|

市场调查报告书

商品编码

1698267

汽车牵引马达市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Traction Motor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

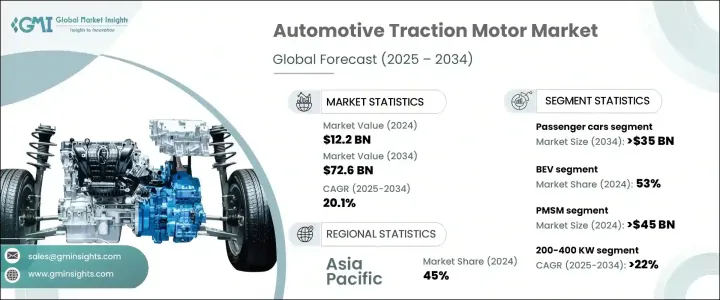

2024 年全球汽车牵引马达市场价值为 122 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 20.1%。全球电动车 (EV) 产量的大幅成长是这一成长的主要驱动力。各国政府正在透过减少对柴油车队的依赖和促进汽车电气化来降低碳排放。消费者也越来越注重永续性和燃料节约,进一步加速了向电动车的转变。

电力电子和马达控制技术的进步正在提高牵引马达的效率和性能。采用碳化硅(SiC)和氮化镓(GaN)半导体可提高电源效率、最大限度地减少能量损失并优化马达输出。这项进步使製造商能够开发出更紧凑、更轻的发动机,从而提高车辆性能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 122亿美元 |

| 预测值 | 726亿美元 |

| 复合年增长率 | 20.1% |

汽车牵引马达市场依马达类型分为永磁同步马达(PMSM)和交流感应马达。 2024 年,PMSM 占据市场主导地位,创造超过 450 亿美元的收入。这些马达因其轻质结构、卓越扭力和更高效率而受到青睐,成为电动车牵引系统的热门选择。由于 PMSM 比感应马达消耗更多的电能,因此製造商优先将其整合到现代电动车设计中。

稀土材料成本的上升和供应问题的出现,促使製造商开发不含稀土元素的永磁同步电机,这种电机无需钕或镝就能高效运行。这些创新正在稳定供应链并促进永磁同步马达在电动车中的更广泛应用。随着这些设计的不断改进,预计将有更多製造商采用它们,从而进一步推动市场扩张。

根据功率输出,市场也分为三类:低于 200 kW、200-400 kW 和高于 400 kW。预计到 2034 年,200-400 kW 细分市场的复合年增长率将超过 22%。该范围内的高输出牵引马达在电动 SUV、跑车和商用车中越来越受欢迎。汽车製造商正在整合这些马达以提高加速度和性能,满足对强大而高效的电动传动系统日益增长的需求。

卡车和公共汽车等电动商用车也推动了对高功率牵引马达的需求。物流和货运正在向电气化转型,对高扭力和高功率容量马达的需求不断增加。现在许多电动车都配备了双马达全轮驱动 (AWD) 系统,以提高稳定性和牵引力,同时要求额定功率在 200-400 kW 范围内。汽车製造商正在采用这种设计来优化车辆动力学,进一步推动对高功率牵引马达的需求。

亚太地区仍然是电动车生产的主导力量,中国、日本、韩国和印度等国家大力投资电动车基础设施和製造业。领先的电动车製造商的存在以及区域供应链的进步,特别是稀土磁铁生产方面的进步,正在支持市场成长。中国作为全球最大的电动车市场,不断扩大产能以满足国内和全球需求。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 原料及零件供应商

- 製造商

- 汽车製造商

- 最终用途

- 供应商格局

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 价格趋势

- 案例研究

- 衝击力

- 成长动力

- 政府加强激励措施和减排政策力度,推动电动车发展

- 消费者对环保节能电动车的需求不断成长

- 提高马达效率,降低能耗,延长车辆行驶里程

- 人工智慧和自动驾驶技术的日益普及,推动了牵引马达系统的创新

- 产业陷阱与挑战

- 引擎所需的稀土元素等关键材料的供应链限制

- 先进牵引马达技术开发成本高昂

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车 (LCV)

