|

市场调查报告书

商品编码

1698306

格林-巴利症候群诊断市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Guillain-Barre Syndrome Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

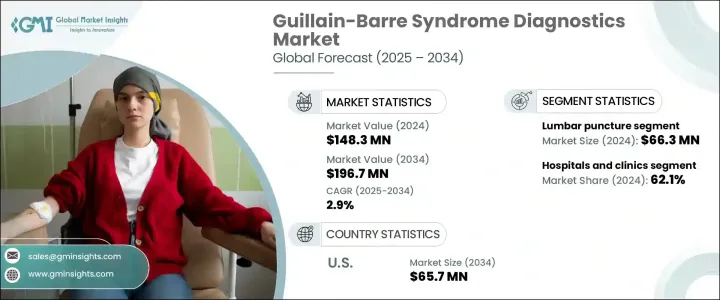

2024 年全球格林巴利症候群 (GBS) 诊断市场价值为 1.483 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 2.9%。这一增长得益于神经系统检测方法的进步和早期诊断意识的提高。自体免疫疾病盛行率的不断上升、诊断程序的可及性的提高以及医疗基础设施投资的不断增加都导致了这一上升趋势。随着医疗技术的发展,医疗保健提供者正致力于提高诊断准确性,以便及时干预,降低与格林-巴利综合症相关的严重併发症的风险。

格林巴利症候群是一种罕见的自体免疫疾病,患者免疫系统会错误地攻击週边神经。这会导致肌肉无力,严重时甚至会导致瘫痪。虽然确切病因尚不清楚,但病毒和细菌感染被认为是主要诱因。鑑于这种疾病的潜在严重性,早期发现至关重要,这推动了对先进诊断测试的需求。世界各地的医疗机构都优先进行格林-巴利综合症筛检,并整合最先进的设备以提高诊断精度。研究和开发计划也在促进创新,公司正在探索新的基于生物标记的测试方法,这可能会彻底改变诊断领域。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.483亿美元 |

| 预测值 | 1.967亿美元 |

| 复合年增长率 | 2.9% |

市场根据测试类型进行细分,包括腰椎穿刺、神经传导研究、肌电图和其他诊断方法。 2024 年,腰椎穿刺领域将引领市场,创造 6,630 万美元的产值。作为一项黄金标准诊断程序,腰椎穿刺可以进行脑脊髓液分析,透过检测升高的蛋白质水平和正常的白血球计数来帮助确认格林-巴利综合症。此方法因其可靠性和准确性而受到高度评价,因此成为医疗保健专业人士的首选。随着技术的不断进步,腰椎穿刺技术不断改进,确保了患者的治疗效果。

格林巴利症候群诊断的最终用途应用包括医院和诊所、诊断实验室和其他医疗机构。 2024 年,医院和诊所占据市场主导地位,占总份额的 62.1%。由于拥有专门的神经病学部门、经验丰富的医疗专业人员和尖端的诊断设备,这些设施仍然是格林-巴利综合症诊断的主要场所。神经学中心和综合医院进行大部分 GBS 测试,包括神经传导研究、肌电图和腰椎穿刺。医院内配备齐全的实验室可确保患者得到及时且准确的诊断,从而巩固了该领域的主导地位。

在美国,格林-巴利症候群诊断市场在 2023 年创造了 4,880 万美元的产值,预计到 2034 年将达到 6,570 万美元。格林-巴利综合症发病率的上升加大了诊断能力的提升力度,医疗保健提供者强调早期发现和介入。该国人口老化进一步促进了市场扩张,因为老年人罹患自体免疫疾病的风险增加。因此,对创新诊断解决方案的需求不断增长,促使製造商投资研发。扩大医疗保健政策和改善保险覆盖范围也在加速市场成长方面发挥作用,使得 GBS 诊断在美国医疗保健领域更容易获得。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 格林-巴利症候群发生率不断上升

