|

市场调查报告书

商品编码

1698286

子宫内膜异位症治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Endometriosis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

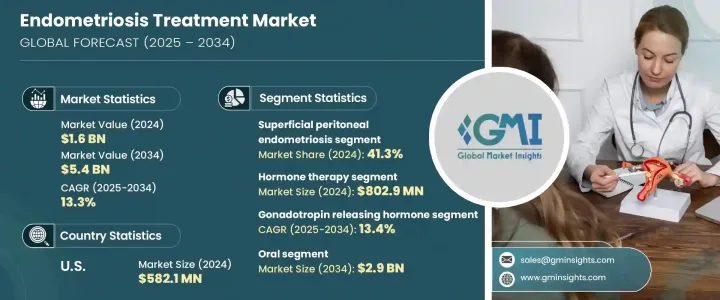

全球子宫内膜异位症治疗市场价值 16 亿美元,预计 2025 年至 2034 年期间的复合年增长率将达到 13.3%,这得益于人们认识的提高、医疗治疗的进步以及医疗保健可及性的提高。加强教育和早期诊断工作正在帮助更多人在早期阶段寻求医疗干预,从而增加对有效治疗方案的需求。医疗保健提供者正专注于综合管理策略,不仅解决即时症状缓解问题,而且还改善长期健康结果。政府措施和倡导团体在消除对这种疾病的耻辱感、鼓励更多女性寻求治疗方面发挥关键作用。研发投入的不断增加也有助于扩大治疗选择,製药公司正在探索创新疗法以加强对患者的照护。

医疗支出的增加和保险覆盖范围的扩大使得子宫内膜异位症的治疗变得更加容易,更多的患者能够及时得到医疗救治。随着宣传活动不断强调未治疗的子宫内膜异位症的长期影响,越来越多的患者正在寻求专门的护理。对非侵入性治疗方案的需求激增,尤其是寻求手术介入替代方案的年轻患者。医疗保健专业人员正在努力整合个人化治疗方法,以满足个别患者的需求,进一步推动市场向前发展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 16亿美元 |

| 预测值 | 54亿美元 |

| 复合年增长率 | 13.3% |

根据疾病类型,市场细分为不同的形式,其中浅层腹膜子宫内膜异位症部分在 2024 年占据 41.3% 的主导份额。这种形式的疾病以腹膜表面病变为特征,比深层子宫内膜异位症更广泛且更容易辨识。因此,这种疾病的诊断频率更高,从而需要更快的医疗干预,并且针对这种类型的治疗的需求更高。早期检测和管理浅层腹膜子宫内膜异位症的能力使其成为市场上最普遍的领域。

子宫内膜异位症的治疗方案主要分为荷尔蒙疗法和疼痛管理,其中荷尔蒙疗法在 2024 年产生 8.029 亿美元的收入。医生通常会开立避孕药、黄体素和荷尔蒙调节药物来缓解骨盆腔疼痛和月经过多等症状。这些治疗方法因其有效性、易于实施以及能够改善患者的生活品质而越来越受欢迎。越来越多的人选择荷尔蒙疗法,因为它们可以缓解症状,而无需进行侵入性手术。

受公共卫生计画和宣传活动不断加强的推动,美国子宫内膜异位症治疗市场规模在 2024 年达到 5.821 亿美元。努力教育人们了解子宫内膜异位症的症状和影响,鼓励人们做出积极的医疗保健决策,并减少围绕疾病的耻辱感。医学研究的进步、对生殖健康的更加关注以及专业医疗服务的改善正在进一步加速市场扩张。随着对创新治疗方案的需求不断增长,製药公司和医疗保健提供者正在努力透过更先进、更有针对性的治疗方法来改善患者的治疗效果。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 子宫内膜异位症的盛行率和认知度不断上升

- 诊断技术的进步

- 增加政府资金和倡议

- 产业陷阱与挑战

- 先进治疗成本高

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依疾病类型,2021 年至 2034 年

- 主要趋势

- 表浅腹膜子宫内膜异位症

- 卵巢子宫内膜异位症

- 深部浸润性子宫内膜异位症

- 其他疾病类型

第六章:市场估计与预测:依治疗类型,2021 年至 2034 年

- 主要趋势

- 荷尔蒙治疗

- 止痛药

第七章:市场估计与预测:依药物类别,2021 年至 2034 年

- 主要趋势

- 促性腺激素释放激素

- 非类固醇抗发炎药

- 口服避孕药

- 其他药物类

第八章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 注射剂

- 其他给药途径

第九章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- AbbVie

- Astellas Pharma

- AstraZeneca

- Bayer

- Eli Lilly and Company

- ObsEva

- Pfizer

- Teva Pharmaceutical Industries

- TerSera Therapeutics

- Zydus Healthcare Limited

The Global Endometriosis Treatment Market, valued at USD 1.6 billion in 2024, is projected to expand at a CAGR of 13.3% from 2025 to 2034, driven by rising awareness, advances in medical treatments, and improved healthcare accessibility. Increased education and early diagnosis efforts are helping more individuals seek medical intervention at earlier stages, boosting demand for effective therapeutic solutions. Healthcare providers are focusing on comprehensive management strategies that not only address immediate symptom relief but also improve long-term health outcomes. Government initiatives and advocacy groups are playing a critical role in destigmatizing the condition, encouraging more women to pursue treatment options. The growing investment in research and development is also contributing to the expansion of treatment choices, with pharmaceutical companies exploring innovative therapies to enhance patient care.

