|

市场调查报告书

商品编码

1685207

防火材料市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Fire Stopping Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

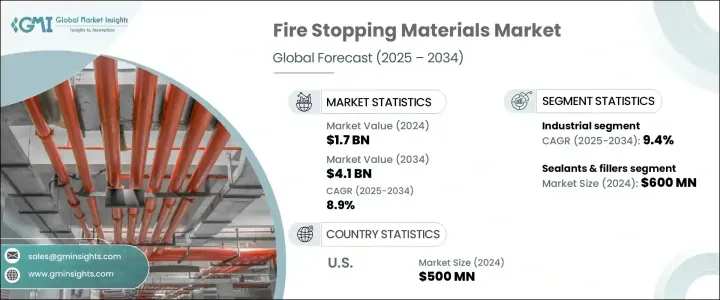

2024 年全球防火材料市场规模达到 17 亿美元,预计将经历强劲成长,2025 年至 2034 年的复合年增长率为 8.9%。推动这一市场扩张的几个关键因素包括加强消防安全法规、建筑活动激增以及全球城市化和工业化速度的加速。此外,防火技术的进步和消防安全意识的提高进一步推动了各行业对防火材料的需求。石油和天然气、航太、海洋和资料中心等行业对这些材料的需求尤其突出,因为这些行业的营运风险较高,因此都有严格的消防安全要求。

儘管成长轨迹看好,但市场仍面临重大挑战。主要障碍之一是先进防火解决方案的成本高昂,这可能会阻碍其采用,尤其是对于中小型企业而言。不同地区之间监管框架不一致的问题也使製造商和最终用户的合规工作变得复杂。供应链中断和替代材料的竞争(可提供更低的初始成本)进一步增加了市场的复杂性。建筑业放缓和技术劳动力持续短缺等经济不确定性也对实现市场持续成长构成挑战。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17亿美元 |

| 预测值 | 41亿美元 |

| 复合年增长率 | 8.9% |

防火材料领域,特别是密封剂和填料类别,在 2024 年的市场规模为 6 亿美元,预计到 2034 年的复合年增长率将达到 9.4%。密封剂和填料的创新是这一增长的关键,製造商不断开发性能更强、更易于使用、更耐用的产品。膨胀型密封剂越来越受欢迎,因为它们在高温下膨胀,能够有效密封缝隙,防止火势蔓延。防火砂浆也发挥着至关重要的作用,特别是在密封防火墙和地板上的电缆、管道和管子周围的大开口时,从而满足商业和工业环境中日益增长的防火需求。

工业部门在 2024 年占据了防火材料市场的 49%,预计在 2025 年至 2034 年期间的复合年增长率为 9.4%。这一增长是由石油和天然气设施、化工厂和製造基地等高风险环境中严格的消防安全法规所推动的。由于存在易燃化学品、气体和重型机械,在这些操作中防止火势蔓延至关重要。随着这些行业的不断扩大,对防火材料的需求只会增加。

在美国,防火材料市场在 2024 年创收 5 亿美元,预计到 2034 年将以 9.2% 的复合年增长率成长。该国的成长归因于更严格的消防安全标准、蓬勃发展的建筑业以及被动防火技术的不断进步。对改造、翻新和保护关键基础设施的关注进一步支持了该地区市场的强劲上升趋势。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算。

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 更严格的消防安全规定

- 建设、都市化和工业化进程加快

- 产业陷阱与挑战

- 防火材料成本高

- 熟练劳动力不足

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 涂料

- 密封剂和填料

- 硅酮密封胶

- 丙烯酸密封剂

- 膨胀密封剂

- 其他(水泥填料等)

- 板材

- 矿棉板

- 膨胀板材

- 复合板

- 其他(石膏板等)

- 腻子和泡沫

- 膨胀腻子

- 防火泡沫

- 膨胀泡沫

- 其他(腻子垫等)

- 其他(项圈、火块等)

第 6 章:市场估计与预测:按产品类型,2021-2034 年

- 主要趋势

- 被动防火

- 主动防火

第 7 章:市场估计与预测:按防火等级,2021 年至 2034 年

- 主要趋势

- 1小时额定

- 2 小时额定

- 3 小时额定

- 4 小时额定

- 额定时间超过 4 小时

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 电力

- 机械的

- 管道

- 其他的

第 9 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 住宅

- 商业的

- 工业的

- 石油和天然气

- 汽车

- 製造业

- 资料中心

- 其他(汽车、船等)

第 10 章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 直接销售

- 间接销售

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 12 章:公司简介

- 3M

- Bostik

- Emseal Joint Systems

- Everkem

- Flame Stop

- Fosroc

- HB Fuller Company

- Hilti

- Promat

- RectorSeal

- Rockwool

- Sika

- Specified Technologies

- Tremco

- Unique Fire Stop Products

The Global Fire Stopping Materials Market reached USD 1.7 billion in 2024 and is projected to experience robust growth, with a CAGR of 8.9% from 2025 to 2034. Several key factors are driving this market expansion, including tightening fire safety regulations, a surge in construction activities, and the increasing rate of urbanization and industrialization worldwide. Additionally, advancements in fire stopping technologies and heightened awareness surrounding fire safety further fuel the demand for fire stopping materials across various sectors. The need for these materials is especially prominent in industries such as oil and gas, aerospace, marine, and data centers, all of which have strict fire safety requirements due to the high-risk nature of their operations.

