|

市场调查报告书

商品编码

1685188

内分泌检测市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Endocrine Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

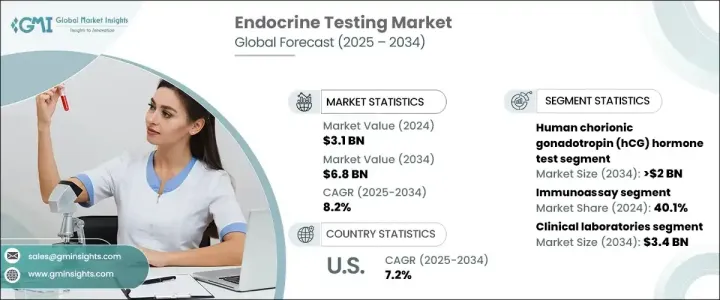

2024 年全球内分泌检测市场价值为 31 亿美元,预计将大幅成长,预计 2025 年至 2034 年的复合年增长率为 8.2%。推动这一增长的因素有很多,包括内分泌疾病患病率上升、常规健康检查意识增强,以及政府支持的旨在改善医疗保健可及性的倡议。人们对预防性医疗保健的日益重视导致对内分泌测试的需求激增,特别是对于管理糖尿病和甲状腺疾病等慢性病的个人而言。

诊断工具的技术进步和检测服务的改善正在进一步加速市场扩张。即时诊断和个人化医疗解决方案等创新检测方法的整合也正在重塑医疗格局,使内分泌检测更加方便、高效。由于全球医疗保健系统优先考虑内分泌相关疾病的早期发现和管理,预计市场在预测期内将实现持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 31亿美元 |

| 预测值 | 68亿美元 |

| 复合年增长率 | 8.2% |

在各种测试类型中,人类绒毛膜促性腺激素 (hCG) 测试预计将以 7.6% 的复合年增长率增长,到 2034 年将达到 20 亿美元。 hCG 测试广泛用于妊娠检测,因其准确性和易用性而受到青睐。这些测试可在临床环境和家庭环境中轻鬆使用,对于寻求可靠妊娠确认的个人来说是一种方便的选择。这些测试的日益普及反映了对用户友好且精确的诊断解决方案日益增长的需求。

市场按最终用途进行细分,其中临床实验室在 2024 年占据最大份额。预计到 2034 年,该细分市场将达到 34 亿美元。临床实验室配备了先进的诊断技术并配备了熟练的专业人员,使其成为准确荷尔蒙检测的首选。这些机构专门为糖尿病、甲状腺功能障碍和肾上腺疾病等需要详细而精确的检测的疾病提供全面的诊断服务。临床实验室提供的专业知识和可靠性继续推动其在市场上占据主导地位。

美国内分泌检测市场在 2024 年创下了 12 亿美元的产值,预计到 2034 年将以 7.2% 的复合年增长率成长。领先的诊断公司和实验室提供最先进的检测解决方案,支持了美国市场的成长。政府旨在解决慢性病和促进预防保健的措施进一步促进了市场的扩张。此外,即时诊断和个人化医疗解决方案的日益普及正在推动全国对内分泌检测的需求。随着对早期诊断和客製化治疗方案的关注度不断提高,预计美国市场将继续成为全球内分泌检测产业的主要贡献者。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 糖尿病、甲状腺疾病和肥胖症盛行率不断上升

- 政府支持性资金倡议

- 技术进步

- 日常健康监测意识不断增强

- 产业陷阱与挑战

- 测试技术开发成本高

- 缺乏意识

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 报销场景

- 差距分析

- 波特的分析

- PESTEL 分析

- 未来市场趋势

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第 5 章:市场估计与预测:按测试类型,2021 - 2034 年

- 主要趋势

- 人类绒毛膜促性腺激素 (hCG) 检测

- 促甲状腺激素 (TSH) 检测

- 胰岛素测试

- 黄体酮检测

- 黄体生成素 (LH) 检测

- 催乳素测试

- 其他测试类型

第六章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 免疫分析

- 质谱

- 色谱法

- 基于核酸

- 其他技术

第 7 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 临床实验室

- 医院

- 诊断中心

- 其他最终用途

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- Agilent

- BECKMAN COULTER

- BIO RAD

- biomedical TECHNOLOGIES

- BIOMERIEUX

- DH TECH

- Diasorin

- labcorp

- QuidelOrtho

- QIAGEN

- Quest Diagnostics

- Roche

- SCIEX

- SIEMENS Healthineers

- Thermo Fisher SCIENTIFIC

The Global Endocrine Testing Market, valued at USD 3.1 billion in 2024, is poised for significant growth, with a projected CAGR of 8.2% from 2025 to 2034. This growth is driven by several factors, including the rising prevalence of endocrine disorders, increasing awareness of routine health check-ups, and government-backed initiatives aimed at improving healthcare accessibility. The growing emphasis on preventive healthcare has led to a surge in demand for endocrine tests, particularly among individuals managing chronic conditions such as diabetes and thyroid disorders.

