|

市场调查报告书

商品编码

1685084

马达起动器市场机会、成长动力、产业趋势分析和 2025 - 2034 年预测Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

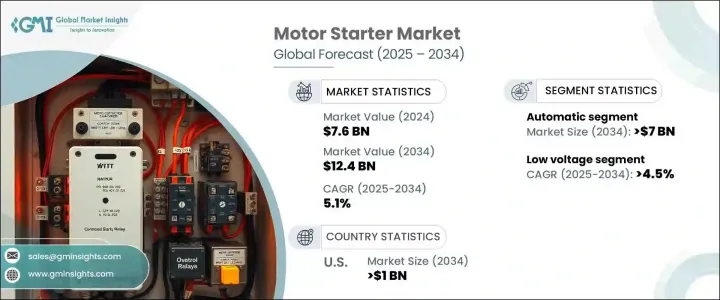

2024 年全球电动马达起动器市场价值为 76 亿美元,预计将稳定成长,2025 年至 2034 年的复合年增长率预计为 5.1%。这一增长可归因于工业自动化的快速应用,这导致了对更高效的电机控制和保护解决方案的需求。随着各行各业越来越关注能源效率和永续性,对先进马达起动器的需求激增。主要的市场驱动因素包括人们对具有远端监控、诊断和智慧控制功能的智慧型马达起动器的日益青睐,所有这些都大大提高了营运效率。

此外,将物联网 (IoT) 技术整合到电动马达起动器中的转变透过提高功能性、适应性和节能性彻底改变了市场。基于微处理器的控制、数位介面和即时监控功能等技术创新也在重塑该产业的未来。工业自动化加上环保意识预计将在未来几年推动对这些系统的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 76亿美元 |

| 预测值 | 124亿美元 |

| 复合年增长率 | 5.1% |

预计到 2034 年,自动电动马达起动器市场将创造 70 亿美元的收入。这一成长主要得益于小型工业和商业领域日益增长的需求,在这些领域,电动马达起动器对于高效和安全的电动马达运作至关重要。基于微处理器的技术和电子控制的结合增强了它们的吸引力,使企业能够最大限度地节省能源并降低营运成本。基础设施的不断扩张,加上全球製造活动的不断增加,将推动对这些高效且经济的解决方案的需求。

同时,预计到 2034 年低压电动马达起动器市场的复合年增长率将达到 4.5%。对节能降耗的电动马达起动器的需求不断增长是推动该产业发展的关键因素。低压启动器对于寻求实现永续发展目标同时最大限度减少能源浪费的行业尤其有价值。先进通讯协定、物联网连接和更环保的设计元素的整合使这一领域实现了强劲成长。人们对再生能源和永续实践的日益重视为低压起动器在从绿色建筑项目到智慧电网等多个行业中发挥重要作用提供了机会。

到 2034 年,美国电动马达起动器市场规模预计将达到 10 亿美元。製造技术的进步、自动化的广泛采用以及基础设施的现代化是这一增长的重要推动因素。此外,再生能源系统的整合和更严格的能源效率法规的实施,正在推动美国对先进马达控制解决方案的需求。随着各行各业寻求满足高能源标准和提高营运效率,电机起动器市场有望蓬勃发展,满足现代製造业和基础设施发展的需求。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第 5 章:市场规模与预测:依技术,2021 – 2034 年

