|

市场调查报告书

商品编码

1684868

腔内缝合装置市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Endoluminal Suturing Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

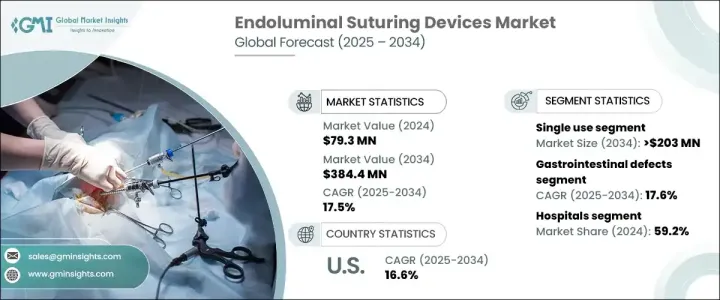

2024 年全球腔内缝合器市场价值为 7,930 万美元,预计 2025 年至 2034 年期间将以 17.5% 的强劲复合年增长率扩张,这得益于人们对微创手术的偏好日益增加以及胃肠道和减肥手术数量的增加。由于医疗保健提供者优先考虑患者的安全和更快的恢復时间,对先进缝合解决方案的需求持续上升。全球范围内肥胖症的日益流行导致了减肥手术的激增,其中腔内缝合装置在胃绕道手术和外科修復等手术中发挥着至关重要的作用。此外,包括改进的可视化、增强的可操作性和与机器人系统的整合在内的技术进步,使得这些设备更加高效、更易于使用。这种向精准手术干预的转变极大地促进了市场扩张。

越来越多的医疗专业人员开始采用腔内缝合装置,因为它能够降低手术风险、缩短住院时间并改善病患治疗效果。这些设备具有高精度,能够在复杂的手术过程中实现无缝组织近似。随着医疗机构强调感染控制和成本效益,对一次性缝合设备的需求正在激增。自动缝合系统和人工智慧手术工具的引入进一步简化了操作,使手术更加安全、有效。此外,监管部门的批准和优惠的报销政策正在支持市场成长,鼓励人们采用这些创新医疗设备。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7,930 万美元 |

| 预测值 | 3.844亿美元 |

| 复合年增长率 | 17.5% |

在产品类型中,一次性产品将成为主要驱动力,预计复合年增长率为 17.2%,到 2034 年将达到 2.03 亿美元。这些设备在外科手术中更受青睐,因为它们能够消除交叉污染风险并减少感染相关的併发症。它们的便利性,加上无需消毒,大大降低了营运成本,同时确保符合严格的卫生标准。尤其是医院和门诊手术中心,正在采用一次性腔内缝合装置来提高效率和病人安全。随着医疗保健行业转向一次性解决方案以满足监管和安全要求,这些先进设备的需求预计将激增。

胃肠道缺陷应用领域预计将显着成长,预计复合年增长率为 17.6%,到 2034 年将达到 1.696 亿美元。溃疡、穿孔和瘻管等胃肠道疾病发病率的增加推动了对微创治疗方案的需求。许多此类疾病源自于慢性疾病和生活方式相关因素,需要有效的手术介入。腔内缝合装置为此类复杂病例提供了精确、微创的解决方案,提高了患者的康復率并减少了术后併发症。人们越来越关注透过先进的缝合技术加强胃肠道护理,这进一步推动了市场扩张。

美国腔内缝合器市场预计将大幅成长,2024 年价值估计将达到 2,740 万美元。肥胖率上升和胃肠道疾病盛行率上升是推动需求的关键因素。随着减重手术越来越受欢迎以及对慢性胃肠道疾病创新治疗的需求不断增长,腔内缝合装置正成为全国各地外科医生的首选。人口老化加上生活方式的转变,进一步加速了对这些设备的需求。随着手术技术的不断进步和对微创手术的大力投入,美国市场预计将在塑造腔内缝合解决方案的未来方面发挥关键作用。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球慢性病盛行率上升

- 微创手术的需求不断增加

- 技术进步

- 老年人口不断增加

- 产业陷阱与挑战

- 严格的监管环境

- 缺乏熟练的医疗保健专业人员

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按产品类型,2021 年至 2034 年

- 主要趋势

- 一次使用

- 可重复使用的

第 6 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 胃肠道缺陷

- 减重手术

- 胃食道逆流症(GERD)

