|

市场调查报告书

商品编码

1685225

经皮血氧测定係统市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Transcutaneous Oximetry Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

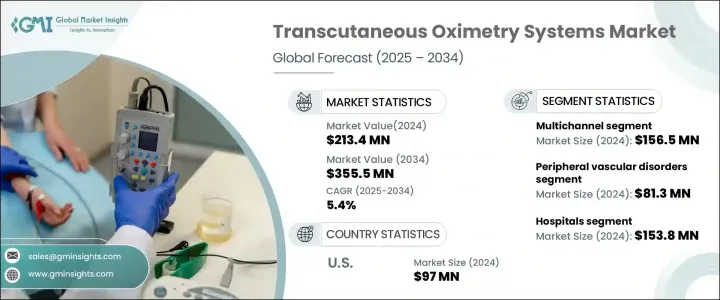

到 2024 年,全球经皮血氧测定係统市场规模将达到 2.134 亿美元,预计 2025 年至 2034 年期间将呈现 5.4% 的稳定成长率。这一市场成长是由多种因素推动的,包括週边动脉疾病盛行率的不断上升、非侵入性监测技术的快速发展以及人口老化。随着对有效伤口护理的需求不断增加,越来越多的医疗保健提供者开始采用经皮血氧测定係统来监测组织中的氧气水平。这些系统可以及时准确地读数,这对于早期检测和预防护理至关重要。

感测器技术和无线连接的创新使这些系统更加高效,并可在广泛的医疗保健环境中轻鬆使用。从医院到门诊设施,经皮血氧测定係统的日益普及反映了精准医疗和以患者为中心的护理的大趋势。随着医疗保健提供者专注于提高诊断准确性和优化工作流程,对这些先进监控解决方案的投资正在增加。此外,监管变化和对血管和呼吸系统疾病的认识不断提高也有助于塑造市场动态。随着患者和照护者寻求即时、在家中监测血氧水平,对家庭医疗保健和远端监控解决方案的需求不断增长,进一步推动了市场的成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.134 亿美元 |

| 预测值 | 3.555 亿美元 |

| 复合年增长率 | 5.4% |

根据通路类型,市场分为多通路系统和单通路系统。 2024 年,多通道系统预计将产生 1.565 亿美元的收入。它们能够同时测量多个部位的氧气水平,从而提高诊断的准确性和效率,特别是对于健康状况复杂的患者。透过消除多次单独读数的需要,这些系统简化了临床工作流程并提供了有关组织氧合的全面资料,从而推动了它们在高容量医疗机构中的普及。

在最终用途方面,医院将在 2024 年占据最大的市场份额,预计到 2034 年收入将达到 1.538 亿美元。医院越来越多地采用经皮血氧仪系统来监测患有周边血管疾病、糖尿病和呼吸系统疾病等慢性疾病的患者。这些系统提供持续、非侵入性的组织氧合评估,以便及时干预,改善患者的治疗效果。这些设备在医院专门部门(如伤口管理、术后监测和血管评估)中的日益整合,进一步刺激了需求。

2024 年,美国经皮血氧测定係统市场价值 9,700 万美元,预计到 2034 年复合年增长率为 4.1%。美国仍然是医疗技术创新领域的全球领导者,推动经皮血氧测定係统在各个医疗保健领域的广泛应用。感测器精度、便携性和无线连接的改进使得这些系统更加用户友好且高效。随着美国医疗保健系统向预防保健转变,这些设备的需求预计将大幅增长,从而促进区域市场扩张。

