|

市场调查报告书

商品编码

1698246

家庭睡眠筛检设备市场机会、成长动力、产业趋势分析及 2025-2034 年预测Home Sleep Screening Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

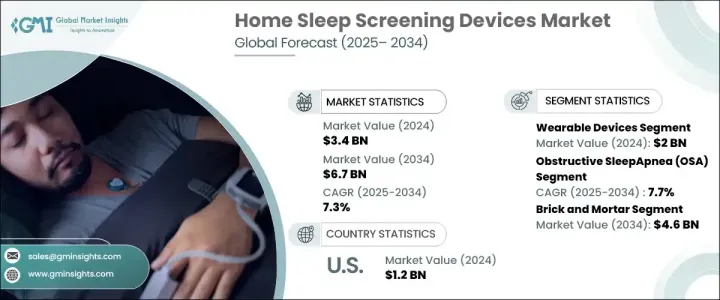

2024 年全球家用睡眠筛检设备市场价值为 34 亿美元,预计 2025 年至 2034 年的复合年增长率为 7.3%。穿戴式和可携式技术的进步、对经济高效的睡眠解决方案日益增长的需求、更高的诊断率以及人口老化是推动扩张的关键因素。失眠、不安腿症候群和阻塞性睡眠呼吸中止症等睡眠障碍的盛行率不断上升,推动了家庭睡眠监测解决方案的需求。

居家睡眠筛检设备监测和分析睡眠模式并检测睡眠障碍。这些工具包括智慧手錶和健身追踪器等穿戴式装置以及便携式多导睡眠图和睡眠呼吸中止监测器等不可穿戴系统。 2024 年,穿戴式装置引领市场,创造 20 亿美元收入,较 2021 年的 17 亿美元成长。这些轻巧的设备使用户可以轻鬆追踪他们的睡眠模式。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 34亿美元 |

| 预测值 | 67亿美元 |

| 复合年增长率 | 7.3% |

2022 年全球穿戴式科技出货量将达到 5.343 亿美元,智慧手錶和健身追踪器的受欢迎程度日益增长。随着消费者对睡眠健康的认识不断提高,穿戴式睡眠监测设备市场大幅扩张。报告显示,成年人的睡眠不足率稳定上升,促使更多人采用穿戴式睡眠追踪解决方案。

根据应用,市场分为阻塞性睡眠呼吸中止症、失眠、不安腿症候群、昼夜节律紊乱和其他情况。阻塞性睡眠呼吸中止症市场在 2024 年的市场规模为 16 亿美元,预计到 2034 年的复合年增长率将达到 7.7%。该疾病被广泛认为是一个主要的健康问题,人们对其风险的认识也不断提高,包括心血管疾病和白天嗜睡。睡眠障碍评估的诊断和转诊的增加增加了对家庭睡眠测试解决方案的需求。

提高人们对睡眠障碍认识的公共卫生措施在市场成长中发挥重要作用。针对识别和管理睡眠呼吸中止症状的教育项目明显增加。此外,居家睡眠筛检设备的采用率也大幅上升,过去几年的使用量显着增加。

根据分销管道,市场分为实体店和电子商务平台。实体零售店(包括药局、医疗用品店和睡眠诊所)在 2024 年占据主导地位,预计到 2034 年将达到 46 亿美元。对于大多数寻求健康相关产品的消费者来说,店内购买仍然是首选。这些地点提供专家指导和实际产品体验,增强客户信心和满意度。

2024 年,美国家用睡眠筛检设备市场规模达到 12 亿美元,预计到 2034 年将以 6.4% 的复合年增长率扩张。家用睡眠测试为传统的实验室为基础的多导睡眠图提供了一种经济高效的替代方案,使消费者更容易获得。成本降低和保险覆盖范围扩大正在推动市场渗透,同时也更广泛地推动预防性医疗保健措施。更高的价格和便利性正在加速向家庭睡眠监测解决方案的转变,为未来几年市场持续成长奠定基础。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球睡眠障碍盛行率不断上升

- 家庭医疗保健解决方案的需求不断增长

- 睡眠监测技术的进步

- 对整合数位健康和可穿戴技术的需求激增

- 产业陷阱与挑战

- 先进设备的初始成本高

- 资料隐私和安全问题

- 成长动力

- 成长潜力分析

- 监管格局

- 我们

- 欧洲

- 技术格局

- 报销场景

- 波特的分析

- PESTEL 分析

- 差距分析

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 穿戴式装置

- 智慧手錶

- 健身追踪器

- 其他穿戴式装置

- 非穿戴式装置

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 阻塞性睡眠呼吸中止症(OSA)

- 失眠

- 不安腿症候群

- 昼夜节律紊乱

- 其他应用

第七章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 实体店面

- 电子商务

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- ApneaMed

- BMC

- BRAEBON

- CleveMed

- GARMIN

- HUAWEI

- natus

- NovaSom

- PHILIPS

- ResMed

- SleepWorks

- SOMNOmedics

- VIRTUOX

- ZEPP

- ZOLL itamar

The Global Home Sleep Screening Devices Market was valued at USD 3.4 billion in 2024 and is expected to grow at a CAGR of 7.3% from 2025 to 2034. Advances in wearable and portable technology, the increasing need for cost-effective sleep solutions, higher diagnosis rates, and an aging population are key factors driving expansion. The rising prevalence of sleep disorders such as insomnia, restless leg syndrome, and obstructive sleep apnea is fueling demand for home-based sleep monitoring solutions.

