|

市场调查报告书

商品编码

1698276

资料中心支援基础设施市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Data Center Support Infrastructure Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球资料中心支援基础设施市场规模达到 392 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 9.1%。数位转型、云端运算和人工智慧 (AI) 等先进技术的日益普及,持续推动对高效、可扩展资料中心基础设施的需求。随着企业越来越依赖数据驱动的运营,各行各业的组织都优先考虑扩展和现代化其资料中心,以提高效率、安全性和永续性。

随着巨量资料分析、机器学习和物联网 (IoT) 的快速发展,对可靠的资料储存、处理和管理解决方案的需求达到了前所未有的高度。企业正在对配电、冷却解决方案和安全系统进行大量投资,以保持营运连续性并防止停机。随着企业将内部部署基础设施与基于云端的服务相结合以优化效能和成本效率,混合云端模型的采用日益增多,进一步推动了市场扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 392亿美元 |

| 预测值 | 922亿美元 |

| 复合年增长率 | 9.1% |

该市场涵盖多个基础设施领域,包括配电系统、冷却系统、机架和机柜、安全系统以及站点和设施基础设施。其中,配电系统到2024年将占30%的份额,成为最重要的部分。这些系统包括发电机、不间断电源 (UPS) 和配电单元 (PDU),在维持资料中心的持续电力供应方面发挥着至关重要的作用。 PDU 对于分配电力给各种 IT 设备至关重要,而 UPS 系统则确保关键系统在停电期间仍能运作。发电机充当备用电源,提供额外的可靠性,防止资料中心运作中断。随着资料流量的不断增加以及对云端服务的依赖日益加深,企业越来越重视节能且具弹性的电力基础设施,以支援其不断增长的资料处理需求。

市场根据组织规模进一步细分,包括中小型企业 (SME) 和大型企业。 2024年,大型企业将占据市场主导地位,占有67%的份额。这些公司正在扩展其 IT 基础设施,以管理大量资料工作负载并增强处理能力。随着企业致力于优化营运效率并最大限度地降低能源消耗,对先进配电、高速网路和下一代冷却解决方案的投资正在加速。随着人工智慧、自动化和即时资料分析的日益普及,企业正在整合智慧基础设施管理解决方案,以简化营运并降低成本。混合云端解决方案也在重塑市场格局,大型企业利用内部资料中心和基于云端的平台的组合来实现更大的灵活性、可扩展性和资料安全性。

北美资料中心支援基础设施市场占有 35% 的份额,其中美国是最大的贡献者。 2024 年,受云端运算、人工智慧应用和数位服务的强劲需求推动,美国从资料中心支援基础设施中获得了 120 亿美元的收入。作为技术最先进的地区之一,美国继续引领全球资料中心产业,超大规模资料中心和主机託管设施正在显着扩张。包括 IT、电信、金融和医疗保健在内的各行各业的企业都在大力投资最先进的基础设施,以支援其数位转型计画。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 人工智慧软体供应商

- 服务提供者

- 数据提供者

- 系统整合商

- 最终用途

- 供应商格局

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 案例研究

- 衝击力

- 成长动力

- 云端服务需求增加

- 超大规模和边缘资料中心的兴起

- 资料中心设计的技术进步

- 政府措施和政策

- 产业陷阱与挑战

- 能源消耗和环境影响不断增加

- 资料安全与保障问题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依基础设施,2021 - 2034 年

