|

市场调查报告书

商品编码

1685179

动脉粥状硬化切除设备市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Atherectomy Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

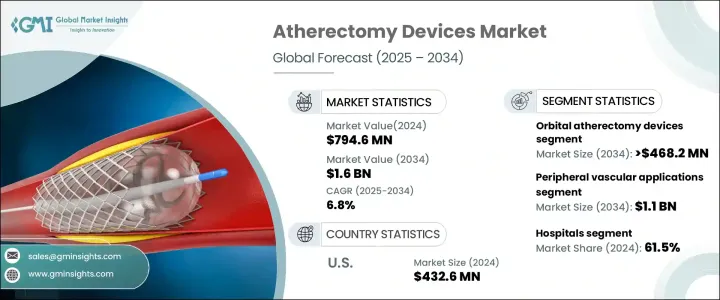

2024 年全球动脉粥状硬化切除设备市场规模达到 7.946 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 6.8%。週边动脉疾病 (PAD) 和冠状动脉疾病 (CAD) 盛行率的上升推动了对先进治疗方案的需求。随着老龄人口的增加和久坐生活方式的日益普遍,糖尿病和肥胖症病例激增,进一步推动了对微创手术的需求。医疗保健提供者正在寻求精准驱动的解决方案,以增强斑块去除效果,同时最大限度地减少併发症,使动脉粥状硬化切除设备成为心血管治疗的重要工具。

以患者为中心的医疗保健日益成为趋势,推动医院和医疗中心采用可改善临床结果的技术。与传统治疗方法相比,微创动脉粥状硬化斑块切除术可缩短恢復时间、减少住院时间并降低术后併发症的风险。这种转变正在促进医生和患者的更高采用率。持续的技术进步、监管部门的批准和正在进行的临床试验正在增强人们对这些设备的信心,为其更广泛的应用铺平道路。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7.946 亿美元 |

| 预测值 | 16亿美元 |

| 复合年增长率 | 6.8% |

不断成长的研发投入也推动了市场扩张。各公司正在推出具有卓越效率、精准度和安全性的创新动脉粥状硬化切除系统。自动化和人工智慧整合设备正在涌现,使临床医生能够优化治疗方法,同时缩短手术时间。优惠的报销政策和不断增加的门诊心血管手术数量进一步推动了市场成长。随着医疗机构优先考虑具有高成功率且经济有效的解决方案,动脉粥状硬化斑块切除设备的使用势头持续增强。

根据产品类型,市场分为轨道式、雷射式、定向式和旋转式动脉粥状硬化切除术设备。眼眶动脉粥状硬化切除设备将经历大幅成长,预计到 2034 年市场价值将达到 4.682 亿美元,复合年增长率为 6.6%。这些装置利用高速旋转的冠或钻头去除斑块同时保持动脉完整性,从而提高了程序的准确性。他们在治疗週边动脉和冠状动脉方面的持续成功使他们成为处理复杂病例的医疗保健专业人员的首选。随着医院和外科中心优先考虑创新有效的治疗方案,对眼眶动脉粥状硬化切除设备的需求持续上升。

根据应用,市场分为週边血管和冠状动脉手术。预计週边血管领域将大幅扩张,到 2034 年将达到 11 亿美元,复合年增长率为 6.3%。週边动脉疾病严重影响活动能力和生活质量,迫切需要有效的治疗替代方案。与传统手术相比,动脉粥状硬化斑块切除术具有显着的优势,包括恢復期短、併发症少、住院时间短。随着对这些益处的认识不断提高,越来越多的患者和医疗保健提供者选择微创干预,从而增加了对动脉粥状硬化切除设备的需求。

2024 年美国动脉粥状硬化切除设备市场规模为 4.326 亿美元,预计 2025 年至 2034 年的复合年增长率为 6.2%。美国週边动脉疾病 (PAD) 和冠状动脉疾病 (CAD) 等心血管疾病负担日益加重,推动了对先进治疗方案的需求。老年人口的不断增长,加上肥胖和糖尿病的高发生率,进一步加速了市场的成长。医疗机构越来越多地采用先进的动脉粥状硬化切除设备,以提高手术精度、改善患者安全性并确保更快的康復。随着对微创心血管手术的需求不断增长,美国市场预计将在全球保持主导地位。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 微创手术的受欢迎程度增加

- 目标患者群体不断增长

- 最近的技术进步

- 週边动脉疾病盛行率上升

- 产业陷阱与挑战

- 产品成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 报销场景

- 技术格局

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 眼眶动脉粥状硬化切除装置

- 雷射旋切设备

- 定向旋切装置

- 旋磨装置

第 6 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 週边血管应用

- 冠状动脉应用

第 7 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用户

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- angiodynamics

- AVINGER

- B. Braun

- BD (Becton, Dickinson and Company)

- BIOMERICS

- Boston Scientific

- Cardinal Health

- Cardiovascular Systems

- Cordis

- Philips

- Medtronic

- Nipro

- Rex Medical

- TERUMO

The Global Atherectomy Devices Market reached USD 794.6 million in 2024 and is projected to grow at a CAGR of 6.8% between 2025 and 2034. The rising prevalence of peripheral artery disease (PAD) and coronary artery disease (CAD) is fueling demand for advanced treatment solutions. As aging populations increase and sedentary lifestyles become more common, cases of diabetes and obesity are surging, further driving the need for minimally invasive procedures. Healthcare providers are seeking precision-driven solutions to enhance plaque removal while minimizing complications, making atherectomy devices an essential tool in cardiovascular treatment.

