|

市场调查报告书

商品编码

1684764

胆道支架市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Biliary Stents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

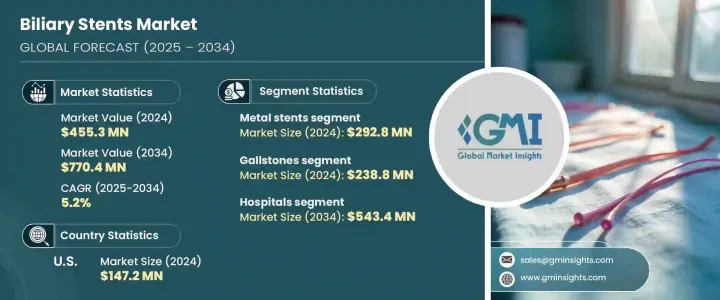

2024 年全球胆道支架市场规模达到 4.553 亿美元,预计到 2034 年将以 5.2% 的复合年增长率稳定成长。这一增长很大程度上可归因于肝臟和胆管疾病盛行率的不断上升,以及支架技术的不断进步。胆道支架主要用于治疗导致胆管阻塞的疾病,例如胆管炎、胰臟炎和某些癌症。这些情况会导致阻塞,扰乱胆汁流动,需要使用支架来缓解和治疗。

随着全球人口老化和生活方式相关的健康问题的增加,对胆道支架的需求预计将大幅增加。此外,随着支架技术的创新,包括药物洗脱和可生物降解材料的开发,这些设备变得更加有效,可确保更好的患者治疗结果和更持久的解决方案。这种扩张也受到医疗保健机会的增加和程序技术的改进的推动,使得支架置入更加有效,从而促进了市场的积极发展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 4.553亿美元 |

| 预测值 | 7.704 亿美元 |

| 复合年增长率 | 5.2% |

市场主要分为两个关键部分:金属支架和聚合物支架。 2024 年,金属支架部分价值为 2.928 亿美元。金属支架,尤其是自膨胀式支架,因其能够治疗恶性阻塞并提供持久的解决方案,从而减少更换频率而受到青睐。这些支架对于癌症患者的安宁疗护至关重要,并透过完全和部分覆盖的版本提供额外的好处,例如防止肿瘤生长和迁移。可生物降解和药物洗脱金属支架的引入增加了它们的吸引力,并因其先进的特性进一步推动了它们在医疗领域的应用。

医院部门是胆道支架的主要终端用户,预计到预测期末将达到 5.434 亿美元。医院拥有必要的基础设施和专业知识来执行 ERCP 和 PTC 等复杂程序,这对于诊断和治疗胆道疾病至关重要。这些程序对于确保胆道支架的准确放置起着至关重要的作用,最终有助于改善患者的治疗效果。随着支架技术和置入技术的不断进步,医院有望继续引领市场,为患有胆道疾病的患者提供最佳护理。

在美国,2024 年胆道支架市场价值为 1.472 亿美元,预计 2025 年至 2034 年期间的成长率为 4.9%。这一增长主要得益于胆道疾病发病率的上升和医疗保健机会的增强。保险覆盖(包括医疗保险和医疗补助等计划)对于让更广泛的患者群体能够接受支架手术至关重要,从而进一步加速了对胆道支架的需求。这项资金支持确保患者得到必要的治疗,以有效治疗胆管阻塞。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 胆管疾病和慢性肝病盛行率不断上升