- 主要趋势

- 配电系统

- 冷却系统

- 机架和机柜

- 场地和设施基础设施

- 安全系统

第六章:市场估计与预测:依部署模型,2021 - 2034 年

- 主要趋势

- 本地

- 云

第七章:市场估计与预测:依组织规模,2021 - 2034 年

- 主要趋势

- 中小企业

- 大型企业

第八章:市场估计与预测:依层级,2021 - 2034 年

- 主要趋势

- 一级

- II 级

- 第三级

- IV 级

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- IT和电信

- 金融服务业

- 医疗保健与生命科学

- 政府和国防

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- ABB

- Asetek

- Black Box

- Cisco Systems

- Delta Electronics

- Eaton

- Fujitsu

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies

- IBM

- Johnson Controls

- Legrand

- Mitsubishi Electric

- Raritan

- Rittal

- Schneider Electric

- Siemens

- STULZ

- Toshiba

- Vertiv

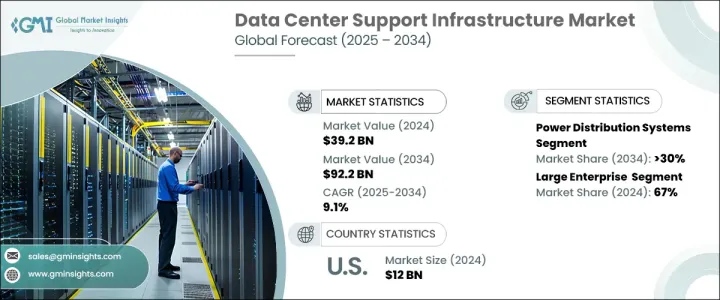

The Global Data Center Support Infrastructure Market reached USD 39.2 billion in 2024 and is projected to grow at a CAGR of 9.1% between 2025 and 2034. The increasing adoption of digital transformation, cloud computing, and advanced technologies such as artificial intelligence (AI) continues to drive demand for efficient and scalable data center infrastructure. As businesses increasingly rely on data-driven operations, organizations across various industries are prioritizing the expansion and modernization of their data centers to enhance efficiency, security, and sustainability.

With rapid advancements in big data analytics, machine learning, and the Internet of Things (IoT), the need for reliable data storage, processing, and management solutions is at an all-time high. Enterprises are making substantial investments in power distribution, cooling solutions, and security systems to maintain operational continuity and prevent downtime. The rising adoption of hybrid cloud models is further fueling market expansion as businesses integrate on-premises infrastructure with cloud-based services to optimize performance and cost efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39.2 Billion |

| Forecast Value | $92.2 Billion |

| CAGR | 9.1% |

The market encompasses several infrastructure segments, including power distribution systems, cooling systems, racks and enclosures, security systems, and site and facility infrastructure. Among these, power distribution systems accounted for a 30% share in 2024, making them the most significant segment. These systems, comprising generators, uninterruptible power supplies (UPS), and power distribution units (PDUs), play a crucial role in maintaining continuous power supply within data centers. PDUs are essential for distributing electricity to various IT equipment, while UPS systems ensure that critical systems remain operational during outages. Generators act as backup power sources, offering an additional layer of reliability to prevent disruptions in data center operations. With the increasing volume of data traffic and the growing reliance on cloud services, organizations are placing greater emphasis on energy-efficient and resilient power infrastructure to support their expanding data processing needs.

The market is further segmented based on organization size, including small and medium enterprises (SME) and large enterprises. In 2024, large enterprises dominated the market with a 67% share. These companies are expanding their IT infrastructures to manage extensive data workloads and enhance processing capabilities. Investments in advanced power distribution, high-speed networking, and next-generation cooling solutions are accelerating as enterprises aim to optimize operational efficiency and minimize energy consumption. With AI, automation, and real-time data analytics gaining traction, businesses are integrating intelligent infrastructure management solutions to streamline operations and reduce costs. Hybrid cloud solutions are also reshaping the market landscape, with large enterprises leveraging a combination of on-premises data centers and cloud-based platforms to achieve greater flexibility, scalability, and data security.

North America data center support infrastructure market held a 35% share, with the U.S. being the largest contributor. In 2024, the U.S. generated USD 12 billion in revenue from data center support infrastructure, driven by strong demand for cloud computing, AI-powered applications, and digital services. As one of the most technologically advanced regions, the U.S. continues to lead the global data center industry, with hyperscale data centers and colocation facilities witnessing significant expansion. Enterprises across industries, including IT, telecom, finance, and healthcare, are heavily investing in state-of-the-art infrastructure to support their digital transformation initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 AI software providers

- 3.1.2 Service providers

- 3.1.3 Data providers

- 3.1.4 System integrators

- 3.1.5 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Case studies

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increased demand for cloud services

- 3.9.1.2 Rise of hyperscale and edge data centers

- 3.9.1.3 Technological advancements in data center design

- 3.9.1.4 Government initiatives and policies

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing energy consumption and environmental impact

- 3.9.2.2 Data safety and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Infrastructure, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Power distribution systems

- 5.3 Cooling systems

- 5.4 Racks and enclosures

- 5.5 Site and facility infrastructure

- 5.6 Security systems

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprise

Chapter 8 Market Estimates & Forecast, By Tier, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Tier I

- 8.3 Tier II

- 8.4 Tier III

- 8.5 Tier IV

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 IT & telecom

- 9.3 BFSI

- 9.4 Healthcare & life sciences

- 9.5 Government & defense

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Asetek

- 11.3 Black Box

- 11.4 Cisco Systems

- 11.5 Delta Electronics

- 11.6 Eaton

- 11.7 Fujitsu

- 11.8 Hewlett Packard Enterprise (HPE)

- 11.9 Huawei Technologies

- 11.10 IBM

- 11.11 Johnson Controls

- 11.12 Legrand

- 11.13 Mitsubishi Electric

- 11.14 Raritan

- 11.15 Rittal

- 11.16 Schneider Electric

- 11.17 Siemens

- 11.18 STULZ

- 11.19 Toshiba

- 11.20 Vertiv