Despite the promising growth trajectory, the market faces significant challenges. One of the primary hurdles is the high cost associated with advanced fire stopping solutions, which can inhibit adoption, particularly for small and medium-sized enterprises. There is also the issue of inconsistent regulatory frameworks across different regions, which complicates compliance for manufacturers and end-users alike. Supply chain disruptions and competition from alternative materials, which can offer lower initial costs, further add to the market's complexities. Economic uncertainties, such as slowdowns in the construction industry and the ongoing shortage of skilled labor, also pose challenges to achieving consistent growth in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 8.9% |

The fire stopping materials segment, specifically the sealants and fillers category, accounted for USD 600 million in 2024 and is expected to grow at a CAGR of 9.4% through 2034. Innovation in sealants and fillers has been key to this growth, with manufacturers continuously developing products that offer enhanced performance, easier application, and greater durability. Intumescent sealants, in particular, are gaining popularity as they expand under high temperatures to effectively seal gaps and prevent the spread of fire. Firestopping mortars also play a crucial role, particularly in sealing large openings around cables, ducts, and pipes in fire-rated walls and floors, thereby addressing the growing demand for fire protection in commercial and industrial settings.

The industrial sector, which accounted for 49% of the fire stopping materials market in 2024, is projected to grow at a CAGR of 9.4% between 2025 and 2034. This growth is driven by stringent fire safety regulations in high-risk environments such as oil and gas facilities, chemical plants, and manufacturing sites. The need to prevent fire spread in these operations is critical due to the presence of flammable chemicals, gases, and heavy machinery. As these industries continue to expand, the demand for fire stopping materials will only increase.

In the U.S., the fire stopping materials market generated USD 500 million in 2024 and is expected to grow at a CAGR of 9.2% through 2034. The country's growth is attributed to stricter fire safety standards, a booming construction industry, and ongoing advancements in passive fire protection technologies. The focus on retrofitting, renovations, and protecting critical infrastructure further supports the strong upward trend of the market in the region.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Stricter fire safety regulations

- 3.6.1.2 Increased construction, urbanization, and industrialization

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of fire stopping materials

- 3.6.2.2 Inadequate skilled labor

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Coatings

- 5.3 Sealants & fillers

- 5.3.1 Silicone-based sealants

- 5.3.2 Acrylic sealants

- 5.3.3 Intumescent sealants

- 5.3.4 Others (cementitious fillers etc.)

- 5.4 Sheets & boards

- 5.4.1 Mineral wool boards

- 5.4.2 Intumescent sheets

- 5.4.3 Composite boards

- 5.4.4 Others (gypsum-based boards etc.)

- 5.5 Putty & foam

- 5.5.1 Intumescent putty

- 5.5.2 Fire-rated foam

- 5.5.3 Expanding foam

- 5.5.4 Others (putty pads etc.)

- 5.6 Others (collars, fire blocks etc.)

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Passive fire protection

- 6.3 Active fire protection

Chapter 7 Market Estimates & Forecast, By Fire Rating, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 1-hour rated

- 7.3 2-hour rated

- 7.4 3-hour rated

- 7.5 4-hour rated

- 7.6 More than 4-hour rated

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Electrical

- 8.3 Mechanical

- 8.4 Plumbing

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.4 Industrial

- 9.4.1 Oil & gas

- 9.4.2 Automotive

- 9.4.3 Manufacturing

- 9.4.4 Data centers

- 9.4.5 Others (automotive, marine etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 3M

- 12.2 Bostik

- 12.3 Emseal Joint Systems

- 12.4 Everkem

- 12.5 Flame Stop

- 12.6 Fosroc

- 12.7 H. B. Fuller Company

- 12.8 Hilti

- 12.9 Promat

- 12.10 RectorSeal

- 12.11 Rockwool

- 12.12 Sika

- 12.13 Specified Technologies

- 12.14 Tremco

- 12.15 Unique Fire Stop Products

建筑领域消防材料市场:依产品类型、材料成分、应用、最终用途及通路划分-2025-2032年全球预测消防材料市场依产品类型和市场状况划分-全球预测(2025-2032年)消防材料市场:按类型、材料、最终用途和分销管道划分-2025-2032年全球预测

建筑领域消防材料市场:依产品类型、材料成分、应用、最终用途及通路划分-2025-2032年全球预测消防材料市场依产品类型和市场状况划分-全球预测(2025-2032年)消防材料市场:按类型、材料、最终用途和分销管道划分-2025-2032年全球预测 全球被动防火材料市场

全球被动防火材料市场 防火材料市场 - 预测 2025-2030全球防火材料市场

防火材料市场 - 预测 2025-2030全球防火材料市场 2025年全球防火材料市场报告全球建筑防火材料市场报告(2025年)全球不燃覆层市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球被动防火材料市场规模(按类型、应用、地区、范围和预测)

2025年全球防火材料市场报告全球建筑防火材料市场报告(2025年)全球不燃覆层市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)全球被动防火材料市场规模(按类型、应用、地区、范围和预测)