- 主要趋势

- 手动的

- 自动的

第 6 章:市场规模与预测:按电压,2021 – 2034 年

- 主要趋势

- 低的

- 中等的

- 高的

第 7 章:市场规模及预测:依阶段,2021 – 2034 年

- 主要趋势

- 单相

- 三相

第 8 章:市场规模与预测:按应用,2021 – 2034 年

- 主要趋势

- 住宅

- 商业的

- 工业的

第 9 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 西班牙

- 荷兰

- 奥地利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 埃及

- 南非

- 奈及利亚

- 拉丁美洲

- 巴西

- 阿根廷

第十章:公司简介

- ABB

- C&S Electric

- CG Power & Industrial Solutions

- CHINT Group

- CORDYNE

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric

- General Electric

- Havells India

- Kalp Controls

- L&T Electrical & Automation

- LOVATO ELECTRIC

- Mitsubishi Electric

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-BENTEX GROUP

- WEG

The Global Motor Starter Market, valued at USD 7.6 billion in 2024, is expected to experience steady growth, with a projected CAGR of 5.1% from 2025 to 2034. This growth can be attributed to the rapid adoption of industrial automation, which has created a demand for more efficient motor control and protection solutions. As industries increasingly focus on energy efficiency and sustainability, the need for advanced motor starters has surged. Key market drivers include the growing preference for intelligent motor starters that offer remote monitoring, diagnostics, and smart controls, all of which significantly enhance operational efficiency.

Moreover, the shift towards integrating Internet of Things (IoT)-)-enabled technologies into motor starters have revolutionized the market by improving functionality, adaptability, and energy savings. Technological innovations like microprocessor-based controls, digital interfaces, and real-time monitoring features are also reshaping the industry's future. Industrial automation, coupled with environmental consciousness, is expected to propel demand for these systems in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 5.1% |

The automatic motor starter segment is anticipated to generate USD 7 billion in revenue through 2034. This growth is largely driven by the increasing demand from small-scale industries and the commercial sector, where motor starters are crucial for efficient and safe motor operations. The incorporation of microprocessor-based technologies and electronic controls enhances their appeal, allowing businesses to maximize energy savings and reduce operational costs. The ongoing expansion of infrastructure, coupled with rising manufacturing activities globally, will fuel the demand for these efficient and cost-effective solutions.

Meanwhile, the low-voltage motor starter segment is forecast to grow at a CAGR of 4.5% through 2034. The growing demand for energy-efficient motor starters with reduced power consumption is a key factor propelling this sector. Low-voltage starters are particularly valued in industries looking to meet sustainability goals while minimizing energy waste. The integration of advanced communication protocols, IoT connectivity, and more eco-conscious design elements positions this segment for strong growth. The increasing emphasis on renewable energy sources and sustainable practices presents an opportunity for low-voltage starters to play a significant role across multiple industries, from green building projects to smart grids.

The U.S. motor starter market is set to generate USD 1 billion by 2034. Advances in manufacturing technologies, the widespread adoption of automation, and the modernization of infrastructure are significant contributors to this growth. Additionally, the integration of renewable energy systems and the enforcement of stricter energy efficiency regulations are driving the demand for advanced motor control solutions in the U.S. As industries seek to meet high energy standards and improve operational efficiency, the market for motor starters is well-positioned to thrive, meeting the needs of modern manufacturing and infrastructure development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (Units & USD Million)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Automatic

Chapter 6 Market Size and Forecast, By Voltage, 2021 – 2034 (Units & USD Million)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Size and Forecast, By Phase, 2021 – 2034 (Units & USD Million)

- 7.1 Key trends

- 7.2 Single phase

- 7.3 Three phase

Chapter 8 Market Size and Forecast, By Application, 2021 – 2034 (Units & USD Million)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.4 Industrial

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (Units & USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.3.8 Austria

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.4.6 New Zealand

- 9.4.7 Indonesia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Egypt

- 9.5.5 South Africa

- 9.5.6 Nigeria

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABB

- 10.2 C&S Electric

- 10.3 CG Power & Industrial Solutions

- 10.4 CHINT Group

- 10.5 CORDYNE

- 10.6 Danfoss

- 10.7 Eaton

- 10.8 Emerson Electric

- 10.9 Fuji Electric

- 10.10 General Electric

- 10.11 Havells India

- 10.12 Kalp Controls

- 10.13 L&T Electrical & Automation

- 10.14 LOVATO ELECTRIC

- 10.15 Mitsubishi Electric

- 10.16 Rockwell Automation

- 10.17 Schneider Electric

- 10.18 Siemens

- 10.19 SKN-BENTEX GROUP

- 10.20 WEG