|

市场调查报告书

商品编码

1685213

电气绝缘材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Electrical Insulation Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

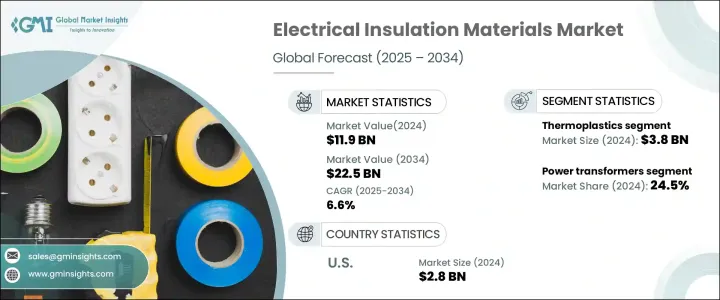

2024 年全球电气绝缘材料市场规模将达到 119 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 6.6%。这一成长是由各行各业对高效、可靠和安全电气系统日益增长的需求所推动的。电气绝缘材料在商业和工业应用中保护电气元件、确保使用寿命以及提高系统性能方面发挥关键作用。

随着产业的发展,对创新、耐用和可持续的绝缘解决方案的需求日益增加,以满足更严格的法规和性能标准。材料技术的进步以及对能源效率和永续性的日益重视进一步推动了需求。基础设施的持续扩张,特别是再生能源和现代化电网,也为积极的市场前景做出了贡献。随着人们不断向环保解决方案转变,製造商正致力于提供不仅能提高性能而且对环境负责的产品。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 119亿美元 |

| 预测值 | 225亿美元 |

| 复合年增长率 | 6.6% |

根据材料类型,市场细分包括热固性塑胶、玻璃纤维、云母、陶瓷、热塑性塑胶、纤维素、棉花等。 2024 年,热塑性塑胶部门的收入为 38 亿美元。热固性塑料以其出色的耐用性和耐高温性而闻名,使其成为要求苛刻的应用中的热门选择。陶瓷因其优异的介电性能而备受推崇,非常适合高压操作,而玻璃纤维则具有强度和出色的绝缘能力。云母仍然是高压环境中的首选材料,既具有耐热性又具有电气保护性。此外,纤维素和棉花正在成为具有防火特性的环保材料,符合电气领域可持续和安全解决方案日益增长的趋势。

电气绝缘材料的应用范围非常广泛,服务于电力变压器、配电变压器、电动马达和发电机、电线电缆、开关设备、电池和断路器等行业。电力变压器在 2024 年占据了 24.5% 的市场份额,预计到 2034 年将保持强劲成长。绝缘材料对于优化配电变压器和电动马达的性能和效率至关重要,将进一步推动发电、输电和工业自动化等关键领域的需求。

在美国,电气绝缘材料市场规模将在 2024 年达到 28 亿美元,并且由于基础设施的大量投资,预计将大幅成长。对过时的电网进行现代化改造和扩大再生能源计划正在推动先进绝缘材料的采用。透过专注于永续性和节能解决方案,美国将继续成为区域市场的主要参与者,确保在整个预测期内持续成长。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 汽车产业需求不断成长

- 航太应用的采用率不断提高

- 不断增长的化学加工工业

- 产业陷阱与挑战

- 电气绝缘材料成本高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场规模及预测:按材料,2021-2034 年

- 主要趋势

- 氟碳弹性体 (FKM)

- 全电绝缘材料(FFKM)

第 6 章:市场规模与预测:按应用,2021-2034 年

- 主要趋势

- 密封件和垫圈

- O 型环

- 软管和管子

- 其他的

第 7 章:市场规模与预测:依最终用途产业,2021-2034 年

- 主要趋势

- 汽车

- 航太

- 石油和天然气

- 化学加工

第 8 章:市场规模与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- 3M

- AGC (Asahi Glass)

- Chemours

- Daikin Industries

- DowDuPont

- DuPont (EI du Pont de Nemours and Company)

- Gujarat Fluorochemicals

- HaloPolymer

- Mitsui Chemicals

- Momentive Performance Materials

- Saint-Gobain Performance Plastics

- Shin-Etsu Chemical

- Solvay

- Wacker Chemie

- Zeon Corporation

The Global Electrical Insulation Materials Market reached USD 11.9 billion in 2024 and is set to expand at a CAGR of 6.6% from 2025 to 2034. This growth is driven by the increasing demand for efficient, reliable, and safe electrical systems across various industries. Electrical insulation materials play a critical role in protecting electrical components, ensuring longevity, and enhancing system performance in both commercial and industrial applications.

