|

市场调查报告书

商品编码

1698337

商用车座椅市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Commercial Vehicle Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

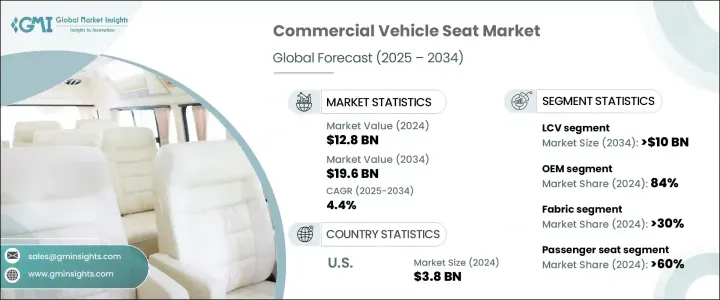

2024 年全球商用车座椅市场规模达到 128 亿美元,预计 2025 年至 2034 年期间将以 4.4% 的复合年增长率稳定成长。商用车需求的不断增长,尤其是在物流和运输领域,继续推动对耐用、符合人体工学的座椅解决方案的需求。汽车製造商和车队营运商优先考虑能够提高舒适性、安全性和使用寿命的高品质座椅,确保车辆满足驾驶员和乘客不断变化的期望。

在材料、设计和安全法规的进步推动下,市场正在经历一场转型。轻量化和节能的座椅解决方案越来越受到关注,特别是随着汽车行业转向电动和自动驾驶汽车。製造商正在整合高性能材料、智慧缓衝和自适应设计,以改善使用者体验,同时优化车辆重量和燃油效率。模组化座椅结构的采用也日益增多,从而可以根据应用需求实现更大的灵活性和客製化。此外,严格的安全标准要求不断创新,迫使汽车製造商开发符合全球监管框架的抗衝击、符合人体工学的座椅。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 128亿美元 |

| 预测值 | 196亿美元 |

| 复合年增长率 | 4.4% |

轻型商用车 (LCV) 领域仍然是商用车座椅市场的主导力量,到 2024 年将占据 55% 的市场份额。预计到 2034 年,该领域的产值将达到 100 亿美元,这得益于城市交通和最后一英里配送服务中使用的紧凑型、省油车辆的需求激增。随着城市化进程的加速,企业和物流供应商寻求能够轻鬆穿越拥挤城市景观的灵活交通解决方案。 LCV 兼具出色的机动性、燃油效率和成本效益,使其成为送货车队、共乘服务和租赁业务的首选。小型企业活动的扩大和电子商务的成长进一步加强了对先进座椅解决方案的需求,製造商专注于增强腰部支撑、改善座椅可调节性和可持续材料,以满足不断增长的消费者期望。

商用车座椅市场分为OEM和售后市场销售管道,其中 OEM 到 2024 年将占据 84% 的市场份额。汽车製造商绝大多数青睐符合品牌形象、品质基准和不断发展的安全法规的原厂安装座椅。原始设备製造商大力投资高端座椅解决方案,这些解决方案具有人体工学设计、高耐用性布料以及气候控制座椅、记忆功能和可调式腰部支撑等先进功能。这些创新不仅提高了驾驶舒适度,也提高了车辆的效率和使用寿命。随着汽车製造商面临提供卓越内装功能的压力,座椅製造商正在开发尖端解决方案,以满足驾驶员和乘客的需求,同时确保符合严格的安全标准。

北美商用车座椅市场占全球收入的 36%,其中美国在 2024 年的收入为 38 亿美元。这一领导地位源自于该国广泛的生产能力、强劲的汽车销售以及持续的研发投资。汽车製造商和供应商不断增强座椅功能,加入加热、通风和记忆设置,以满足不断变化的消费者偏好。美国仍然是市场趋势的重要推动者,影响着品质标准并塑造商用车座椅的创新。随着国内需求的不断发展,产业参与者专注于提供技术先进、符合安全要求且舒适度更高的座椅解决方案,以在全球市场上保持竞争优势。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 材料供应商

- 製造商

- 经销商

- 最终用途

- 利润率分析

- 供应商格局

- 技术与创新格局

- 专利分析

- 成本細項分析

- 监管格局

- 衝击力

- 成长动力

- 对轻量和人体工学座椅的需求不断增长

- 严格的安全和排放法规

- 电子商务和物流的成长

- 可持续材料的进步

- 产业陷阱与挑战

- 先进座椅技术成本高

- 供应链中断

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按座位,2021 - 2034

- 主要趋势

- 驾驶座椅

- 乘客座椅

- 后座

- 折迭座椅

第六章:市场估计与预测:依资料,2021 - 2034 年

- 主要趋势

- 织物

- 乙烯基塑料

- 皮革

- 合成材料

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 轻型商用车(LCV)

- 重型商用车(HCV)

- 巴士和长途客车

第八章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- 标准/常规座位

- 电动座椅

- 加热和通风座椅

- 记忆座椅

- 按摩座椅

第九章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Adient

- Brose Fahrzeugteile

- Daimler

- Faurecia

- Hyundai Dymos

- Iveco

- Kongsberg Automotive

- Kongsberg Gruppen

- Lear

- Magna International

- RECARO Automotive Seating

- Seoyon E-Hwa

- Sogefi Group

- Sumitomo Riko

- Sundaram Clayton

- Tachi-S

- Toyota Boshoku

- TS Tech

- Yanfeng Automotive Interiors

- Zhejiang Panyu-Jeep Vehicle

The Global Commercial Vehicle Seat Market reached USD 12.8 billion in 2024, with projections indicating steady growth at a CAGR of 4.4% from 2025 to 2034. The increasing demand for commercial vehicles, particularly within the logistics and transportation sectors, continues to drive the need for durable, ergonomic seating solutions. Automakers and fleet operators prioritize high-quality seats that enhance comfort, safety, and longevity, ensuring vehicles meet the evolving expectations of drivers and passengers alike.