- 其他应用

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用户

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Apollo Endosurgery

- Boston Scientific

- Braun Melsungen

- Cook Group

- Endo Tools Therapeutics

- ErgoSuture

- Johnson and Johnson

- Karl Storz

- Medtronic

- Olympus Corporation

- Ovesco Endoscopy

- Richard Wolf

- Teleflex Corporation

- Terumo Corporation

- USGI Medical

The Global Endoluminal Suturing Devices Market, valued at USD 79.3 million in 2024, is projected to expand at a robust CAGR of 17.5% from 2025 to 2034., driven by the increasing preference for minimally invasive surgical procedures and the rising number of gastrointestinal and bariatric surgeries. As healthcare providers prioritize patient safety and faster recovery times, the demand for advanced suturing solutions continues to rise. The growing prevalence of obesity worldwide has led to a surge in bariatric procedures, where endoluminal suturing devices play a crucial role in procedures like gastric bypass and surgical revisions. Furthermore, technological advancements, including improved visualization, enhanced maneuverability, and integration with robotic systems, are making these devices more efficient and easier to use. This shift towards precision-driven surgical interventions is significantly contributing to market expansion.

Medical professionals are increasingly embracing endoluminal suturing devices due to their ability to reduce surgical risks, shorten hospital stays, and improve patient outcomes. These devices offer high accuracy, enabling seamless tissue approximation in complex surgical procedures. As healthcare facilities emphasize infection control and cost-efficiency, the demand for disposable, single-use suturing devices is surging. The introduction of automated suturing systems and AI-driven surgical tools is further streamlining operations, making procedures safer and more effective. Additionally, regulatory approvals and favorable reimbursement policies are supporting market growth, encouraging the adoption of these innovative medical devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $79.3 Million |

| Forecast Value | $384.4 Million |

| CAGR | 17.5% |

Among product types, the single-use segment is set to be a key driver, with a projected CAGR of 17.2%, reaching an estimated USD 203 million by 2034. These devices are preferred in surgical settings due to their ability to eliminate cross-contamination risks and reduce infection-related complications. Their convenience, combined with the elimination of sterilization requirements, significantly lowers operational costs while ensuring compliance with stringent hygiene standards. Hospitals and ambulatory surgical centers, in particular, are embracing single-use endoluminal suturing devices to enhance efficiency and patient safety. As the healthcare industry moves towards disposable solutions to meet regulatory and safety requirements, the demand for these advanced devices is expected to surge.

The gastrointestinal defects application segment is anticipated to witness significant growth, with a projected CAGR of 17.6%, reaching USD 169.6 million by 2034. The increasing incidence of gastrointestinal conditions, including ulcers, perforations, and fistulas, is driving demand for minimally invasive treatment options. Many of these conditions stem from chronic diseases and lifestyle-related factors, necessitating effective surgical interventions. Endoluminal suturing devices provide a precise and minimally invasive solution for such complex cases, improving patient recovery rates and reducing post-surgical complications. The growing focus on enhancing gastrointestinal care through advanced suturing technologies is further fueling market expansion.

The United States endoluminal suturing devices market is poised for substantial growth, with an estimated value of USD 27.4 million in 2024. The rising obesity rates and increasing prevalence of gastrointestinal disorders are key factors driving demand. As bariatric procedures gain popularity and the need for innovative treatments for chronic gastrointestinal diseases grows, endoluminal suturing devices are becoming a preferred choice for surgeons across the country. The aging population, coupled with shifting lifestyle trends, is further accelerating the demand for these devices. With continuous advancements in surgical technology and strong investment in minimally invasive procedures, the US market is expected to play a pivotal role in shaping the future of endoluminal suturing solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic disease across the globe

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising geriatric population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 Dearth of skilled healthcare professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Single use

- 5.3 Reusable

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gastrointestinal defects

- 6.3 Bariatric surgery

- 6.4 Gastroesophageal reflux disease (GERD)

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Apollo Endosurgery

- 9.2 Boston Scientific

- 9.3 Braun Melsungen

- 9.4 Cook Group

- 9.5 Endo Tools Therapeutics

- 9.6 ErgoSuture

- 9.7 Johnson and Johnson

- 9.8 Karl Storz

- 9.9 Medtronic

- 9.10 Olympus Corporation

- 9.11 Ovesco Endoscopy

- 9.12 Richard Wolf

- 9.13 Teleflex Corporation

- 9.14 Terumo Corporation

- 9.15 USGI Medical