Rising healthcare expenditure and improved insurance coverage have made endometriosis treatments more accessible, allowing more patients to receive timely medical attention. As awareness campaigns continue to highlight the long-term impact of untreated endometriosis, an increasing number of patients are seeking specialized care. The demand for non-invasive treatment options has surged, particularly among younger patients looking for alternatives to surgical interventions. Healthcare professionals are working to integrate personalized treatment approaches that cater to individual patient needs, further driving the market forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 13.3% |

By disease type, the market is segmented into different forms, with the superficial peritoneal endometriosis segment holding a dominant 41.3% share in 2024. This form of the condition, characterized by lesions on the peritoneal surface, is widespread and more easily identifiable than deeper forms of endometriosis. As a result, it is diagnosed more frequently, leading to quicker medical intervention and higher demand for treatments targeting this type. The ability to detect and manage superficial peritoneal endometriosis early has positioned it as the most prevalent segment within the market.

Endometriosis treatment options are primarily divided into hormone therapy and pain management, with hormone therapy generating USD 802.9 million in 2024. Physicians commonly prescribe contraceptives, progestins, and hormone-modulating drugs to alleviate symptoms such as pelvic pain and excessive menstrual bleeding. These treatments are gaining popularity due to their effectiveness, ease of administration, and ability to improve patients' quality of life. More individuals are opting for hormone-based therapies as they provide symptom relief without the need for invasive procedures.

The United States endometriosis treatment market accounted for USD 582.1 million in 2024, fueled by increasing public health initiatives and awareness campaigns. Efforts to educate individuals about the symptoms and implications of endometriosis have encouraged proactive healthcare decisions and reduced stigma surrounding the condition. Advancements in medical research, a stronger focus on reproductive health, and improved access to specialized healthcare services are further accelerating market expansion. As demand for innovative treatment solutions continues to grow, pharmaceutical companies and healthcare providers are working to enhance patient outcomes through more advanced and targeted therapeutic approaches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence and awareness of endometriosis

- 3.2.1.2 Advancement in diagnostic techniques

- 3.2.1.3 Increased government fundings and initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Superficial peritoneal endometriosis

- 5.3 Ovarian endometriomas

- 5.4 Deep infiltrating endometriosis

- 5.5 Other disease types

Chapter 6 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hormone therapy

- 6.3 Pain medication

Chapter 7 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Gonadotropin releasing hormone

- 7.3 NSAIDs

- 7.4 Oral contraceptive

- 7.5 Other drug class

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Injectable

- 8.4 Other routes of administration

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AbbVie

- 11.2 Astellas Pharma

- 11.3 AstraZeneca

- 11.4 Bayer

- 11.5 Eli Lilly and Company

- 11.6 ObsEva

- 11.7 Pfizer

- 11.8 Teva Pharmaceutical Industries

- 11.9 TerSera Therapeutics

- 11.10 Zydus Healthcare Limited

子宫内膜异位症治疗市场规模、份额、趋势分析报告,按治疗类型、药物类别、给药途径、分销管道、地区、细分预测,2025-2030 年美国子宫内膜异位症治疗市场规模、份额、趋势分析报告,按治疗类型、药物类别、给药途径、分销管道、细分预测,2025-2030 年

子宫内膜异位症治疗市场规模、份额、趋势分析报告,按治疗类型、药物类别、给药途径、分销管道、地区、细分预测,2025-2030 年美国子宫内膜异位症治疗市场规模、份额、趋势分析报告,按治疗类型、药物类别、给药途径、分销管道、细分预测,2025-2030 年 2025-2033 年子宫内膜异位症市场报告(按类型、诊断和治疗、最终用户和地区)

2025-2033 年子宫内膜异位症市场报告(按类型、诊断和治疗、最终用户和地区) 子宫内膜异位症药物市场:按药物类型、治疗类型、分销管道划分 - 全球预测 2025-2030子宫内膜异位症药物市场:按药物类型、给药途径、患者特征和最终用户划分 - 全球预测 2025-2030

子宫内膜异位症药物市场:按药物类型、治疗类型、分销管道划分 - 全球预测 2025-2030子宫内膜异位症药物市场:按药物类型、给药途径、患者特征和最终用户划分 - 全球预测 2025-2030 全球子宫内膜异位症药物市场规模(按产品、应用、地区、范围和预测)

全球子宫内膜异位症药物市场规模(按产品、应用、地区、范围和预测) 子宫内膜异位症治疗市场 - 全球产业分析、规模、份额、成长、趋势和预测,2024-2034 年全球子宫内膜异位症治疗市场:预测(2024-2029)

子宫内膜异位症治疗市场 - 全球产业分析、规模、份额、成长、趋势和预测,2024-2034 年全球子宫内膜异位症治疗市场:预测(2024-2029)