The market is undergoing a transformation fueled by advancements in materials, design, and safety regulations. Lightweight and energy-efficient seat solutions are gaining traction, particularly as the industry pivots toward electric and autonomous vehicles. Manufacturers are integrating high-performance materials, smart cushioning, and adaptive designs to improve user experience while optimizing vehicle weight and fuel efficiency. The adoption of modular seating structures is also rising, allowing for greater flexibility and customization based on application needs. Additionally, stringent safety standards necessitate continuous innovation, compelling automakers to develop impact-resistant, ergonomic seating that complies with global regulatory frameworks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.8 Billion |

| Forecast Value | $19.6 Billion |

| CAGR | 4.4% |

The Light Commercial Vehicle (LCV) segment remains a dominant force in the commercial vehicle seat market, accounting for a 55% share in 2024. This segment is projected to generate USD 10 billion by 2034, driven by the surging demand for compact, fuel-efficient vehicles used in urban transport and last-mile delivery services. As urbanization accelerates, businesses and logistics providers seek agile transportation solutions capable of navigating congested cityscapes with ease. LCVs offer a compelling combination of maneuverability, fuel efficiency, and cost-effectiveness, making them the preferred choice for delivery fleets, ride-sharing services, and rental operations. Expanding small business activities and the growth of e-commerce further reinforce the need for advanced seating solutions, with manufacturers focusing on enhanced lumbar support, improved seat adjustability, and sustainable materials to meet the rising consumer expectations.

The commercial vehicle seat market is segmented into OEM and aftermarket sales channels, with OEMs securing an 84% market share in 2024. Automakers overwhelmingly favor factory-installed seats that align with brand identity, quality benchmarks, and evolving safety regulations. OEMs invest heavily in premium seating solutions featuring ergonomic designs, high-durability fabrics, and advanced features such as climate-controlled seating, memory functions, and adjustable lumbar support. These innovations not only enhance driving comfort but also improve vehicle efficiency and longevity. As automakers face mounting pressure to offer superior interior features, seat manufacturers are developing cutting-edge solutions that cater to both driver and passenger needs while ensuring compliance with stringent safety standards.

North America Commercial Vehicle Seat Market accounted for 36% of the global revenue, with the United States generating USD 3.8 billion in 2024. This leadership position stems from the country's expansive production capabilities, robust vehicle sales, and ongoing investment in research and development. Automakers and suppliers continuously enhance seat functionality, incorporating heating, ventilation, and memory settings to meet shifting consumer preferences. The US remains a critical driver of market trends, influencing quality standards and shaping innovation in commercial vehicle seating. As domestic demand continues to evolve, industry players focus on delivering technologically advanced, safety-compliant, and comfort-enhancing seating solutions to maintain a competitive edge in the global market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Material providers

- 3.1.1.2 Manufacturers

- 3.1.1.3 Distributors

- 3.1.1.4 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Cost breakdown analysis

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for lightweight and ergonomic seating

- 3.6.1.2 Stringent safety and emission regulations

- 3.6.1.3 Growth in e-commerce and logistics

- 3.6.1.4 Advancements in sustainable materials

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced seating technologies

- 3.6.2.2 Supply chain disruptions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Seat, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Driver seat

- 5.3 Passenger seat

- 5.4 Rear seat

- 5.5 Folding seat

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Fabric

- 6.3 Vinyl

- 6.4 Leather

- 6.5 Synthetic materials

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Light Commercial Vehicles (LCV)

- 7.3 Heavy Commercial Vehicles (HCV)

- 7.4 Buses & Coaches

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Standard/conventional seats

- 8.3 Powered/electric seats

- 8.4 Heated & ventilated seats

- 8.5 Memory seats

- 8.6 Massage seats

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Adient

- 11.2 Brose Fahrzeugteile

- 11.3 Daimler

- 11.4 Faurecia

- 11.5 Hyundai Dymos

- 11.6 Iveco

- 11.7 Kongsberg Automotive

- 11.8 Kongsberg Gruppen

- 11.9 Lear

- 11.10 Magna International

- 11.11 RECARO Automotive Seating

- 11.12 Seoyon E-Hwa

- 11.13 Sogefi Group

- 11.14 Sumitomo Riko

- 11.15 Sundaram Clayton

- 11.16 Tachi-S

- 11.17 Toyota Boshoku

- 11.18 TS Tech

- 11.19 Yanfeng Automotive Interiors

- 11.20 Zhejiang Panyu-Jeep Vehicle