- 重型商用车(HCV)

- 两轮车

- 越野车

第六章:市场估计与预测:按电动传动系统,2021 - 2034 年

- 主要趋势

- 纯电动车(BEV)

- 混合动力电动车 (HEV)

- 插电式混合动力电动车(PHEV)

第七章:市场估计与预测:按汽车,2021 - 2034 年

- 主要趋势

- 永磁同步电机

- 交流感应

第八章:市场估计与预测:依发电量,2021 - 2034

- 主要趋势

- 小于200千瓦

- 200-400千瓦

- 400度以上

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Audi

- Bosch

- Continental

- Ford

- General

- Honda

- Hyundai

- Kia

- Magna

- Magneti Marelli

- Mercedes Benz

- Mitsubishi

- Nidec

- Parker Hannifin

- PSA Group

- SAIC Motor

- Schaeffler

- Valeo

- Volkswagen

- ZF Friedrichshafen

The Global Automotive Traction Motor Market was valued at USD 12.2 billion in 2024 and is projected to grow at a CAGR of 20.1% from 2025 to 2034. A significant rise in electric vehicle (EV) production worldwide is a key driver of this growth. Governments are pushing for lower carbon emissions by reducing reliance on diesel fleets and promoting vehicle electrification. Consumers are also becoming more conscious of sustainability and fuel conservation, further accelerating the transition to EVs.

Technological advancements in power electronics and motor control are improving the efficiency and performance of traction motors. The adoption of silicon carbide (SiC) and gallium nitride (GaN) semiconductors enhances power efficiency, minimizes energy loss, and optimizes motor output. This progress allows manufacturers to develop more compact and lightweight motors, leading to better vehicle performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.2 Billion |

| Forecast Value | $72.6 Billion |

| CAGR | 20.1% |

The automotive traction motor market is categorized by motor type into Permanent Magnet Synchronous Motors (PMSM) and AC induction motors. PMSM dominated the market in 2024, generating over USD 45 billion in revenue. These motors are preferred due to their lightweight structure, superior torque, and higher efficiency, making them a popular choice for EV traction systems. As PMSMs consume more electric energy compared to induction motors, manufacturers are prioritizing their integration into modern EV designs.

Rising costs and supply concerns surrounding rare earth materials have prompted manufacturers to develop rare-earth-free PMSMs that function efficiently without neodymium or dysprosium. These innovations are stabilizing the supply chain and facilitating broader adoption of PMSMs in EVs. As these designs continue to improve, more manufacturers are expected to implement them, further driving market expansion.

The market is also segmented by power output into three categories: less than 200 kW, 200-400 kW, and above 400 kW. The 200-400 kW segment is anticipated to grow at a CAGR of over 22% by 2034. High-output traction motors in this range are becoming increasingly popular in electric SUVs, sports cars, and commercial vehicles. Automakers are integrating these motors to enhance acceleration and performance, meeting the growing demand for powerful yet efficient electric drivetrains.

Electric commercial vehicles, including trucks and buses, are also fueling the demand for high-power traction motors. Logistics and freight transport are transitioning toward electrification, increasing the need for motors with high torque and power capacity. Many EVs are now equipped with dual-motor all-wheel-drive (AWD) systems, improving stability and traction while requiring power ratings within the 200-400 kW range. Automakers are adopting this design to optimize vehicle dynamics, further driving the demand for high-power traction motors.

