|

市场调查报告书

商品编码

1684871

船舶船上通讯与控制系统市场机会、成长动力、产业趋势分析与预测 2025 - 2034Marine Onboard Communication and Control Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

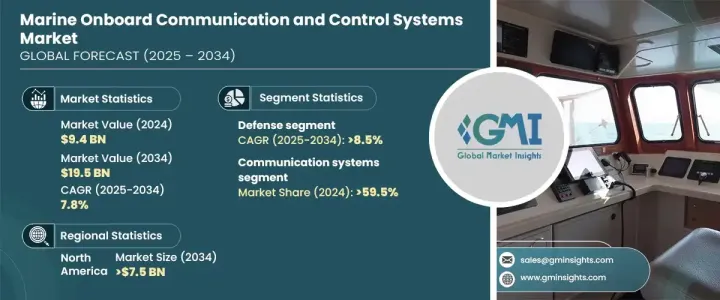

2024 年全球船舶船上通讯和控制系统市场价值为 94 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 7.8%。这一令人印象深刻的成长轨迹是由越来越依赖先进技术来优化海上作业所推动的。随着全球贸易的快速发展和对安全、高效海上运输的需求不断增长,采用最先进的通讯和控制系统已变得至关重要。这些系统实现了无缝协调、即时监控和资料交换,确保了海事部门的营运安全和效率。此外,该行业正在经历向环保创新和基于卫星的解决方案的转变,这有望彻底改变船上通讯和控制流程。

儘管前景乐观,但市场仍面临挑战。高昂的安装成本、恶劣的海洋环境所导致的维护困难以及与现有基础设施的兼容性问题阻碍了其广泛采用。此外,缺乏能够管理和操作这些复杂系统的熟练专业人员也是另一个重大障碍。然而,卫星通讯的进步和对永续自动化技术的投资不断增加正在开闢新的成长途径,并为其中的一些障碍提供解决方案。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 94亿美元 |

| 预测值 | 195亿美元 |

| 复合年增长率 | 7.8% |

根据类型,市场分为通讯系统和控制系统。通讯系统领域在 2024 年占据 59.5% 的主导份额,并有望在 2034 年稳步成长。增强的连接解决方案(例如更快、更可靠的资料传输)正在推动这一领域的成长。这些进步对于确保顺利协调并实现船舶和岸基设施之间的即时资料共享对于改善海上作业至关重要。随着海上活动越来越依赖数位连接,对创新通讯解决方案的需求持续增长。

市场也根据平台细分为商业应用和国防应用。由于军事行动对安全、高效通讯系统的迫切需求,预计到 2034 年国防部门的复合年增长率将达到 8.5%。这些系统确保有效的协调和安全的资料传输,尤其是在高风险情境中。对国家安全的日益关注以及尖端技术与国防行动的融合是该领域快速增长的主要驱动力。

从地区来看,北美船舶船上通讯和控制系统市场规模预计到 2034 年将达到 75 亿美元。该地区的成长归因于控制系统采用自动化和人工智慧,从而提高了营运效率并最大限度地减少了人为干预。此外,卫星通讯技术的进步大大提高了偏远海洋地区的连结性,巩固了北美作为全球市场主要参与者的地位。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 自主船舶需求不断成长

- 物联网与人工智慧技术的融合

- 增加对智慧航运的投资

- 卫星通讯的进步

- 航运业数位化日益受关注

- 产业陷阱与挑战

- 初期投资高

- 与遗留系统集成

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 通讯系统

- 机载卫星通讯系统

- 无线电系统

- 机载宽频系统

- 其他通讯系统

- 控制系统

- 导航定位控制系统

- 引擎和推进控制系统

- 监控和监视控制系统

- 其他控制系统

第 6 章:市场估计与预测:按平台,2021-2034 年

- 主要趋势

- 商业的

- 客船

- 游艇

- 渡轮

- 邮轮

- 货船

- 货柜船

- 散货船

- 油轮

- 天然气运输车

- 干货船

- 驳船

- 其他船舶

- 专用船舶

- 近海船舶

- 研究船

- 客船

- 防御

- 航空母舰

- 护卫舰

- 护卫舰

- 潜水艇

- 驱逐舰

- 两栖舰船

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 原始设备製造商(OEM)

- 售后市场

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- ABB

- Emerson

- Furuno

- Honeywell

- Japan Radio

- Kongsberg

- L3Harris

- Navico

- Northrop Grumman

- Raymarine

- Saab

- ST Engineering

- Viasat

- Wartsila

The Global Marine Onboard Communication And Control Systems Market was valued at USD 9.4 billion in 2024 and is anticipated to grow at a CAGR of 7.8% between 2025 and 2034. This impressive growth trajectory is fueled by the increasing reliance on advanced technologies to optimize maritime operations. With the rapid evolution of global trade and heightened demand for safe, efficient maritime transportation, the adoption of state-of-the-art communication and control systems has become essential. These systems enable seamless coordination, real-time monitoring, and data exchange, ensuring operational safety and efficiency in the maritime sector. Furthermore, the industry is witnessing a shift toward eco-friendly innovations and satellite-based solutions, which are expected to revolutionize onboard communication and control processes.

