|

市场调查报告书

商品编码

1698271

上皮瘤治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Epithelioma Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

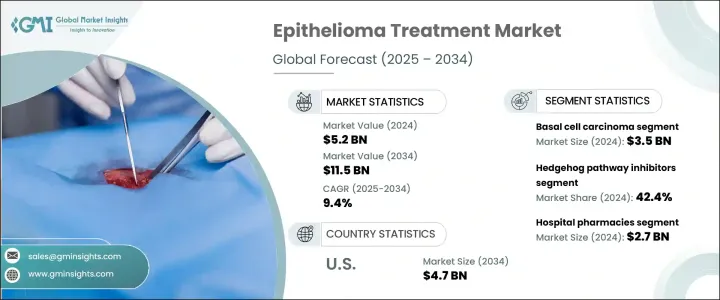

2024 年全球上皮瘤治疗市场价值约为 52 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 9.4%。由于上皮组织肿瘤病例的增加,市场正在扩大,这些肿瘤可能是良性的,也可能是恶性的,例如基底细胞癌和鳞状细胞癌。治疗的重点是切除肿瘤、预防復发和减轻有害影响。提高意识、早期发现和政府措施是推动市场成长的关键因素。皮肤癌病例的不断增加刺激了对创新疗法的需求,从而导致治疗方法取得了重大进展。持续的研发努力和新药核准正在进一步推动市场扩张。监管机构正在支持引入先进的治疗方案,改善患者获得有效治疗选择的机会。医疗技术的进步也透过更好的疾病管理促进了市场的成长。

市场按类型、药品类别和配销通路细分。根据类型,基底细胞癌占最大份额,2024 年创造 35 亿美元的收入。作为最常见的非黑色素瘤皮肤癌形式,其发生率的上升增加了对有效治疗的需求。长期暴露于紫外线和生活方式的改变等因素导致病例激增。人们对早期检测的认识不断提高,进一步推动了对先进疗法的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 52亿美元 |

| 预测值 | 115亿美元 |

| 复合年增长率 | 9.4% |

按药物类别划分,Hedgehog 通路抑制剂占据主导地位,到 2024 年将贡献 42.4% 的总市场收入。此细分市场的成长是由基底细胞癌盛行率的上升所推动的,尤其是在日照强度高和人口老化的地区。这些抑制剂已被证明在治疗晚期和转移性病例方面有效,因此其采用率高于传统的化疗和放射疗法。正在进行的研究和临床试验可能会引入更多的刺猬通路抑制剂,扩大患者的治疗选择。

在分销管道方面,医院药房成为领先细分市场,2024 年销售额达 27 亿美元。这些药房在为接受上皮瘤治疗的住院患者提供即时药物方面发挥着至关重要的作用。因基底细胞癌和鳞状细胞癌入院的人数不断增加,促进了该领域的扩张。医院药局也提供支持性护理服务,确保全面治疗并改善病患治疗效果。

从地区来看,北美是上皮瘤治疗市场的关键参与者。尤其是美国,预计将大幅成长,市场收入将从 2023 年的 20 亿美元增加到 2034 年的 47 亿美元。该国受益于有利的监管环境,有利于促进先进疗法的采用。预计新疗法的监管批准将推动市场发展,增强该地区未来几年的主导地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 皮肤癌发生率上升

- 标靶治疗和免疫疗法的进展

- 支持性医疗基础设施和宣传活动

- 产业陷阱与挑战

- 治疗费用高

- 疾病晚期疗效有限且有不良反应

- 成长动力

- 成长潜力分析

- 监管格局

- 差距分析

- 专利分析

- 管道分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 基底细胞癌

- 鳞状细胞癌

- 其他类型

第六章:市场估计与预测:依药物类别,2021 年至 2034 年

- 主要趋势

- Hedgehog 路径抑制剂

- 免疫检查点抑制剂

- 化疗药物

- 其他药物类别

第七章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 电子商务

- 其他分销管道

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Amgen

- AstraZeneca

- BeiGene

- Bristol-Myers Squibb

- F. Hoffmann-La Roche

- Johnson & Johnson

- Merck and Co.

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Sun Pharmaceutical Industries

The Global Epithelioma Treatment Market was valued at approximately USD 5.2 billion in 2024 and is projected to grow at a 9.4% CAGR from 2025 to 2034. The market is expanding due to rising cases of epithelial tissue tumors, which may be benign or malignant, such as basal cell carcinoma and squamous cell carcinoma. Treatment focuses on removing tumors, preventing recurrence, and mitigating harmful effects. Increasing awareness, early detection, and government initiatives are key factors driving market growth. The growing number of skin cancer cases has fueled demand for innovative therapies, leading to significant advancements in treatment methods. Continuous R&D efforts and new drug approvals are further propelling market expansion. Regulatory bodies are supporting the introduction of advanced therapeutic solutions, improving patient access to effective treatment options. Medical technology improvements have also strengthened market growth by enabling better disease management.

The market is segmented by type, drug class, and distribution channel. Based on type, basal cell carcinoma accounted for the largest share, generating USD 3.5 billion in revenue in 2024. As the most prevalent form of non-melanoma skin cancer, its rising incidence has increased the demand for effective treatments. Factors such as prolonged UV exposure and shifting lifestyle patterns have contributed to the surge in cases. Greater awareness of early detection has further boosted the need for advanced therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 9.4% |

By drug class, hedgehog pathway inhibitors held the dominant share, contributing 42.4% of total market revenue in 2024. The segment growth is driven by the increasing prevalence of basal cell carcinoma, especially in regions with high sunlight exposure and aging populations. These inhibitors have demonstrated efficacy in treating advanced and metastatic cases, leading to their higher adoption over traditional chemotherapy and radiation therapies. Ongoing research and clinical trials are likely to introduce additional hedgehog pathway inhibitors, expanding treatment options for patients.

Regarding distribution channels, hospital pharmacies emerged as the leading segment, generating USD 2.7 billion in 2024. These pharmacies play a crucial role in providing immediate access to medications for inpatients undergoing treatment for epithelioma. The rising number of hospital admissions for basal cell carcinoma and squamous cell carcinoma has contributed to segment expansion. Hospital pharmacies also facilitate supportive care services, ensuring comprehensive treatment and improving patient outcomes.

Regionally, North America is a key player in the epithelioma treatment market. The United States, in particular, is projected to witness substantial growth, with market revenue increasing from USD 2 billion in 2023 to USD 4.7 billion by 2034. The country benefits from a favorable regulatory landscape that promotes the adoption of advanced therapies. Regulatory approvals for novel treatments are expected to drive market progression, strengthening the region's dominance in the coming years.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 Synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of skin cancer

- 3.2.1.2 Advancements in targeted therapies and immunotherapies

- 3.2.1.3 Supportive healthcare infrastructure and awareness campaigns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Limited efficacy and adverse effects in advanced stages of the disease

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Basal cell carcinoma

- 5.3 Squamous cell carcinoma

- 5.4 Other types

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hedgehog pathway inhibitors

- 6.3 Immune checkpoint inhibitors

- 6.4 Chemotherapeutic agents

- 6.5 Other drug classes

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

- 7.5 Other distribution channels

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amgen

- 9.2 AstraZeneca

- 9.3 BeiGene

- 9.4 Bristol-Myers Squibb

- 9.5 F. Hoffmann-La Roche

- 9.6 Johnson & Johnson

- 9.7 Merck and Co.

- 9.8 Novartis

- 9.9 Pfizer

- 9.10 Regeneron Pharmaceuticals

- 9.11 Sanofi

- 9.12 Sun Pharmaceutical Industries