As industries evolve, there is a rising need for innovative, durable, and sustainable insulation solutions to meet stricter regulations and performance standards. Advancements in material technology, along with a growing emphasis on energy efficiency and sustainability, are further fueling demand. The continued expansion of infrastructure, particularly in renewable energy and modernized electrical grids, is also contributing to the positive market outlook. With the ongoing shift toward eco-friendly solutions, manufacturers are focusing on providing products that not only improve performance but are also environmentally responsible.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.9 Billion |

| Forecast Value | $22.5 Billion |

| CAGR | 6.6% |

Based on material type, the market segments include thermosets, fiberglass, mica, ceramics, thermoplastics, cellulose, cotton, and others. In 2024, the thermoplastics segment generated USD 3.8 billion. Thermosets are known for their exceptional durability and high-temperature resistance, making them a popular choice in demanding applications. Ceramics are highly valued for their superior dielectric properties, ideal for high-voltage operations, while fiberglass provides strength and excellent insulation capabilities. Mica remains a preferred material in high-voltage environments, providing both heat resistance and electrical protection. Additionally, cellulose and cotton are emerging as eco-friendly materials that offer fire resistance, aligning with the growing trend of sustainable and safe solutions in the electrical sector.

The applications of electrical insulation materials are wide-ranging, serving industries like power transformers, distribution transformers, electrical motors and generators, wires and cables, switchgear, batteries, and circuit breakers. Power transformers accounted for 24.5% of the market share in 2024, with strong growth expected through 2034. Insulation materials are crucial for optimizing the performance and efficiency of distribution transformers and electrical motors, further boosting demand across critical sectors such as power generation, transmission, and industrial automation.

In the U.S., the electrical insulation materials market reached USD 2.8 billion in 2024 and is expected to grow significantly due to substantial investments in infrastructure. Modernizing outdated electrical grids and expanding renewable energy initiatives are driving the adoption of advanced insulation materials. With a focus on sustainability and energy-efficient solutions, the U.S. is poised to remain a major player in the regional market, ensuring continued growth throughout the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand in automotive industry

- 3.6.1.2 Rising adoption in aerospace applications

- 3.6.1.3 Growing chemical processing industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of electrical insulation materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fluorocarbon elastomers (FKM)

- 5.3 Perelectrical insulation materials (FFKM)

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Seals and gaskets

- 6.3 O-rings

- 6.4 Hoses and tubings

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use Industries, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Oil & gas

- 7.5 Chemical processing

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 AGC (Asahi Glass)

- 9.3 Chemours

- 9.4 Daikin Industries

- 9.5 DowDuPont

- 9.6 DuPont (E. I. du Pont de Nemours and Company)

- 9.7 Gujarat Fluorochemicals

- 9.8 HaloPolymer

- 9.9 Mitsui Chemicals

- 9.10 Momentive Performance Materials

- 9.11 Saint-Gobain Performance Plastics

- 9.12 Shin-Etsu Chemical

- 9.13 Solvay

- 9.14 Wacker Chemie

- 9.15 Zeon Corporation

生物基电绝缘材料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、最终用户、形式、安装类型及组件划分

生物基电绝缘材料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、最终用户、形式、安装类型及组件划分 2026年全球电气绝缘材料市场报告

2026年全球电气绝缘材料市场报告 全球柔性绝缘层压板市场预测(按材料类型、产品形式、应用和最终用途行业划分),2026-2032年电气绝缘压製板市场:材料类型、板材类型、厚度、电压等级、製造流程、应用和最终用户划分,全球预测,2026-2032年

全球柔性绝缘层压板市场预测(按材料类型、产品形式、应用和最终用途行业划分),2026-2032年电气绝缘压製板市场:材料类型、板材类型、厚度、电压等级、製造流程、应用和最终用户划分,全球预测,2026-2032年 电气绝缘材料市场规模、份额和成长分析(按材料类型、热固性树脂、应用和地区划分)—2026-2033年产业预测

电气绝缘材料市场规模、份额和成长分析(按材料类型、热固性树脂、应用和地区划分)—2026-2033年产业预测 电气绝缘胶带市场规模、份额及成长分析(按材料、应用及地区划分)-2026-2033年产业预测

电气绝缘胶带市场规模、份额及成长分析(按材料、应用及地区划分)-2026-2033年产业预测 电气绝缘压製板:全球市场份额和排名、总收入和需求预测(2025-2031 年)电气绝缘变压器压製板:全球市场份额和排名、总收入和需求预测(2025-2031年)

电气绝缘压製板:全球市场份额和排名、总收入和需求预测(2025-2031 年)电气绝缘变压器压製板:全球市场份额和排名、总收入和需求预测(2025-2031年) 电气绝缘材料市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年)

电气绝缘材料市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争细分,2020-2030 年) 全球电气绝缘胶带市场

全球电气绝缘胶带市场