|

市场调查报告书

商品编码

1685061

铠装电缆市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Armored Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

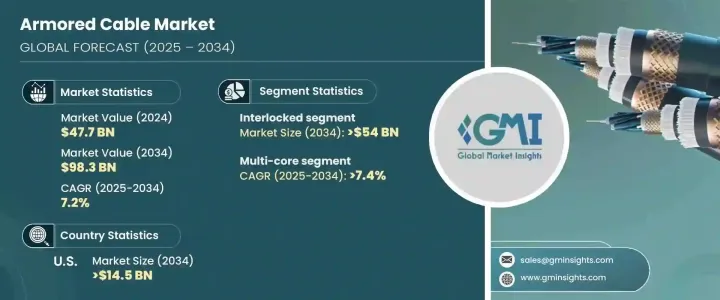

2024 年全球铠装电缆市场价值达到 477 亿美元,预估 2025 年至 2034 年期间复合年增长率为 7.2%。这种快速成长源于建筑、能源和製造等行业对安全、耐用和可靠的布线解决方案日益增长的需求。随着全球基础设施项目的加速推进,特别是在新兴经济体,铠装电缆因其出色的抵御机械损伤、恶劣天气条件和环境挑战的能力而受到青睐。

城市化以及住宅、商业和工业空间建设活动的增加进一步刺激了需求,特别是在易受不利环境条件影响的地区。此外,製造工艺的进步,包括更强大的材料和创新设计的集成,正透过提高电缆的耐用性和性能来促进市场发展。各行业对电气安全标准认识的不断提高也大大推动了铠装电缆的采用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 477亿美元 |

| 预测值 | 983亿美元 |

| 复合年增长率 | 7.2% |

随着各行各业转向可持续、高效的能源解决方案,对支持太阳能和风力发电场等再生能源专案的强大布线基础设施的需求日益加剧。铠装电缆因其即使在严苛的户外环境中也能提供安全可靠的电力传输的能力而得到越来越多的应用。此外,随着全球数位转型的推进,电信业正在采用铠装电缆来保护关键通讯网路免受物理损坏和干扰。技术、环境和工业因素的整合继续推动市场成长,使铠装电缆成为现代基础设施发展中不可或缺的组成部分。

预计到 2034 年,互锁铠装电缆市场将创收 540 亿美元,这得益于其机械保护性、灵活性和成本效益。互锁铠装电缆采用金属带缠绕电缆芯的设计,具有出色的抵抗物理损坏和外部压力的能力。这种设计使其非常适合建筑、工业设施和户外设施等电缆面临严峻条件的行业。它们的耐用性和可靠性使其成为需要增强机械强度的应用的必不可少的解决方案。

在核心类型类别中,多芯铠装电缆预计到 2034 年将以 7.4% 的复合年增长率成长。这些电缆在一条电缆内容纳多个电路,简化了安装并降低了整体专案成本,使其成为製造业、电信业和建筑业等行业的理想选择。它们能够支援有限空间内的高效配电和简化布线,这在空间优化和可靠性至关重要的环境中尤其有利。

受建筑、电信和能源等关键领域对先进电力基础设施投资不断增加的推动,美国铠装电缆市场预计到 2034 年将创收 145 亿美元。该国不断扩大的城市化进程,加上智慧城市计画的发展,进一步加速了对可靠布线解决方案的需求。此外,再生能源专案的成长,特别是太阳能和风能,为铠装电缆创造了新的机会,铠装电缆对于确保在恶劣的户外环境中安全传输电力至关重要。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第 5 章:市场规模及预测:依装甲类型,2021 – 2034 年

- 主要趋势

- 互锁

- 连续波纹焊接

第六章:市场规模及预测:依核心类型,2021 – 2034 年

- 主要趋势

- 单核

- 多核心

第 7 章:市场规模与预测:按最终用户,2021 – 2034 年

- 主要趋势

- 石油和天然气

- 製造业

- 矿业

- 建造

- 其他的

第 8 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- Anixter

- AT&T

- Atkore

- Belden

- Finolex

- Furukawa Electric

- Havells

- Helukabel

- KEI Industries

- Leoni Cables

- LS Cable & System

- Nexans

- NKT

- Okonite

- Omni Cables

- Polycab

- Prysmian

- Riyadh Cables

- RR Kabel

- Southwire

- Sumitomo Electric

The Global Armored Cable Market reached a valuation of USD 47.7 billion in 2024 and is projected to expand at a CAGR of 7.2% from 2025 to 2034. This rapid growth stems from the increasing need for secure, durable, and reliable wiring solutions across industries such as construction, energy, and manufacturing. As global infrastructure projects accelerate, particularly in emerging economies, armored cables are gaining traction due to their superior ability to withstand mechanical damage, harsh weather conditions, and environmental challenges.