Home sleep screening devices monitor and analyze sleep patterns and detect disorders. These tools include wearable options like smartwatches and fitness trackers and non-wearable systems like portable polysomnography and sleep apnea monitors. In 2024, wearable devices led the market, generating USD 2 billion, an increase from USD 1.7 billion in 2021. These lightweight devices allow users to track their sleep patterns conveniently.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 7.3% |

Global shipments of wearable technology reached USD 534.3 million in 2022, with a growing preference for smartwatches and fitness trackers. The market for wearable sleep monitoring devices has expanded significantly, driven by increasing consumer awareness of sleep health. Reports indicate that sleep deprivation rates among adults have risen steadily, encouraging more individuals to adopt wearable sleep-tracking solutions.

By application, the market is segmented into obstructive sleep apnea, insomnia, restless leg syndrome, circadian rhythm disorders, and other conditions. The obstructive sleep apnea segment accounted for USD 1.6 billion in 2024 and is projected to grow at a CAGR of 7.7% through 2034. The condition is widely recognized as a major health concern, with rising awareness about its risks, including cardiovascular disease and daytime drowsiness. Increased diagnoses and referrals for sleep disorder evaluations have amplified the demand for home-based sleep testing solutions.

Public health initiatives promoting awareness of sleep disorders are playing a significant role in market growth. There has been a noticeable rise in educational programs focused on recognizing and managing sleep apnea symptoms. Additionally, the adoption of home sleep screening devices has surged, with a significant increase in their use over the past few years.

Based on distribution channels, the market is divided into brick-and-mortar stores and e-commerce platforms. Physical retail outlets, including pharmacies, medical supply stores, and sleep clinics, held the dominant share in 2024 and are projected to reach USD 4.6 billion by 2034. In-store purchases remain the preferred option for most consumers seeking health-related products. These locations offer expert guidance and hands-on product experience, enhancing customer confidence and satisfaction.

In 2024, the U.S. home sleep screening devices market generated USD 1.2 billion and is expected to expand at a CAGR of 6.4% through 2034. Home sleep tests offer a cost-effective alternative to traditional lab-based polysomnography, making them more accessible for consumers. Lower costs and expanding insurance coverage are driving market penetration, alongside a broader push toward preventive healthcare measures. Greater affordability and convenience are accelerating the shift toward at-home sleep monitoring solutions, positioning the market for sustained growth in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global prevalence of sleep disorders

- 3.2.1.2 Growing demand for home healthcare solutions

- 3.2.1.3 Advancements in sleep monitoring technologies

- 3.2.1.4 Surging need for integrated digital health and wearable technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial costs for advanced devices

- 3.2.2.2 Data privacy and security concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Gap analysis

- 3.10 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable devices

- 5.2.1 Smartwatches

- 5.2.2 Fitness trackers

- 5.2.3 Other wearable devices

- 5.3 Non-wearable devices

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Obstructive sleep apnea (OSA)

- 6.3 Insomnia

- 6.4 Restless leg syndrome

- 6.5 Circadian rhythm disorders

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Brick and mortar

- 7.3 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ApneaMed

- 9.2 BMC

- 9.3 BRAEBON

- 9.4 CleveMed

- 9.5 GARMIN

- 9.6 HUAWEI

- 9.7 natus

- 9.8 NovaSom

- 9.9 PHILIPS

- 9.10 ResMed

- 9.11 SleepWorks

- 9.12 SOMNOmedics

- 9.13 VIRTUOX

- 9.14 ZEPP

- 9.15 ZOLL itamar

单分子追踪显微镜市场:按仪器类型、组件、应用和最终用户划分-全球预测,2026-2032年

单分子追踪显微镜市场:按仪器类型、组件、应用和最终用户划分-全球预测,2026-2032年 2026年全球家用睡眠筛检设备市场报告

2026年全球家用睡眠筛检设备市场报告 睡眠技术设备市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户及功能划分2026年全球睡眠技术设备市场报告

睡眠技术设备市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户及功能划分2026年全球睡眠技术设备市场报告 睡眠监测设备市场-2026-2031年预测

睡眠监测设备市场-2026-2031年预测 家用睡眠检测设备市场规模、份额和成长分析(按设备类型、技术、用户画像、功能、通路和地区划分)—2026-2033年产业预测

家用睡眠检测设备市场规模、份额和成长分析(按设备类型、技术、用户画像、功能、通路和地区划分)—2026-2033年产业预测 睡眠科技设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

睡眠科技设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球家用睡眠测试设备市场全球睡眠科技设备市场全球睡眠追踪设备市场

全球家用睡眠测试设备市场全球睡眠科技设备市场全球睡眠追踪设备市场