|

市场调查报告书

商品编码

1698241

甲苯二异氰酸酯市场机会、成长动力、产业趋势分析及2025-2034年预测Toluene Diisocyanate Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

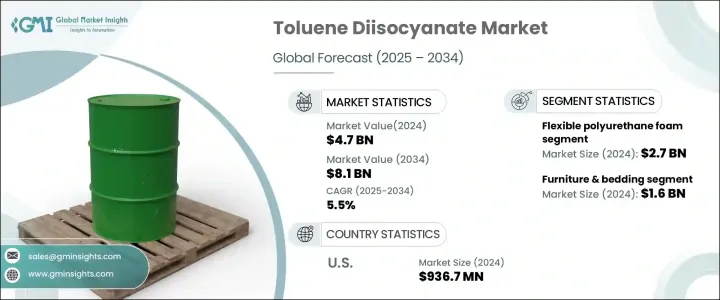

2024 年全球甲苯二异氰酸酯市场价值为 47 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.5%。 TDI 的需求持续上升,主要原因是其在软质聚氨酯泡沫生产中的广泛应用。这些泡沫对于多个行业都至关重要,包括家具、床上用品和汽车应用。随着城市化和住房开发的不断推进,特别是在新兴经济体,对基于 TDI 的产品的需求大幅增长。

随着汽车製造商寻求提高燃油效率和性能的解决方案,汽车製造业向轻质材料的转变进一步刺激了其需求。此外,聚氨酯配方的进步正在提高产品质量,促进市场扩张。永续发展趋势和监管压力正在推动製造商转向低排放、环保的 TDI 替代品,以响应全球减少环境影响的努力。市场的稳定成长反映了其在各种工业应用中的关键作用及其对不断变化的监管和消费者偏好的适应性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 47亿美元 |

| 预测值 | 81亿美元 |

| 复合年增长率 | 5.5% |

软质聚氨酯泡沫市场价值 2024 年为 27 亿美元,预计到 2034 年将以 6.1% 的复合年增长率成长。该材料广泛应用于家具、床上用品和汽车内饰,使其成为市场上升趋势的关键推动因素。消费者对耐用性和舒适性的需求不断增加,促使製造商改进泡沫配方,以获得更好的弹性和支撑性。随着对永续性的重视,生物基泡沫的研究已获得发展动力。家具行业电子商务的成长也在推动用于易于运输和高效包装的聚氨酯泡沫的需求方面发挥了关键作用。

家具和床上用品市场规模在 2024 年将达到 16 亿美元,预计在 2025 年至 2034 年期间的复合年增长率将达到 6.5%。不断增长的城市人口、不断变化的生活方式以及更高的可支配收入将继续推动对高品质聚氨酯家具解决方案的需求。人体工学设计和客製化选项变得越来越普遍,反映了消费者对功能性和个人化家居和办公家具的偏好。人们对环保材料的日益关注导致可回收泡沫产品的采用率更高。由于消费者优先考虑舒适性和生产力,对家庭办公家具的需求进一步加速了市场的扩张。

在美国,2024 年 TDI 市场价值为 9.367 亿美元,预计在预测期内将以 6% 的复合年增长率成长。家具、建筑和汽车行业不断增长的需求对市场成长做出了巨大贡献。在建筑领域,硬质聚氨酯泡棉在隔热方面起着至关重要的作用,而汽车业则利用基于 TDI 的材料来改善车辆内装并减轻重量。随着製造商努力满足监管标准,对永续 TDI 生产的投资预计将重塑市场格局。绿色化学和创新配方的推动使 TDI 成为永续材料开发的关键参与者。

目录

第一章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 蓬勃发展的建筑业

- 汽车产业成长

- 技术进步

- 产业陷阱与挑战

- 监管压力

- 原物料价格波动

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 软质聚氨酯泡沫

- 硬质聚氨酯泡沫

- 涂料

- 黏合剂和密封剂

- 弹性体

- 其他的

第六章:市场估计与预测:按最终用途产业,2021-2034 年

- 主要趋势

- 家具和床上用品

- 建造

- 汽车

- 电子产品

- 包装

- 纺织品

- 其他的

第七章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Basf Se

- Cangzhou Dahua Group

- Covestro Ag

- Dow

- Evonik

- Ibi Chematur

- Kh Chemicals

- Merck Kgaa

- Redox

- Sabic

- Simel Chemical Industry Co., Ltd.

- Tokyo Chemical Industry

- Tosoh

- Wanhua

The Global Toluene Diisocyanate Market, valued at USD 4.7 billion in 2024, is projected to expand at a CAGR of 5.5% between 2025 and 2034. Demand for TDI continues to rise, driven primarily by its extensive use in the production of flexible polyurethane foams. These foams are essential in multiple industries, including furniture, bedding, and automotive applications. With increasing urbanization and housing developments, particularly in emerging economies, the need for TDI-based products has significantly surged.