- 支架的技术进步

- 手术过程中采用微创方法

- 全球老年人口不断增长

- 产业陷阱与挑战

- 胆管支架相关的併发症和风险

- 塑胶胆管支架成本高

- 成长动力

- 成长潜力分析

- 2024 年定价分析

- 监管格局

- 报销场景

- 技术格局

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 金属支架

- 聚合物支架

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 胆结石

- 胰腺癌

- 胆胰漏

- 良性胆道狭窄

- 其他应用

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 专科诊所

- 其他最终用户

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- B Braun

- Becton, Dickinson & Company

- Boston Scientific

- Cardinal Health

- CONMED Corporation

- Cook Group

- ENDO-FLEX GmbH

- MI Tech

- Mediwood

- Medtronic

- Merit Medical System

- Olympus Corporation

- S & G Biotech

- TAEWOONG

The Global Biliary Stents Market reached USD 455.3 million in 2024 and is projected to grow at a steady CAGR of 5.2% through 2034. This growth can largely be attributed to the increasing prevalence of liver and bile duct diseases, in line with ongoing advancements in stent technologies. Biliary stents are primarily used to manage conditions that cause bile duct blockages, such as cholangitis, pancreatitis, and certain cancers. These conditions can result in obstructions that disrupt bile flow, necessitating the use of stents for relief and treatment.

As the global population ages and lifestyle-related health issues rise, the demand for biliary stents is expected to surge significantly. Moreover, with innovations in stent technology, including the development of drug-eluting and biodegradable materials, these devices have become more effective, ensuring better patient outcomes and longer-lasting solutions. This expansion is also driven by increasing healthcare access and improvements in procedural techniques that allow more efficient stent placements, contributing to the market's positive trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $455.3 Million |

| Forecast Value | $770.4 Million |

| CAGR | 5.2% |

The market is primarily divided into two key segments: metal and polymer stents. In 2024, the metal stents segment was worth USD 292.8 million. Metal stents, particularly self-expanding versions, are favored for their ability to treat malignant obstructions and provide long-lasting solutions, reducing the frequency of replacements. These stents are critical in palliative care for cancer patients, offering additional benefits such as the prevention of tumor ingrowth and migration through fully and partially covered versions. The introduction of biodegradable and drug-eluting metal stents has increased their appeal, further driving their adoption across medical settings due to their advanced features.

The hospitals segment, the primary end-user of biliary stents, is expected to reach USD 543.4 million by the end of the forecast period. Hospitals have necessary infrastructure and expertise to perform complex procedures like ERCP and PTC, essential for diagnosing and treating biliary conditions. These procedures play a crucial role in ensuring the accurate placement of biliary stents, which ultimately contributes to improved treatment outcomes for patients. With continuous advancements in stent technology and placement techniques, hospitals are expected to continue leading the market, offering optimal care for individuals suffering from biliary disorders.

In the U.S., the biliary stents market was valued at USD 147.2 million in 2024, with an anticipated growth rate of 4.9% between 2025 and 2034. This growth is primarily driven by the rising incidence of biliary diseases and enhanced access to healthcare. Insurance coverage, including programs such as Medicare and Medicaid, are vital in making stent procedures more accessible to a broader patient base, further accelerating the demand for biliary stents. This financial support ensures that patients receive the necessary treatment to manage bile duct obstructions effectively.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of bile duct and chronic liver disease

- 3.2.1.2 Technological advancements in stents

- 3.2.1.3 Adoption of minimally invasive approach during the procedure

- 3.2.1.4 Growing geriatric population globally

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications and risks related to bile duct stents

- 3.2.2.2 High cost of the plastic bile duct stents

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis, 2024

- 3.5 Regulatory landscape

- 3.6 Reimbursement scenario

- 3.7 Technology landscape

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Metal stents

- 5.3 Polymer stents

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gallstones

- 6.3 Pancreatic cancer

- 6.4 Bilio-pancreatic leakages

- 6.5 Benign biliary strictures

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Other end-users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Becton, Dickinson & Company

- 9.3 Boston Scientific

- 9.4 Cardinal Health

- 9.5 CONMED Corporation

- 9.6 Cook Group

- 9.7 ENDO-FLEX GmbH

- 9.8 M.I Tech

- 9.9 Mediwood

- 9.10 Medtronic

- 9.11 Merit Medical System

- 9.12 Olympus Corporation

- 9.13 S & G Biotech

- 9.14 TAEWOONG