目录

第 1 章:方法论与范围

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 週边血管疾病和伤口癒合障碍的盛行率不断上升

- 诊断和治疗期间患者监测受到越来越多的关注

- 技术进步

- 人们对早产儿使用经皮血氧测定係统的认识不断提高

- 产业陷阱与挑战

- 严格的监理政策

- 经皮血氧测定係统成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 报销场景

- 定价分析

- 波特的分析

- PESTEL 分析

- 差距分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按通路类型,2021 年至 2034 年

- 主要趋势

- 多通道

- 单通道

第六章:市场估计与预测:按应用,2021 — 2034 年

- 主要趋势

- 周围血管疾病

- 糖尿病足溃疡

- 早产

- 其他应用

第 7 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 诊断中心

- 其他最终用户

第 8 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- ADVIN

- Cephalon

- Drager

- ELCAT

- medicap

- PERIMED

- PHILIPS

- RADIOMETER

- sentec

The Global Transcutaneous Oximetry Systems Market reached USD 213.4 million by 2024 and is expected to exhibit a steady growth rate of 5.4% CAGR from 2025 to 2034. This market growth is driven by a combination of factors, including the increasing prevalence of peripheral artery disease, the rapid advancements in non-invasive monitoring technologies, and the aging population. As the need for effective wound care continues to rise, more healthcare providers are turning to transcutaneous oximetry systems to monitor oxygen levels in tissues. These systems allow for timely and accurate readings, essential for early detection and preventive care.

Innovations in sensor technology and wireless connectivity are making these systems more efficient and accessible across a wide range of healthcare settings. From hospitals to outpatient facilities, the growing adoption of transcutaneous oximetry systems reflects a larger trend toward precision medicine and patient-centered care. With healthcare providers focused on improving diagnostic accuracy and optimizing workflows, investments in these advanced monitoring solutions are increasing. Additionally, regulatory changes and growing awareness about vascular and respiratory conditions are helping to shape market dynamics. The rising demand for home healthcare and remote monitoring solutions further fuels the growth of the market, as patients and caregivers seek real-time, at-home monitoring of oxygenation levels.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $213.4 Million |

| Forecast Value | $355.5 Million |

| CAGR | 5.4% |

By channel type, the market is divided into multichannel and single-channel systems. In 2024, multichannel systems are projected to generate USD 156.5 million in revenue. Their ability to measure oxygen levels at multiple sites simultaneously boosts diagnostic accuracy and enhances efficiency, especially for patients with complex health conditions. By eliminating the need for multiple individual readings, these systems streamline clinical workflows and provide comprehensive data on tissue oxygenation, driving their popularity in high-volume healthcare facilities.

In terms of end use, hospitals lead the market with the largest share in 2024, with revenue expected to reach USD 153.8 million by 2034. Hospitals are increasingly adopting transcutaneous oximetry systems to monitor patients with chronic conditions such as peripheral vascular disease, diabetes, and respiratory disorders. These systems offer continuous, non-invasive assessments of tissue oxygenation, enabling timely interventions that improve patient outcomes. The growing integration of these devices in specialized hospital departments, such as wound management, post-surgical monitoring, and vascular assessments, is further fueling demand.

The U.S. transcutaneous oximetry systems market generated USD 97 million in 2024, with a projected CAGR of 4.1% through 2034. The U.S. remains a global leader in medical technology innovation, driving the widespread adoption of transcutaneous oximetry systems across various healthcare sectors. Improvements in sensor precision, portability, and wireless connectivity are making these systems more user-friendly and efficient. As the U.S. healthcare system shifts towards preventive care, the demand for these devices is expected to grow significantly, contributing to regional market expansion.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of peripheral vascular disorders and wound healing disorders

- 3.2.1.2 Rising focus towards patient monitoring during diagnosis and treatment

- 3.2.1.3 Technological advancements

- 3.2.1.4 Growing awareness regarding use of transcutaneous oximetry systems for preterm infants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory policies

- 3.2.2.2 High cost associated with transcutaneous oximetry systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Pricing analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

- 3.10 Gap analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Channel Type, 2021 — 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multichannel

- 5.3 Single channel

Chapter 6 Market Estimates and Forecast, By Application, 2021 — 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Peripheral vascular disorders

- 6.3 Diabetic foot ulcers

- 6.4 Preterm births

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 — 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Diagnostic centers

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 — 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADVIN

- 9.2 Cephalon

- 9.3 Drager

- 9.4 ELCAT

- 9.5 medicap

- 9.6 PERIMED

- 9.7 PHILIPS

- 9.8 RADIOMETER

- 9.9 sentec