Despite this promising outlook, the market faces challenges. High installation costs, maintenance difficulties due to harsh marine environments, and compatibility issues with existing infrastructure hinder widespread adoption. Additionally, the shortage of skilled professionals capable of managing and operating these sophisticated systems poses another significant hurdle. However, advancements in satellite communication and growing investments in sustainable, automated technologies are opening new avenues for growth, offering solutions to some of these barriers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.4 Billion |

| Forecast Value | $19.5 Billion |

| CAGR | 7.8% |

By type, the market is divided into communication systems and control systems. The communication systems segment held a dominant 59.5% share in 2024 and is poised to grow steadily through 2034. Enhanced connectivity solutions, such as faster and more reliable data transmission, are driving this segment's growth. These advancements are critical for improving maritime operations by ensuring smooth coordination and enabling real-time data sharing between vessels and shore-based facilities. As maritime activities become increasingly dependent on digital connectivity, the demand for innovative communication solutions continues to grow.

The market is also segmented based on platform into commercial and defense applications. The defense segment is expected to register a robust CAGR of 8.5% by 2034, driven by the critical need for secure, efficient communication systems in military operations. These systems ensure effective coordination and secure data transmission, especially in high-stakes scenarios. The increasing focus on national security and the integration of cutting-edge technologies within defense operations are key drivers for this segment's rapid growth.

Regionally, the North America marine onboard communication and control systems market is projected to reach USD 7.5 billion by 2034. The region's growth is attributed to the adoption of automation and artificial intelligence in control systems, which enhance operational efficiency and minimize human intervention. Additionally, advancements in satellite communication technologies have significantly improved connectivity in remote oceanic areas, solidifying North America's position as a major player in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for autonomous vessels

- 3.6.1.2 Integration of IoT and AI technologies

- 3.6.1.3 Increased investment in smart shipping

- 3.6.1.4 Advancements in satellite communication

- 3.6.1.5 Rising focus on maritime industry digitalization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investment

- 3.6.2.2 Integration with legacy systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Communication systems

- 5.2.1 Onboard satellite communication systems

- 5.2.2 Radio systems

- 5.2.3 Onboard broadband systems

- 5.2.4 Other communication systems

- 5.3 Control systems

- 5.3.1 Navigation and positioning control systems

- 5.3.2 Engine and propulsion control systems

- 5.3.3 Monitoring and surveillance control systems

- 5.3.4 Other control systems

Chapter 6 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Commercial

- 6.2.1 Passenger vessels

- 6.2.1.1 Yachts

- 6.2.1.2 Ferries

- 6.2.1.3 Cruise ships

- 6.2.2 Cargo vessels

- 6.2.2.1 Container vessels

- 6.2.2.2 Bulk carrier

- 6.2.2.3 Tankers

- 6.2.2.4 Gas tankers

- 6.2.2.5 Dry cargo ship

- 6.2.2.6 Barges

- 6.2.3 Other ships

- 6.2.3.1 Specialized vessels

- 6.2.3.2 Offshore vessels

- 6.2.3.3 Research vessels

- 6.2.1 Passenger vessels

- 6.3 Defense

- 6.3.1 Aircraft carrier

- 6.3.2 Corvettes

- 6.3.3 Frigates

- 6.3.4 Submarines

- 6.3.5 Destroyers

- 6.3.6 Amphibious ships

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Original Equipment Manufacturer (OEM)

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Emerson

- 9.3 Furuno

- 9.4 Honeywell

- 9.5 Japan Radio

- 9.6 Kongsberg

- 9.7 L3Harris

- 9.8 Navico

- 9.9 Northrop Grumman

- 9.10 Raymarine

- 9.11 Saab

- 9.12 ST Engineering

- 9.13 Viasat

- 9.14 Wartsila

全球联合全局指挥控制系统市场(按组件、通讯方式、平台、应用和最终用户划分)预测(2026-2032年)按组件、平台和应用分類的指挥控制系统市场 - 全球预测(2025-2032 年)船舶通讯与控制系统市场(依系统类型、船舶类型及安装类型划分)-2025-2032年全球预测

全球联合全局指挥控制系统市场(按组件、通讯方式、平台、应用和最终用户划分)预测(2026-2032年)按组件、平台和应用分類的指挥控制系统市场 - 全球预测(2025-2032 年)船舶通讯与控制系统市场(依系统类型、船舶类型及安装类型划分)-2025-2032年全球预测 2025年太空执法全球市场报告2025年全球船舶通讯与控制系统市场报告指挥与控制系统市场:2034 年市场机会与策略

2025年太空执法全球市场报告2025年全球船舶通讯与控制系统市场报告指挥与控制系统市场:2034 年市场机会与策略 指挥与控制系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

指挥与控制系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 指挥与控制系统市场规模、份额及成长分析(按组件、安装类型、平台类型、应用和地区)-2025 年至 2032 年产业预测

指挥与控制系统市场规模、份额及成长分析(按组件、安装类型、平台类型、应用和地区)-2025 年至 2032 年产业预测 指挥与控制系统市场 2025-2029

指挥与控制系统市场 2025-2029 命令与控制系统市场 - 全球产业规模、份额、趋势、机会和预测,按平台、解决方案、应用、地区和竞争细分,2020-2030 年

命令与控制系统市场 - 全球产业规模、份额、趋势、机会和预测,按平台、解决方案、应用、地区和竞争细分,2020-2030 年