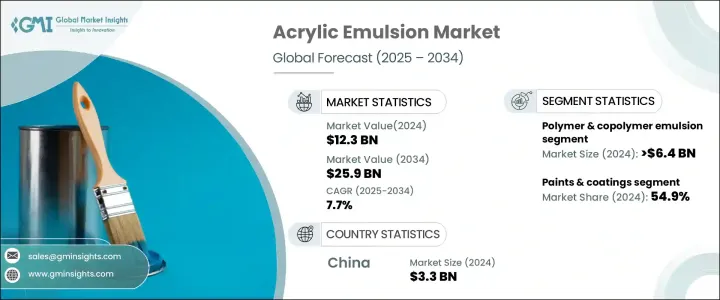

2024 年全球丙烯酸乳液市场价值为 123 亿美元,预计 2025 年至 2034 年期间将以 7.7% 的复合年增长率稳步增长。这些特性使得丙烯酸乳液成为汽车、航太、石油和天然气以及化学加工等需要耐用密封解决方案的产业中不可或缺的一部分。随着业界不断创新和对性能优异材料的需求,丙烯酸乳液市场有望大幅扩张。对环保和高性能材料的需求不断增长,进一步增强了对丙烯酸乳液的需求,尤其是在建筑、汽车和工业领域。

2024 年,聚合物和共聚物乳液领域创造了 64 亿美元的收入。这些乳液广泛应用于黏合剂、密封剂和专用涂料,具有多功能性和高效性,可满足多样化的市场需求。随着各行业采用日益先进的製造技术,对这些乳液的需求预计将稳定上升,确保其在市场上继续占据主导地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 123亿美元 |

| 预测值 | 259亿美元 |

| 复合年增长率 | 7.7% |

2024 年,油漆和涂料领域占据市场主导地位,占有 54.9% 的份额,预计到 2034 年将大幅增长。这些基本特性有助于生产持久、美观的饰面,从而推动汽车、建筑和消费品等各行业的需求。对能够应对环境挑战的高品质饰面的需求确保了该领域在未来几年将继续实现大幅增长。

2024 年中国丙烯酸乳液市场规模将达到 33 亿美元,预计 2025 年至 2034 年间将以惊人的速度增长。城市化以及大型基础设施项目的成长在扩大市场规模方面发挥关键作用。此外,日本和韩国等国家蓬勃发展的汽车产业继续促进对丙烯酸乳液的持续需求。由于这些地区仍处于工业成长的前沿,预计对丙烯酸乳液的需求将持续上升,从而促进全球市场的扩张。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 对环保和低 VOC 涂料的需求不断增加

- 建筑业的成长推动了对丙烯酸乳液涂料的需求

- 纺织业的成长,利用丙烯酸乳液进行功能性整理

- 产业陷阱与挑战

- 对环保和低 VOC 涂料的需求不断增加

- 建筑业的成长推动了对丙烯酸乳液涂料的需求

- 纺织业的成长,利用丙烯酸乳液进行功能性整理

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场规模与预测:按类型,2021-2034 年

- 主要趋势

- 纯丙烯酸乳液

- 聚合物及共聚物丙烯酸乳液

第 6 章:市场规模与预测:按应用,2021-2034 年

- 主要趋势

- 油漆和涂料

- 黏合剂和密封剂

- 建筑材料添加剂

- 纸张涂料

- 其他

第 7 章:市场规模与预测:依最终用途产业,2021-2034 年

- 主要趋势

- 建造

- 汽车

- 纺织品

- 其他

第 8 章:市场规模与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Alv Kimya

- Arkema Group

- Avery Dennison Performance Polymers

- BASF

- Celanese

- Covestro

- DIC

- Dow Inc

- Henkel Additives

- HB Fuller

- Jensen & Nicholson

- Mallard Creek Polymers

- Max Paints

- Mitsui Chemicals

The Global Acrylic Emulsion Market was valued at USD 12.3 billion in 2024 and is expected to experience steady growth at a CAGR of 7.7% between 2025 and 2034. Acrylic emulsions, also known as FKM, are synthetic elastomers prized for their remarkable resistance to heat, chemicals, and a range of fluids. These characteristics make acrylic emulsions indispensable in industries that require durable sealing solutions, such as automotive, aerospace, oil and gas, and chemical processing. As industries continue to innovate and demand materials with superior performance, the acrylic emulsion market is well-positioned for significant expansion. The growing need for eco-friendly and high-performance materials further strengthens the demand for acrylic emulsions, especially in the construction, automotive, and industrial sectors.

The polymer and copolymer emulsion segment generated USD 6.4 billion in 2024. This segment is particularly notable for its additional polymers and copolymers, which enhance specific properties suited for various industrial applications. These emulsions are widely used in adhesives, sealants, and specialized coatings, offering both versatility and efficiency in meeting diverse market demands. As industries adopt increasingly advanced manufacturing techniques, the demand for these emulsions is expected to rise steadily, ensuring their continued prominence in the marketplace.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.3 Billion |

| Forecast Value | $25.9 Billion |

| CAGR | 7.7% |

In 2024, the paints and coatings segment dominated the market with a significant 54.9% share and is forecast to grow substantially by 2034. Acrylic emulsions are especially favored for premium paints and coatings due to their superior adhesion, weathering resistance, and durability. These essential properties contribute to the production of long-lasting, aesthetically pleasing finishes, driving demand across various industries, including automotive, architecture, and consumer goods. The need for high-quality finishes that stand up to environmental challenges ensures that this segment will continue to see substantial growth in the coming years.

China acrylic emulsion market reached USD 3.3 billion in 2024 and is projected to grow at an impressive rate between 2025 and 2034. The rapid expansion of the construction industry in China and India significantly drives this demand, as acrylic emulsions are extensively used in paints, coatings, and construction material additives. Urbanization, along with the growth of large-scale infrastructure projects, is playing a key role in increasing the market's size. Furthermore, the thriving automotive sector in countries like Japan and South Korea continues to contribute to the consistent demand for acrylic emulsions. As these regions remain at the forefront of industrial growth, the demand for acrylic emulsions is expected to keep rising, contributing to the global market's expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.6.1.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.6.1.3 Growth in the textile industry, leveraging acrylic emulsions in functional finishes

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Increasing demand for eco-friendly and low-VOC coatings

- 3.6.2.2 Growth in the construction industry, driving demand for acrylic emulsion-based paints

- 3.6.2.3 Growth in the textile industry, leveraging acrylic emulsions in functional finishes

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pure acrylic emulsion

- 5.3 Polymer & copolymer acrylic emulsion

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Paints & coatings

- 6.3 Adhesives & sealants

- 6.4 Construction material additives

- 6.5 Paper coatings

- 6.6 Other

Chapter 7 Market Size and Forecast, By End Use Industries, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automobile

- 7.4 Textile

- 7.5 Other

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alv Kimya

- 9.2 Arkema Group

- 9.3 Avery Dennison Performance Polymers

- 9.4 BASF

- 9.5 Celanese

- 9.6 Covestro

- 9.7 DIC

- 9.8 Dow Inc

- 9.9 Henkel Additives

- 9.10 H.B. Fuller

- 9.11 Jensen & Nicholson

- 9.12 Mallard Creek Polymers

- 9.13 Max Paints

- 9.14 Mitsui Chemicals