|

市场调查报告书

商品编码

1684819

无人地面车辆市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Unmanned Ground Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

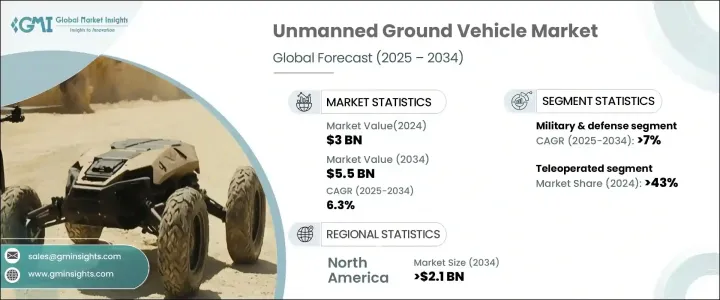

2024 年全球无人地面车辆市场价值为 30 亿美元,预计 2025 年至 2034 年的复合年增长率为 6.3%。军事和国防行动对自动化的需求日益增加,推动了这一增长,因为 UGV 在执行侦察、监视和爆炸物处理等高风险任务中发挥着至关重要的作用。透过减少对人员的威胁,这些车辆提高了任务效率和操作安全性。人工智慧、感测器技术和机器学习的进步不断提高 UGV 的能力,使其能够在复杂地形上实现更精确、更自主的导航。增强的电池性能和即时资料处理进一步扩大了它们的作战范围,使其成为现代战争和安全应用中不可或缺的一部分。

随着世界各国政府优先考虑增强态势感知和任务效率的尖端技术,对边境安全、反恐和国土防御的日益关注加速了 UGV 的采用。国防部队正在增加对自主和远程操作地面系统的投资,以增强作战和监视能力。此外,UGV 的应用范围已不仅限于军事,采矿、农业和物流等行业也纷纷整合这些车辆,以提高营运安全性和生产力。自动化 UGV 透过处理危险任务、减少危险环境中的人为介入并提高成本效率来简化工业流程。随着智慧导航系统的出现和障碍物侦测的改进,这些车辆将改变多个领域的自主运作的未来。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 30亿美元 |

| 预测值 | 55亿美元 |

| 复合年增长率 | 6.3% |

遥控领域将在 2024 年占据 43% 的市场份额,并将继续大幅成长。增强的通讯技术,包括 5G 和卫星连接,可以实现远距离的即时远端操作,使操作员能够精确地、以最小的延迟控制 UGV。这些进步大大提高了操作的灵活性,特别是在立即响应和准确操纵至关重要的危险环境中。国防部门仍然是遥控 UGV 的最大采用者,利用它们进行监视、侦察和消除威胁。它们能够在衝突地区或受灾地区远端部署,确保了持续的需求,巩固了该领域在市场上的主导地位。

军事和国防部门推动了 UGV 市场的大幅扩张,预计到 2034 年的复合年增长率为 7%。这些车辆在现代作战战略中发挥关键作用,执行需要即时情报收集、自主导航和危险物质处理的任务。配备人工智慧驱动的决策和先进的导航演算法,UGV 可以无缝适应动态战场条件,最大限度地降低风险,同时最大限度地提高作战效率。随着国防机构优先考虑自动化以增强战略应变能力,对下一代 UGV 的需求持续上升。

预计到 2034 年,北美 UGV 市场将创收 21 亿美元,美国将在自主地面系统方面处于领先地位。国防对人工智慧军事解决方案的投资不断增加,正在重塑战场战略,从而提高任务的精确度和战术决策能力。製造商正在开发可互通的 UGV 系统,以便与其他无人平台无缝集成,从而优化任务效率。随着国防机构对其舰队进行现代化改造,持续的创新和战略资金推动市场成长,使北美成为下一代无人系统的重要枢纽。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 自主技术的进步

