|

市场调查报告书

商品编码

1698251

远距医疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Telecare Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

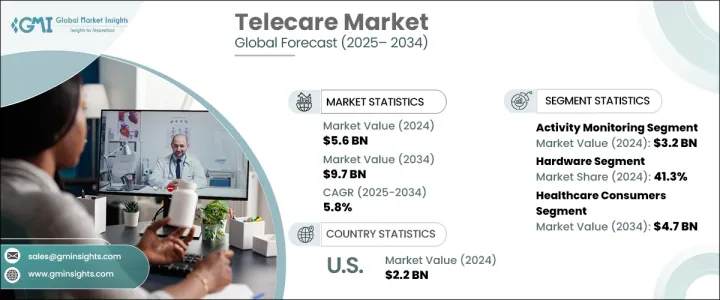

2024 年全球远距医疗市场价值为 56 亿美元,预计在 2025 年至 2034 年期间将以 5.8% 的复合年增长率稳步增长。随着对经济高效且可及的医疗保健解决方案的需求不断增长,远距医疗服务在产业转型中发挥至关重要的作用。糖尿病、高血压和心血管疾病等慢性疾病的日益流行,推动了持续监测和主动管理的需求。随着全球医疗成本的不断上涨,远距医疗透过远端监控减少就诊次数并改善患者治疗效果,提供了可行的替代方案。

技术进步提高了远距医疗解决方案的效率和覆盖范围,进一步推动了市场的成长。穿戴式装置、人工智慧驱动的应用程式和智慧感测器正在彻底改变患者护理,实现即时健康追踪和预测分析。这项创新使医疗保健提供者能够采取预防措施,及时干预,改善患者健康状况并减少紧急住院治疗。随着远距医疗解决方案变得越来越复杂,它们与电子健康记录 (EHR) 和远距医疗平台的整合确保了患者和照护者之间的无缝沟通。世界各国政府和医疗保健组织也透过政策和资金支持远距医疗的采用,加强其在现代医疗保健系统中的作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 56亿美元 |

| 预测值 | 97亿美元 |

| 复合年增长率 | 5.8% |

市场分为两种主要服务类型:活动监控和远端药物管理。 2024 年,活动监测领域将引领市场,达到 32 亿美元。全球老龄人口的增加大大增加了对这些解决方案的需求,因为它们有助于追踪生命体征、活动能力和日常活动,特别是对于独居的老年人。穿戴式健康科技(包括健身追踪器和智慧手錶)越来越多地用于监测心率、氧气水平和睡眠模式等关键健康指标。透过提供即时更新,这些设备使护理人员和医疗专业人员能够及时进行干预。

就组件而言,远距医疗市场包括硬体、软体和服务。受基于感测器的技术和行动健康工具的进步推动,硬体领域在 2024 年占据了 41.3% 的市场份额。血糖监测仪、血压袖带和心率感测器等设备正在提高患者监测能力,实现远端健康追踪并减轻医院的负担。随着医疗保健系统转向预防性护理,这些技术对于确保患者健康和最大限度地降低医疗费用变得不可或缺。

2024 年美国远距医疗市场价值为 22 亿美元,这主要是由于该国慢性病发病率高以及对远距医疗解决方案的需求不断增长。专注于远距医疗的医疗保健新创公司数量激增,加上对远距医疗领域的大量投资,推动了远距医疗服务的快速创新和广泛应用。随着产业的不断发展,人工智慧、物联网健康监测和监管支援的进步将在未来几年进一步加速市场成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 慢性病盛行率不断上升

- 数位健康科技的进步

- 提高认知度与消费者偏好

- 预防保健日益受到重视

- 产业陷阱与挑战

- 资料安全和隐私问题

- 监管挑战和合规问题

- 成长动力

- 成长潜力分析

- 监管格局

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 活动监控

- 远端药物管理

第六章:市场估计与预测:按组件,2021 年至 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医疗保健消费者

- 医疗保健提供者

- 付款人

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Airstrip Technologies

- Allscripts

- Apple

- AT&T

- Biotelemetry

- Google (Alphabet)

- Honeywell Life Care Solutions

- Koninklijke Philips

- Oracle (Cerner Corporation)

- Qualcomm Technologies

- Samsung Electronics

- Teladoc Health

The Global Telecare Market was valued at USD 5.6 billion in 2024 and is set to expand steadily at a CAGR of 5.8% between 2025 and 2034. As the demand for cost-effective and accessible healthcare solutions continues to rise, telecare services are playing a crucial role in transforming the industry. The growing prevalence of chronic diseases, including diabetes, hypertension, and cardiovascular conditions, has driven the need for continuous monitoring and proactive management. With healthcare costs increasing globally, telecare presents a viable alternative by reducing hospital visits and improving patient outcomes through remote monitoring.

The market's growth is further fueled by technological advancements that enhance the efficiency and reach of telecare solutions. Wearable devices, AI-driven applications, and smart sensors are revolutionizing patient care, allowing for real-time health tracking and predictive analytics. This innovation enables healthcare providers to take preventive measures, offering timely interventions that improve patient health and reduce emergency hospitalizations. As telecare solutions become more sophisticated, their integration with electronic health records (EHRs) and telehealth platforms ensures seamless communication between patients and caregivers. Governments and healthcare organizations worldwide are also supporting telecare adoption through policies and funding, reinforcing its role in modern healthcare systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.6 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 5.8% |

The market is segmented into two primary service types: activity monitoring and remote medication management. In 2024, the activity monitoring segment led the market, reaching USD 3.2 billion. The rising global aging population has significantly increased the demand for these solutions, as they help track vital signs, mobility, and daily activities, particularly for seniors living alone. Wearable health technology, including fitness trackers and smartwatches, is increasingly utilized for monitoring key health metrics such as heart rate, oxygen levels, and sleep patterns. By providing real-time updates, these devices empower caregivers and medical professionals to deliver timely interventions.

Regarding components, the telecare market includes hardware, software, and services. The hardware segment held a 41.3% market share in 2024, driven by advancements in sensor-based technology and mobile health tools. Devices like glucose monitors, blood pressure cuffs, and heart rate sensors are improving patient monitoring capabilities, allowing for remote health tracking and reducing the burden on hospitals. As healthcare systems shift towards preventive care, these technologies are becoming indispensable for ensuring patient well-being while minimizing medical expenses.

The U.S. Telecare Market was valued at USD 2.2 billion in 2024, largely due to the country's high incidence of chronic diseases and growing demand for remote healthcare solutions. A surge in healthcare startups specializing in telemedicine, coupled with significant investments in the telehealth sector, has led to rapid innovation and widespread adoption of telecare services. As the industry continues to evolve, advancements in AI, IoT-powered health monitoring, and regulatory support will further accelerate market growth in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic disease

- 3.2.1.2 Advancements in digital health technologies

- 3.2.1.3 Increasing awareness and consumer preference

- 3.2.1.4 Rising shift towards preventive care

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data security and privacy concerns

- 3.2.2.2 Regulatory challenges and compliance issues

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Activity monitoring

- 5.3 Remote medication management

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hardware

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare consumers

- 7.3 Healthcare providers

- 7.4 Payers

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Airstrip Technologies

- 9.2 Allscripts

- 9.3 Apple

- 9.4 AT&T

- 9.5 Biotelemetry

- 9.6 Google (Alphabet)

- 9.7 Honeywell Life Care Solutions

- 9.8 Koninklijke Philips

- 9.9 Oracle (Cerner Corporation)

- 9.10 Qualcomm Technologies

- 9.11 Samsung Electronics

- 9.12 Teladoc Health