|

市场调查报告书

商品编码

1698505

扁平材市场机会、成长动力、产业趋势分析及2025-2034年预测Flat Steel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

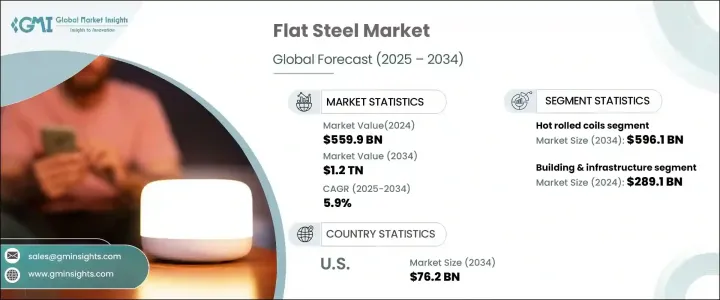

2024 年全球扁平钢市场规模将达到 5,599 亿美元,受建筑和汽车产业需求成长的推动,预计 2025 年至 2034 年期间复合年成长率将达到 5.9%。扁钢的成本效益、能源效率和环保特性使其成为各种应用的首选材料。随着各国政府和私人企业加大基础建设投资,高速公路、桥樑、大型交通工程对扁平材的需求持续上升。随着城市化和工业化的快速成长,市场参与者专注于创新和永续的生产技术,以满足不断变化的行业需求。

扁平材市场的扩张与汽车产业的进步密切相关,汽车製造商优先考虑轻质、高强度的材料,以提高燃油效率并满足严格的排放法规。向电动车的转变进一步扩大了电池外壳和结构部件对扁钢的需求。此外,先进金属涂层的使用日益增多,增强了耐腐蚀性,并延长了多个行业产品的使用寿命。由于消费者和製造商寻求耐用且节能的材料,家电产业也受益。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5599亿美元 |

| 预测值 | 1.2兆美元 |

| 复合年成长率 | 5.9% |

热轧捲仍将是主导产品类别,预计到 2034 年产值将达到 5,961 亿美元,复合年成长率为 7%。由于其多功能性和机械强度,这些线圈对于工业和结构应用是不可或缺的。同时,随着各行各业都强调能源效率,尤其是在变压器和电动马达领域,对电工钢板和电工钢带的需求也日益增加。随着全球能源标准越来越严格,电气应用领域对专用扁钢产品的需求将大幅成长。

建筑和基础设施领域在 2024 年达到 2,891 亿美元,占 55.3% 的市场占有率,预计 2025 年至 2034 年的复合年成长率为 6%。不断扩大的城市中心、大规模的住宅和商业开发以及政府主导的基础设施项目推动持续的需求。优质钢材因其耐用性、永续性和成本效益,在现代建筑中仍然不可或缺。同时,运输业采用扁平钢来提高车辆性能、减轻重量并最佳化燃料消耗。随着钢铁製造技术的进步,业界领导者正在推出符合严格品质标准的高强度、轻量钢材。

预计到 2034 年,美国扁平材市场规模将达到 762 亿美元,自 2024 年起的复合年成长率为 4.8%。经济和技术进步正在重塑该行业,从而推动高性能钢铁解决方案的采用。汽车和航太领域尤其推动了创新,因为製造商寻求能够增强结构完整性同时减轻重量的材料。此外,住宅和商业建筑项目投资的增加也持续增强需求。随着各行各业优先考虑现代化和永续的解决方案,扁平钢市场将稳步成长,主要参与者将专注于效率、可回收性和减少对环境的影响。

目录

第1章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第2章:执行摘要

第3章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和举措

- 监管格局

- 衝击力

- 产业衝击力

- 成长动力

- 加强基础建设

- 汽车产业需求不断成长

- 扩大再生能源项目

- 市场挑战

- 环境法规与永续发展压力

- 成长动力

- 法规和市场影响

- 波特的分析

- PESTEL 分析

第4章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第5章:市场规模及预测:依产品,2021-2034

- 主要趋势

- 热轧平板

- 热轧捲板

- 电工板材及带材

- 金属涂层钢板及带材

- 非金属涂层板材及带材

- 镀锡板

第6章:市场规模及预测:依最终用途,2021-2034

- 主要趋势

- 建筑和基础设施

- 汽车与运输

- 机械设备

- 电器

- 农业设备

- 气体容器

- 其他

第7章:市场规模及预测:依地区,2021-2034

- 主要趋势

- 北美洲

- 美国

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯联合大公国

第8章:公司简介

- Allegheny Technologies (ATI)

- ArcelorMittal

- China Steel Corporation

- Essar Steel

- Gerdau SA

- Hyundai Steel Co., Ltd.

- Nucor Corporation

- Nippon Steel & Sumitomo Metal Corporation (NSSMC)

- POSCO

- Severstal JSC

- Thyssenkrupp AG

- Tata Steel Limited

- Voestalpine Group

- Wuhan Iron & Steel Corporation (WISCO)

The Global Flat Steel Market reached USD 559.9 billion in 2024 and is set to expand at a CAGR of 5.9% between 2025 and 2034, driven by rising demand from the construction and automotive industries. Flat steel's cost-effectiveness, energy efficiency, and eco-friendly properties make it a preferred material across various applications. As governments and private enterprises worldwide increase infrastructure investments, the demand for flat steel in highways, bridges, and large-scale transportation projects continues to rise. With rapid urbanization and industrial growth, market players are focusing on innovation and sustainable production techniques to align with evolving industry needs.