- 人们对罕见疾病的认识不断提高

- 诊断技术的进步

- 人口老化加剧

- 产业陷阱与挑战

- 诊断费用高昂

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按测试类型,2021 年至 2034 年

- 主要趋势

- 腰椎穿刺

- 神经传导

- 肌电图

- 其他测试类型

第六章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院和诊所

- 诊断实验室

- 其他最终用途

第七章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第八章:公司简介

- Alpine Biomed

- Avanos

- Bionen Medical Devices

- Cadwell Industries

- Cardinal Health

- Clarity Medical

- Deymed Diagnostic

- EMS Biomedical

- Medtronic

- Natus Medical Incorporated

- Neurosoft

- Nihon Kohden

- Rochester Electro-Medical

The Global Guillain-Barre Syndrome (GBS) Diagnostics Market was valued at USD 148.3 million in 2024 and is projected to expand at a CAGR of 2.9% from 2025 to 2034. The growth is driven by advancements in neurological testing methods and rising awareness of early diagnosis. The increasing prevalence of autoimmune disorders, improved accessibility to diagnostic procedures, and growing investments in healthcare infrastructure contribute to this upward trend. As medical technology evolves, healthcare providers are focusing on enhancing diagnostic accuracy to facilitate timely intervention, reducing the risk of severe complications associated with GBS.

Guillain-Barre syndrome is a rare autoimmune condition in which the body's immune system erroneously attacks the peripheral nerves. This leads to muscle weakness and in severe cases, paralysis. Although the exact cause remains unknown, viral and bacterial infections are considered major triggers. Given the potential severity of the disorder, early detection is crucial, fueling demand for advanced diagnostic tests. Healthcare facilities worldwide are prioritizing GBS screening, integrating state-of-the-art equipment to improve diagnostic precision. Research and development initiatives are also fostering innovation, with companies exploring new biomarker-based testing approaches that could revolutionize the diagnostic landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $148.3 Million |

| Forecast Value | $196.7 Million |

| CAGR | 2.9% |

The market is segmented based on test types, including lumbar puncture, nerve conduction studies, electromyography, and other diagnostic methods. In 2024, the lumbar puncture segment led the market, generating USD 66.3 million. As a gold-standard diagnostic procedure, lumbar puncture enables cerebrospinal fluid analysis, which helps confirm GBS by detecting elevated protein levels with normal white blood cell counts. This method is highly regarded for its reliability and accuracy, making it the preferred choice among healthcare professionals. With ongoing technological advancements, lumbar puncture techniques continue to improve, ensuring enhanced patient outcomes.

End-use applications of Guillain-Barre syndrome diagnostics include hospitals and clinics, diagnostic laboratories, and other healthcare facilities. Hospitals and clinics dominated the market in 2024, accounting for 62.1% of the total share. These facilities remain the primary settings for GBS diagnosis due to the availability of specialized neurology units, experienced medical professionals, and cutting-edge diagnostic equipment. Neurology centers and general hospitals conduct the majority of GBS tests, including nerve conduction studies, electromyography, and lumbar punctures. The presence of well-equipped laboratories within hospitals ensures that patients receive prompt and accurate diagnoses, reinforcing the dominance of this segment.

In the United States, the Guillain-Barre syndrome diagnostics market generated USD 48.8 million in 2023 and is expected to reach USD 65.7 million by 2034. The rising incidence of GBS has intensified efforts to enhance diagnostic capabilities, with healthcare providers emphasizing early detection and intervention. The country's aging population further contributes to market expansion, as older individuals face an increased risk of developing autoimmune disorders. As a result, demand for innovative diagnostic solutions is growing, prompting manufacturers to invest in research and development. Expanding healthcare policies and improved insurance coverage are also playing a role in accelerating market growth, making GBS diagnostics more accessible across the US healthcare landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of Guillain-Barre syndrome

- 3.2.1.2 Growing awareness for the rare disease

- 3.2.1.3 Technological advancements in diagnostics

- 3.2.1.4 Rise in aging population

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High diagnostic costs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Lumbar puncture

- 5.3 Nerve conduction

- 5.4 Electromyography

- 5.5 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Diagnostic laboratories

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alpine Biomed

- 8.2 Avanos

- 8.3 Bionen Medical Devices

- 8.4 Cadwell Industries

- 8.5 Cardinal Health

- 8.6 Clarity Medical

- 8.7 Deymed Diagnostic

- 8.8 EMS Biomedical

- 8.9 Medtronic

- 8.10 Natus Medical Incorporated

- 8.11 Neurosoft

- 8.12 Nihon Kohden

- 8.13 Rochester Electro-Medical