Urbanization and the rise in construction activities for residential, commercial, and industrial spaces are further fueling demand, particularly in areas prone to adverse environmental conditions. Additionally, advancements in manufacturing processes, including the integration of stronger materials and innovative designs, are bolstering the market by enhancing cable durability and performance. Rising awareness of electrical safety standards across industries is also significantly driving the adoption of armored cables.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $47.7 Billion |

| Forecast Value | $98.3 Billion |

| CAGR | 7.2% |

As industries shift toward sustainable and efficient energy solutions, the need for robust wiring infrastructure to support renewable energy projects, such as solar and wind farms, is intensifying. Armored cables are increasingly being utilized for their ability to provide safe and reliable power transmission, even in demanding outdoor environments. Moreover, as digital transformation advances globally, the telecommunications sector is adopting armored cables for their capacity to protect critical communication networks from physical damage and interference. This confluence of technological, environmental, and industrial factors continues to drive market growth, positioning armored cables as an indispensable component in modern infrastructure development.

The interlocked armored cable segment is anticipated to generate USD 54 billion by 2034, driven by its mechanical protection, flexibility, and cost-effectiveness. Designed with a metal strip wrapped around the cable core, interlocked armored cables offer exceptional resistance to physical damage and external pressures. This design makes them highly suitable for industries such as construction, industrial facilities, and outdoor installations, where cables are subjected to challenging conditions. Their durability and reliability make them an essential solution for applications requiring enhanced mechanical strength.

In the core type category, multi-core armored cables are projected to grow at a CAGR of 7.4% through 2034. These cables, which house multiple electrical circuits within a single cable, simplify installation and reduce overall project costs, making them ideal for industries such as manufacturing, telecommunications, and construction. Their ability to support efficient power distribution and streamline wiring in confined spaces is particularly advantageous in environments where space optimization and reliability are critical.

The US armored cable market is expected to generate USD 14.5 billion by 2034, driven by growing investments in advanced electrical infrastructure across critical sectors such as construction, telecommunications, and energy. The country's expanding urbanization, coupled with the development of smart city projects, is further accelerating the demand for dependable wiring solutions. Additionally, the growth of renewable energy projects, particularly in solar and wind power, is creating new opportunities for armored cables, which are essential for ensuring safe power transmission in rugged and outdoor environments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Armor Type, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 5.1 Key trends

- 5.2 Interlocked

- 5.3 Continuously corrugated welded

Chapter 6 Market Size and Forecast, By Core Type, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 6.1 Key trends

- 6.2 Single core

- 6.3 Multi-core

Chapter 7 Market Size and Forecast, By End User, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Manufacturing

- 7.4 Mining

- 7.5 Construction

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Anixter

- 9.2 AT&T

- 9.3 Atkore

- 9.4 Belden

- 9.5 Finolex

- 9.6 Furukawa Electric

- 9.7 Havells

- 9.8 Helukabel

- 9.9 KEI Industries

- 9.10 Leoni Cables

- 9.11 LS Cable & System

- 9.12 Nexans

- 9.13 NKT

- 9.14 Okonite

- 9.15 Omni Cables

- 9.16 Polycab

- 9.17 Prysmian

- 9.18 Riyadh Cables

- 9.19 RR Kabel

- 9.20 Southwire

- 9.21 Sumitomo Electric

耐油电缆市场(按绝缘材料、电压、导体材料和应用)—2025-2030 年全球预测

耐油电缆市场(按绝缘材料、电压、导体材料和应用)—2025-2030 年全球预测 全球互锁铠装电缆市场全球多芯铠装电缆市场全球铠装电缆市场铠装电缆市场按铠装类型、安装类型、分销管道、最终用途行业划分 - 2025-2030 年全球预测

全球互锁铠装电缆市场全球多芯铠装电缆市场全球铠装电缆市场铠装电缆市场按铠装类型、安装类型、分销管道、最终用途行业划分 - 2025-2030 年全球预测 CCW 铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测石油和天然气铠装电缆市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测单芯铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测采矿铠装电缆市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测多芯铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

CCW 铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测石油和天然气铠装电缆市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测单芯铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测采矿铠装电缆市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测多芯铠装电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测