Asia Pacific remains a dominant force in EV production, with countries such as China, Japan, South Korea, and India investing heavily in EV infrastructure and manufacturing. The presence of leading EV manufacturers and advancements in the regional supply chain, particularly in rare earth magnet production, are supporting market growth. China, as the world's largest EV market, continues to expand production capacity to cater to both domestic and global demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material & component suppliers

- 3.1.2 Manufacturers

- 3.1.3 Automotive manufacturers

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trend

- 3.9 Case studies

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing government incentives and emission reduction policies promoting electric vehicles

- 3.10.1.2 Rising consumer demand for eco-friendly and energy-efficient electric vehicles

- 3.10.1.3 Advancements in motor efficiency, reducing energy consumption and extending vehicle range

- 3.10.1.4 Growing adoption of AI and autonomous technologies, driving innovation in traction motor systems

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Supply chain constraints for critical materials such as rare earth elements needed for motors

- 3.10.2.2 High development costs associated with advanced traction motor technologies

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light Commercial Vehicles (LCV)

- 5.3.2 Heavy Commercial Vehicles (HCV)

- 5.4 Two-wheelers

- 5.5 Off-road vehicles

Chapter 6 Market Estimates & Forecast, By Electric Drivetrain, 2021 - 2034($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicle (BEV)

- 6.3 Hybrid Electric Vehicle (HEV)

- 6.4 Plug-in Hybrid Electric Vehicle (PHEV)

Chapter 7 Market Estimates & Forecast, By Motor, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 PMSM

- 7.3 AC Induction

Chapter 8 Market Estimates & Forecast, By Power Output, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Less than 200 KW

- 8.3 200-400 KW

- 8.4 Above 400 KW

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Audi

- 10.2 Bosch

- 10.3 Continental

- 10.4 Ford

- 10.5 General

- 10.6 Honda

- 10.7 Hyundai

- 10.8 Kia

- 10.9 Magna

- 10.10 Magneti Marelli

- 10.11 Mercedes Benz

- 10.12 Mitsubishi

- 10.13 Nidec

- 10.14 Parker Hannifin

- 10.15 PSA Group

- 10.16 SAIC Motor

- 10.17 Schaeffler

- 10.18 Valeo

- 10.19 Volkswagen

- 10.20 ZF Friedrichshafen

NEV eAxle - 全球市场份额和排名、总销售量和需求预测(2025-2031 年)

NEV eAxle - 全球市场份额和排名、总销售量和需求预测(2025-2031 年) 汽车牵引马达市场(按马达类型、额定功率、车辆类型、速度范围、冷却方式和车辆应用划分)-全球预测,2025-2032年电动车牵引逆变器系统市场(依车辆类型、半导体材料、逆变器拓朴结构、额定功率及销售管道)-全球预测,2025-2032年

汽车牵引马达市场(按马达类型、额定功率、车辆类型、速度范围、冷却方式和车辆应用划分)-全球预测,2025-2032年电动车牵引逆变器系统市场(依车辆类型、半导体材料、逆变器拓朴结构、额定功率及销售管道)-全球预测,2025-2032年 2025年全球电动车牵引马达市场报告

2025年全球电动车牵引马达市场报告 全球汽车牵引马达市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测全球车辆牵引及辅助电池市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球汽车牵引马达市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测全球车辆牵引及辅助电池市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 全球汽车牵引马达市场

全球汽车牵引马达市场 汽车牵引马达市场-全球产业规模、份额、趋势、机会和预测,按车辆类型、电动车类型、功率输出、马达类型、地区和竞争细分,2020-2030 年2026-2032 年电动车牵引马达市场(按车型、马达类型和地区划分)

汽车牵引马达市场-全球产业规模、份额、趋势、机会和预测,按车辆类型、电动车类型、功率输出、马达类型、地区和竞争细分,2020-2030 年2026-2032 年电动车牵引马达市场(按车型、马达类型和地区划分) 2032年电动车牵引动力市场预测:按马达类型、额定功率、车辆类型和地区分類的全球分析

2032年电动车牵引动力市场预测:按马达类型、额定功率、车辆类型和地区分類的全球分析