The expansion of the flat steel market is closely linked to advancements in the automotive sector, where manufacturers prioritize lightweight, high-strength materials to improve fuel efficiency and meet stringent emission regulations. The shift toward electric vehicles further amplifies the demand for flat steel in battery casings and structural components. Additionally, the rising use of advanced metallic coatings enhances corrosion resistance, extending product lifespan across multiple industries. The appliance sector also benefits, as consumers and manufacturers seek durable and energy-efficient materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $559.9 Billion |

| Forecast Value | $1.2 Trillion |

| CAGR | 5.9% |

Hot rolled coils will remain a dominant product category, projected to generate USD 596.1 billion by 2034 at a CAGR of 7%. These coils are integral to industrial and structural applications due to their versatility and mechanical strength. Meanwhile, electrical sheets and strips are witnessing heightened demand as industries emphasize energy efficiency, particularly in transformers and electric motors. As global energy standards tighten, the need for specialized flat steel products in electrical applications is poised for significant growth.

The building and infrastructure segment accounted for USD 289.1 billion in 2024, capturing a 55.3% market share, and is projected to grow at a CAGR of 6% from 2025 to 2034. Expanding urban centers, large-scale residential and commercial developments, and government-led infrastructure projects drive consistent demand. Premium-grade steel remains essential in modern construction due to its durability, sustainability, and cost-effectiveness. Meanwhile, the transportation industry integrates flat steel to enhance vehicle performance, reduce weight, and optimize fuel consumption. With technological advancements in steel manufacturing, industry leaders are introducing high-strength, lightweight variants that meet stringent quality standards.

U.S. flat steel market is projected to reach USD 76.2 billion by 2034, growing at a CAGR of 4.8% from 2024. Economic and technological advancements are reshaping the industry, leading to increased adoption of high-performance steel solutions. The automotive and aerospace sectors, in particular, drive innovation as manufacturers seek materials that enhance structural integrity while minimizing weight. Additionally, rising investments in residential and commercial construction projects continue to reinforce demand. As industries prioritize modernized and sustainable solutions, the flat steel market is set for steady growth, with key players focusing on efficiency, recyclability, and reduced environmental impact.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.7 Industry impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing infrastructure development

- 3.7.1.2 Rising demand from the automotive sector

- 3.7.1.3 Expansion of renewable energy projects

- 3.7.2 Market challenges

- 3.7.2.1 Environmental regulations and sustainability pressures

- 3.7.1 Growth drivers

- 3.8 Regulations & market impact

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product, 2021-2034 (USD Billion) (Million Tons)

- 5.1 Key trends

- 5.2 Hot rolled flat sheets

- 5.3 Hot rolled coils

- 5.4 Electrical sheet & strip

- 5.5 Metallic coated sheet & strip

- 5.6 Non-metallic coated sheet & strip

- 5.7 Tin plates

Chapter 6 Market Size and Forecast, By End Use, 2021-2034 (USD Billion) (Million Tons)

- 6.1 Key trends

- 6.2 Building & infrastructure

- 6.3 Automotive & transportation

- 6.4 Mechanical equipment

- 6.5 Electrical appliances

- 6.6 Agriculture equipment

- 6.7 Gas containers

- 6.8 Others

Chapter 7 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Million Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allegheny Technologies (ATI)

- 8.2 ArcelorMittal

- 8.3 China Steel Corporation

- 8.4 Essar Steel

- 8.5 Gerdau S.A.

- 8.6 Hyundai Steel Co., Ltd.

- 8.7 Nucor Corporation

- 8.8 Nippon Steel & Sumitomo Metal Corporation (NSSMC)

- 8.9 POSCO

- 8.10 Severstal JSC

- 8.11 Thyssenkrupp AG

- 8.12 Tata Steel Limited

- 8.13 Voestalpine Group

- 8.14 Wuhan Iron & Steel Corporation (WISCO)

扁钢市场规模、份额、趋势及预测(依产品、材质、应用及地区划分),2026-2034年

扁钢市场规模、份额、趋势及预测(依产品、材质、应用及地区划分),2026-2034年 2026年全球扁钢市场报告2026年全球热处理钢市场报告

2026年全球扁钢市场报告2026年全球热处理钢市场报告 全球耐磨堆焊钢板市场(依材质类型、製程类型、焊接技术、涂层厚度、最终用途产业和应用划分)-2026-2032年预测复合碳化铬堆焊耐磨钢板市场:按应用、材质等级、形状、销售管道和最终用户产业划分-2026-2032年全球预测按木材类型、处理方法、用途和通路分類的热处理木材市场-2026年至2032年全球预测按连接方式、材料组合、应用、通路和最终用途产业分類的复合钢板市场-2026年至2032年全球预测碳化硅耐磨板市场:依製造流程、终端应用产业及通路划分-2026-2032年全球预测碳化钨耐磨板市场:按产品类型、等级、最终用途产业和分销管道划分 - 全球预测(2026-2032 年)铝钢复合板市场(按产品类型、厚度、硬化状态、复合技术、应用和最终用户划分),全球预测,2026-2032年

全球耐磨堆焊钢板市场(依材质类型、製程类型、焊接技术、涂层厚度、最终用途产业和应用划分)-2026-2032年预测复合碳化铬堆焊耐磨钢板市场:按应用、材质等级、形状、销售管道和最终用户产业划分-2026-2032年全球预测按木材类型、处理方法、用途和通路分類的热处理木材市场-2026年至2032年全球预测按连接方式、材料组合、应用、通路和最终用途产业分類的复合钢板市场-2026年至2032年全球预测碳化硅耐磨板市场:依製造流程、终端应用产业及通路划分-2026-2032年全球预测碳化钨耐磨板市场:按产品类型、等级、最终用途产业和分销管道划分 - 全球预测(2026-2032 年)铝钢复合板市场(按产品类型、厚度、硬化状态、复合技术、应用和最终用户划分),全球预测,2026-2032年