- 增加国防开支和现代化

- 工业自动化需求不断成长

- 持续的地缘政治不稳定与安全问题

- 增加政府对国防和机器人技术的投资

- 产业陷阱与挑战

- 开发成本高

- 与现有系统集成

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按规模,2021-2034 年

- 主要趋势

- 小型(20 磅至 400 磅)

- 中型(401 磅至 2,500 磅)

- 大型(2,501 磅至 20,000 磅)

- 特大型(超过 20,000 磅)

第六章:市场估计与预测:依移动性,2021-2034 年

- 主要趋势

- 轮式

- 履带式

- 有腿的

- 杂交种

第 7 章:市场估计与预测:按系统,2021 年至 2034 年

- 主要趋势

- 有效载荷

- 导航系统

- 控制系统

- 电力系统

- 其他的

第 8 章:市场估计与预测:按营运模式,2021 年至 2034 年

- 主要趋势

- 自主

- 遥控

- 繫留

第 9 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 军事与国防

- 搜救 (SAR)

- 特殊使命

- 战斗支援

- 爆炸物处理 (EOD) 系统

- 其他的

- 商业的

- 消防

- 石油和天然气

- 农业

- 其他的

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Aselsan

- BAE Systems

- ECA Group

- Elbit Systems

- General Dynamics

- Hexagon

- Israel Aerospace Industries

- L3Harris

- Lockheed Martin

- Northrop Grumman

- QinetiQ

- Rheinmetall

- ST Engineering

- Teledyne

- Textron

- Thales

The Global Unmanned Ground Vehicle Market, valued at USD 3 billion in 2024, is set to expand at a CAGR of 6.3% from 2025 to 2034. The increasing need for automation in military and defense operations is fueling this growth as UGVs play a vital role in executing high-risk tasks, including reconnaissance, surveillance, and explosive ordnance disposal. By reducing threats to human personnel, these vehicles enhance mission efficiency and operational safety. Advances in artificial intelligence, sensor technology, and machine learning continue to improve UGV capabilities, enabling more precise and autonomous navigation across complex terrains. Enhanced battery performance and real-time data processing further extend their operational range, making them indispensable in modern warfare and security applications.

The growing focus on border security, counterterrorism, and homeland defense accelerates the adoption of UGVs as governments worldwide prioritize cutting-edge technologies that enhance situational awareness and mission effectiveness. Defense forces are increasingly investing in autonomous and remotely operated ground systems to bolster combat and surveillance capabilities. Additionally, UGVs are gaining traction beyond military applications, with industries such as mining, agriculture, and logistics integrating these vehicles to improve operational safety and productivity. Automated UGVs streamline industrial processes by handling hazardous tasks, reducing human intervention in dangerous environments, and improving cost efficiency. With the emergence of smart navigation systems and improved obstacle detection, these vehicles are poised to transform the future of autonomous operations across multiple sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 billion |

| Forecast Value | $5.5 billion |

| CAGR | 6.3% |

The teleoperated segment, which accounted for 43% of the market share in 2024, continues to witness substantial growth. Enhanced communication technologies, including 5G and satellite connectivity, enable real-time remote operation across vast distances, allowing operators to control UGVs with precision and minimal latency. These advancements significantly enhance operational flexibility, particularly in hazardous environments where immediate response and accurate maneuvering are crucial. The defense sector remains the largest adopter of teleoperated UGVs, utilizing them for surveillance, reconnaissance, and threat neutralization. Their ability to be deployed remotely in conflict zones or disaster-stricken areas ensures continuous demand, reinforcing the segment's dominance in the market.

The military and defense sector drives significant expansion in the UGV market, with an expected CAGR of 7% through 2034. These vehicles play a pivotal role in modern combat strategies, executing missions that require real-time intelligence gathering, autonomous navigation, and hazardous material handling. Equipped with AI-driven decision-making and advanced navigation algorithms, UGVs seamlessly adapt to dynamic battlefield conditions, minimizing risks while maximizing operational efficiency. As defense agencies prioritize automation to enhance strategic response capabilities, the demand for next-generation UGVs continues to rise.