The shift toward lightweight materials in vehicle manufacturing further fuels its demand, as automakers seek solutions that enhance fuel efficiency and performance. Additionally, advancements in polyurethane formulations are enhancing product quality, contributing to market expansion. Sustainability trends and regulatory pressures are pushing manufacturers toward low-emission, eco-friendly TDI alternatives, aligning with global efforts to reduce environmental impact. The market's steady growth reflects its critical role in diverse industrial applications and its adaptation to evolving regulatory and consumer preferences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $8.1 Billion |

| CAGR | 5.5% |

The flexible polyurethane foam segment, valued at USD 2.7 billion in 2024, is expected to grow at a 6.1% CAGR through 2034. The material's widespread application in furniture, bedding, and automotive interiors makes it a key contributor to the market's upward trajectory. Increasing consumer demand for durability and comfort has prompted manufacturers to refine foam formulations for better resilience and support. With a greater emphasis on sustainability, research into bio-based foams has gained momentum. The growth of e-commerce in the furniture sector has also played a crucial role in driving demand for polyurethane foams designed for easy transport and efficient packaging.

The furniture and bedding segment, valued at USD 1.6 billion in 2024, is anticipated to register a 6.5% CAGR from 2025 to 2034. Expanding urban populations, evolving lifestyles, and higher disposable incomes continue to drive demand for high-quality polyurethane-based furniture solutions. Ergonomic designs and customization options are becoming more prevalent, reflecting consumer preferences for functional and personalized home and office furniture. The increasing focus on eco-friendly materials has led to greater adoption of recyclable foam products. The demand for home office furniture has further accelerated the market's expansion, as consumers prioritize comfort and productivity.

In the United States, the TDI market was valued at USD 936.7 million in 2024 and is expected to grow at a 6% CAGR over the forecast period. Rising demand from furniture, construction, and automotive sectors contributes significantly to market growth. In construction, rigid polyurethane foam plays a crucial role in insulation, while the automotive industry leverages TDI-based materials to enhance vehicle interiors and reduce weight. As manufacturers strive to meet regulatory standards, investments in sustainable TDI production are expected to reshape the market landscape. The push toward green chemistry and innovative formulations is positioning TDI as a key player in sustainable material development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Booming construction industry

- 3.6.1.2 Automotive sector growth

- 3.6.1.3 Technological advancements

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Regulatory pressures

- 3.6.2.2 Volatile raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Flexible polyurethane foam

- 5.3 Rigid polyurethane foam

- 5.4 Coatings

- 5.5 Adhesives and sealants

- 5.6 Elastomers

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Furniture & bedding

- 6.3 Construction

- 6.4 Automotive

- 6.5 Electronics

- 6.6 Packaging

- 6.7 Textiles

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Basf Se

- 8.2 Cangzhou Dahua Group

- 8.3 Covestro Ag

- 8.4 Dow

- 8.5 Evonik

- 8.6 Ibi Chematur

- 8.7 Kh Chemicals

- 8.8 Merck Kgaa

- 8.9 Redox

- 8.10 Sabic

- 8.11 Simel Chemical Industry Co., Ltd.

- 8.12 Tokyo Chemical Industry

- 8.13 Tosoh

- 8.14 Wanhua

全球甲苯二异氰酸酯市场规模、份额、趋势和成长分析报告(2026-2034年)

全球甲苯二异氰酸酯市场规模、份额、趋势和成长分析报告(2026-2034年) 甲苯市场分析及预测(至2035年):类型、产品、应用、技术、终端用户、组件、製程、功能、材料类型及导入形式全球甲苯衍生物市场规模、份额、趋势和成长分析报告(2026-2034年)

甲苯市场分析及预测(至2035年):类型、产品、应用、技术、终端用户、组件、製程、功能、材料类型及导入形式全球甲苯衍生物市场规模、份额、趋势和成长分析报告(2026-2034年) 日本甲苯市场规模、份额、趋势和预测:按技术、应用和地区划分,2026-2034年

日本甲苯市场规模、份额、趋势和预测:按技术、应用和地区划分,2026-2034年 2026年全球甲苯市场报告2026年全球甲苯衍生物市场报告

2026年全球甲苯市场报告2026年全球甲苯衍生物市场报告 氯甲苯市场规模、份额和成长分析(依产品类型、形态、应用、最终用途产业、纯度、销售管道和地区划分)-2026-2033年产业预测

氯甲苯市场规模、份额和成长分析(依产品类型、形态、应用、最终用途产业、纯度、销售管道和地区划分)-2026-2033年产业预测 甲苯市场规模、份额及成长分析(按形态、应用和地区划分)-产业预测,2026-2033年

甲苯市场规模、份额及成长分析(按形态、应用和地区划分)-产业预测,2026-2033年 全球乙烯基甲苯(VT)市场-市场份额和排名、总收入、需求预测(2025-2031)

全球乙烯基甲苯(VT)市场-市场份额和排名、总收入、需求预测(2025-2031) 甲苯二异氰酸酯市场预测(至2032年):全球形态、应用、最终用户和地区分析

甲苯二异氰酸酯市场预测(至2032年):全球形态、应用、最终用户和地区分析