Technological advancements in diagnostic tools and improved access to testing services are further accelerating market expansion. The integration of innovative testing methods, such as point-of-care diagnostics and personalized healthcare solutions, is also reshaping the landscape, making endocrine testing more accessible and efficient. As healthcare systems worldwide prioritize early detection and management of endocrine-related conditions, the market is expected to witness sustained growth over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $6.8 Billion |

| CAGR | 8.2% |

Among the various test types, the human chorionic gonadotropin (hCG) hormone test is anticipated to grow at a CAGR of 7.6%, reaching USD 2 billion by 2034. Widely used for pregnancy detection, hCG tests are favored for their accuracy and ease of use. These tests are readily available in both clinical settings and for at-home use, making them a convenient option for individuals seeking reliable pregnancy confirmation. The increasing adoption of these tests reflects the growing demand for user-friendly and precise diagnostic solutions.

The market is segmented by end-use, with clinical laboratories holding the largest share in 2024. This segment is projected to reach USD 3.4 billion by 2034. Clinical laboratories are equipped with advanced diagnostic technologies and staffed by skilled professionals, making them the preferred choice for accurate hormone testing. These facilities specialize in comprehensive diagnostic services for conditions such as diabetes, thyroid dysfunction, and adrenal disorders, which require detailed and precise testing. The expertise and reliability offered by clinical laboratories continue to drive their dominance in the market.

The U.S. endocrine testing market generated USD 1.2 billion in 2024 and is forecast to grow at a CAGR of 7.2% through 2034. The presence of leading diagnostic firms and laboratories offering state-of-the-art testing solutions supports the market's growth in the United States. Government initiatives aimed at addressing chronic illnesses and promoting preventive care further contribute to the market's expansion. Additionally, the increasing adoption of point-of-care testing and personalized healthcare solutions is driving demand for endocrine testing across the country. As the focus on early diagnosis and tailored treatment options intensifies, the U.S. market is expected to remain a key contributor to the global endocrine testing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of diabetes, thyroid, and obesity

- 3.2.1.2 Supportive government funding initiatives

- 3.2.1.3 Technological advancements

- 3.2.1.4 Growing awareness of routine health monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost for the development of testing technologies

- 3.2.2.2 Lack of awareness

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Human chorionic gonadotropin (hCG) hormone test

- 5.3 Thyroid stimulating hormone (TSH) test

- 5.4 Insulin test

- 5.5 Progesterone test

- 5.6 Luteinizing hormone (LH) test

- 5.7 Prolactin test

- 5.8 Other test types

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoassay

- 6.3 Mass spectroscopy

- 6.4 Chromatography

- 6.5 Nucleic acid based

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical laboratories

- 7.3 Hospitals

- 7.4 Diagnostic centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Agilent

- 9.3 BECKMAN COULTER

- 9.4 BIO RAD

- 9.5 biomedical TECHNOLOGIES

- 9.6 BIOMERIEUX

- 9.7 DH TECH

- 9.8 Diasorin

- 9.9 labcorp

- 9.10 QuidelOrtho

- 9.11 QIAGEN

- 9.12 Quest Diagnostics

- 9.13 Roche

- 9.14 SCIEX

- 9.15 SIEMENS Healthineers

- 9.16 Thermo Fisher SCIENTIFIC

内分泌检测市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终使用者、设备、流程、安装类型及解决方案划分

内分泌检测市场分析及预测(至2035年):依类型、产品类型、服务、技术、应用、最终使用者、设备、流程、安装类型及解决方案划分 瘦素检测套组市场按产品类型、检测类型、技术类型、最终用户、应用和分销管道划分,全球预测(2026-2032年)

瘦素检测套组市场按产品类型、检测类型、技术类型、最终用户、应用和分销管道划分,全球预测(2026-2032年) 内分泌检测市场-全球产业规模、份额、趋势、机会和预测,按检测类型、技术、最终用户、地区和竞争格局划分,2020-2030年预测抗苗勒氏管激素检测市场:按产品、组件、应用和最终用户划分 - 全球预测(2025-2032 年)

内分泌检测市场-全球产业规模、份额、趋势、机会和预测,按检测类型、技术、最终用户、地区和竞争格局划分,2020-2030年预测抗苗勒氏管激素检测市场:按产品、组件、应用和最终用户划分 - 全球预测(2025-2032 年) 2025年全球内分泌检测市场报告2025年内分泌胜肽检测全球市场报告

2025年全球内分泌检测市场报告2025年内分泌胜肽检测全球市场报告 内分泌检测市场报告(按检测类型、技术、最终用途和地区)2025-2033

内分泌检测市场报告(按检测类型、技术、最终用途和地区)2025-2033 全球动物内分泌学市场

全球动物内分泌学市场 兽医内分泌学市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

兽医内分泌学市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 内分泌检测产品市场:依产品类型、技术、适应症、最终用户和地区划分

内分泌检测产品市场:依产品类型、技术、适应症、最终用户和地区划分