The increasing shift toward patient-centric healthcare is pushing hospitals and medical centers to adopt technologies that improve clinical outcomes. Minimally invasive atherectomy procedures offer faster recovery times, reduced hospital stays, and lower risks of post-surgical complications compared to traditional treatment methods. This shift is encouraging higher adoption rates among physicians and patients. Continuous technological advancements, regulatory approvals, and ongoing clinical trials are strengthening confidence in these devices, paving the way for their broader implementation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $ 794.6 Million |

| Forecast Value | $ 1.6 Billion |

| CAGR | 6.8% |

Market expansion is also being driven by growing investment in research and development. Companies are introducing innovative atherectomy systems that provide superior efficiency, precision, and safety. Automated and AI-integrated devices are emerging, allowing clinicians to optimize treatment approaches while reducing procedure times. Favorable reimbursement policies and an increasing number of outpatient cardiovascular procedures are further propelling market growth. As medical institutions prioritize cost-effective solutions that deliver high success rates, atherectomy devices continue to gain momentum.

By product type, the market is segmented into orbital, laser, directional, and rotational atherectomy devices. Orbital atherectomy devices are set to experience substantial growth, with market value expected to reach USD 468.2 million by 2034 at a CAGR of 6.6%. These devices improve procedural accuracy by utilizing a high-speed spinning crown or burr to remove plaque while preserving arterial integrity. Their consistent success in treating both peripheral and coronary arteries has positioned them as a preferred choice among healthcare professionals managing complex cases. As hospitals and surgical centers prioritize innovative and efficient treatment options, the demand for orbital atherectomy devices continues to rise.

Based on application, the market is divided into peripheral vascular and coronary procedures. The peripheral vascular segment is expected to expand significantly, projected to reach USD 1.1 billion by 2034 at a CAGR of 6.3%. Peripheral artery disease severely impacts mobility and quality of life, creating an urgent need for effective treatment alternatives. Atherectomy procedures offer notable advantages, including reduced recovery periods, fewer complications, and shorter hospital stays compared to traditional surgery. As awareness of these benefits grows, more patients and healthcare providers are opting for minimally invasive interventions, boosting the demand for atherectomy devices.

The U.S. atherectomy devices market accounted for USD 432.6 million in 2024 and is anticipated to grow at a CAGR of 6.2% from 2025 to 2034. The country's increasing burden of cardiovascular diseases, including PAD and CAD, is driving demand for advanced treatment solutions. A growing elderly population, coupled with high obesity and diabetes rates, is further accelerating market growth. Medical institutions are increasingly adopting cutting-edge atherectomy devices that enhance procedural precision, improve patient safety, and ensure faster recoveries. As the demand for minimally invasive cardiovascular procedures rises, the U.S. market is expected to maintain its dominant position in the global landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in preference for minimally invasive procedures

- 3.2.1.2 Growing target patient population

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Rising prevalence of peripheral arterial diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the products

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Orbital atherectomy devices

- 5.3 Laser atherectomy devices

- 5.4 Directional atherectomy devices

- 5.5 Rotational atherectomy devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular applications

- 6.3 Coronary applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 angiodynamics

- 9.3 AVINGER

- 9.4 B. Braun

- 9.5 BD (Becton, Dickinson and Company)

- 9.6 BIOMERICS

- 9.7 Boston Scientific

- 9.8 Cardinal Health

- 9.9 Cardiovascular Systems

- 9.10 Cordis

- 9.11 Philips

- 9.12 Medtronic

- 9.13 Nipro

- 9.14 Rex Medical

- 9.15 TERUMO

斑块改良设备市场:市场洞察、竞争格局及市场预测(至2034年)

斑块改良设备市场:市场洞察、竞争格局及市场预测(至2034年) 2026年全球冠状动脉动脉粥状硬化斑块切除术器械市场报告2026年全球动脉粥状硬化斑块切除术器械市场报告2026年全球斑块改良设备市场报告2026年全球雷射动脉动脉粥状硬化斑块切除术设备市场报告

2026年全球冠状动脉动脉粥状硬化斑块切除术器械市场报告2026年全球动脉粥状硬化斑块切除术器械市场报告2026年全球斑块改良设备市场报告2026年全球雷射动脉动脉粥状硬化斑块切除术设备市场报告 血管内旋转斑块动脉粥状硬化斑块切除术装置市场(按产品类型、技术、应用和最终用户划分),全球预测(2026-2032)

血管内旋转斑块动脉粥状硬化斑块切除术装置市场(按产品类型、技术、应用和最终用户划分),全球预测(2026-2032) 动脉动脉粥状硬化斑块切除术器械市场规模、份额和成长分析(按产品、应用、最终用户和地区划分)—产业预测(2026-2033 年)

动脉动脉粥状硬化斑块切除术器械市场规模、份额和成长分析(按产品、应用、最终用户和地区划分)—产业预测(2026-2033 年) 全球动脉粥状斑块切除器材市场-产业规模、份额、趋势、机会和预测,依产品、应用、最终用户、地区和竞争格局划分,2020-2030年预测动脉粥状硬化斑块切除术器材:市场洞察、竞争格局及预测(至 2032 年)动脉动脉粥状硬化斑块切除术器械市场:2025-2032年全球预测(按器械类型、应用、最终用户和方式划分)

全球动脉粥状斑块切除器材市场-产业规模、份额、趋势、机会和预测,依产品、应用、最终用户、地区和竞争格局划分,2020-2030年预测动脉粥状硬化斑块切除术器材:市场洞察、竞争格局及预测(至 2032 年)动脉动脉粥状硬化斑块切除术器械市场:2025-2032年全球预测(按器械类型、应用、最终用户和方式划分)