North America UGV market is projected to generate USD 2.1 billion by 2034, with the United States leading advancements in autonomous ground systems. Rising defense investments in AI-driven military solutions are reshaping battlefield strategies, thus improving mission precision and tactical decision-making. Manufacturers are developing interoperable UGV systems that integrate seamlessly with other unmanned platforms, optimizing mission effectiveness. As defense agencies modernize their fleets, continuous innovation and strategic funding drive market growth, positioning North America as a key hub for next-generation unmanned systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in autonomous technologies

- 3.6.1.2 Increased defense spending and modernization

- 3.6.1.3 Rising demand for automation in industry

- 3.6.1.4 Ongoing geopolitical instability and security concerns

- 3.6.1.5 Increasing government investments in defense and robotics

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High development costs

- 3.6.2.2 Integration with existing systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Size, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Small (20lb to 400lb)

- 5.3 Medium (401lb to 2,500lb)

- 5.4 Large (2,501lb to 20,000lb)

- 5.5 Extra-large (Over 20,000lb)

Chapter 6 Market Estimates & Forecast, By Mobility, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Wheeled

- 6.3 Tracked

- 6.4 Legged

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By System, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Payloads

- 7.3 Navigation system

- 7.4 Controller system

- 7.5 Power system

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Mode of Operation, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Autonomous

- 8.3 Teleoperated

- 8.4 Tethered

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Military & defense

- 9.2.1 Search & rescue (SAR)

- 9.2.2 Special mission

- 9.2.3 Combat support

- 9.2.4 Explosive Ordnance Disposal (EOD) System

- 9.2.5 Others

- 9.3 Commercial

- 9.3.1 Fire fighting

- 9.3.2 Oil & gas

- 9.3.3 Agriculture

- 9.3.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aselsan

- 11.2 BAE Systems

- 11.3 ECA Group

- 11.4 Elbit Systems

- 11.5 General Dynamics

- 11.6 Hexagon

- 11.7 Israel Aerospace Industries

- 11.8 L3Harris

- 11.9 Lockheed Martin

- 11.10 Northrop Grumman

- 11.11 QinetiQ

- 11.12 Rheinmetall

- 11.13 ST Engineering

- 11.14 Teledyne

- 11.15 Textron

- 11.16 Thales

农业无人机市场:按平台、类型和应用划分,全球预测(2026-2032年)

农业无人机市场:按平台、类型和应用划分,全球预测(2026-2032年) 无人地面车辆市场规模、份额和成长分析(按营运方式、移动性、尺寸、系统、应用和地区划分)-产业预测,2026-2033年无人地面车辆市场按组件、操作模式、机动性、有效载荷容量、动力来源、尺寸、应用和分销渠道划分 - 全球预测 2025-2030

无人地面车辆市场规模、份额和成长分析(按营运方式、移动性、尺寸、系统、应用和地区划分)-产业预测,2026-2033年无人地面车辆市场按组件、操作模式、机动性、有效载荷容量、动力来源、尺寸、应用和分销渠道划分 - 全球预测 2025-2030 无人地面车辆市场规模、份额和趋势分析报告:按营运、机动性、规模、系统、应用、地区和细分市场预测,2025 年至 2033 年

无人地面车辆市场规模、份额和趋势分析报告:按营运、机动性、规模、系统、应用、地区和细分市场预测,2025 年至 2033 年 无人地面车辆的全球市场:用途·行动·尺寸·行动方式·各地区的机会及预测 (2018-2032年)

无人地面车辆的全球市场:用途·行动·尺寸·行动方式·各地区的机会及预测 (2018-2032年) 无人地面车辆(UGV)的全球市场:2025年~2035年

无人地面车辆(UGV)的全球市场:2025年~2035年 无人地面车辆 (UGV) 市场按产品类型、移动性、操作模式、应用、最终用户、分销管道和地区划分,2024 年至 2031 年

无人地面车辆 (UGV) 市场按产品类型、移动性、操作模式、应用、最终用户、分销管道和地区划分,2024 年至 2031 年