|

市场调查报告书

商品编码

1698522

流程编排市场机会、成长动力、产业趋势分析及 2025-2034 年预测Process Orchestration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

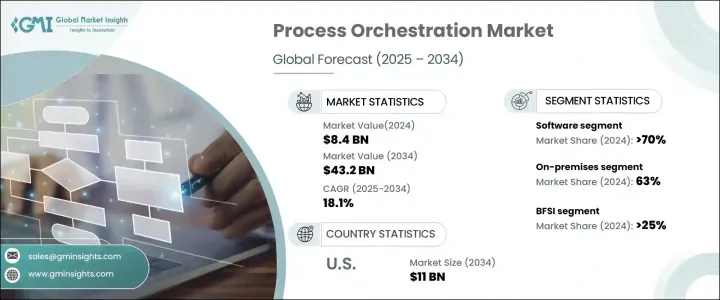

全球流程编排市场在 2024 年的价值为 84 亿美元,预计在 2025 年至 2034 年期间的复合年增长率将达到 18.1%,这得益于对自动化日益增长的需求,以提高营运效率并减少对手动任务的依赖。各行各业的组织都优先考虑人工智慧驱动的编排工具,以简化工作流程、提高生产力并实现即时决策。将人工智慧 (AI) 和机器学习 (ML) 融入工业流程对于实现自动化操作、降低成本和优化业务绩效至关重要。随着数位转型计画在全球范围内获得关注,企业越来越多地采用流程编排解决方案来提高灵活性、可扩展性和竞争力。

流程编排解决方案的需求受到多种因素的推动,包括云端运算的日益普及、法规遵循需求的不断增长以及智慧流程自动化的推动。当组织应对复杂的营运环境时,他们会寻求能够自动化工作流程、整合不同系统并提供数据驱动洞察的先进工具。公司正在投资人工智慧驱动的编排平台,以获得流程的即时可见性,从而实现预测分析和主动决策。这些解决方案不仅提高了效率,而且透过确保无缝、无错误的操作增强了客户体验。随着数位生态系统的不断发展,利用流程编排的企业将能够充分利用新兴机会并推动长期成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 84亿美元 |

| 预测值 | 432亿美元 |

| 复合年增长率 | 18.1% |

从市场构成来看,流程编排产业分为软体和服务。到 2024 年,软体产业将占据 70% 的市场份额,预计未来几年仍将保持强劲势头。可扩展、可自订且经济高效的软体解决方案在优化业务营运方面发挥关键作用。人工智慧和机器学习的整合使软体平台能够提供预测见解、自动执行重复性任务并促进数据驱动的决策。同时,随着企业越来越多地寻求实施和管理编排工具的专业支持,服务部门预计到 2034 年将以约 18% 的复合年增长率成长。

该市场还按行业垂直分类,主要行业包括 BFSI、医疗保健、零售和电子商务、IT、製造业、能源和公用事业、物流和公共部门。 2024 年,BFSI 部门占据了 25% 的市场份额,这得益于对高效、安全和自动化营运的需求,以管理复杂的金融交易和监管要求。随着金融机构努力提升客户体验和提高营运效率,流程编排解决方案对于即时资料处理、诈欺侦测和风险管理变得至关重要。

从地区来看,北美引领全球流程编排市场,2024 年创造 26 亿美元的收入。到 2034 年,该区域市场预计将达到 110 亿美元,其中美国将占据主导地位。该国拥有强大的技术基础设施和高度集中的领先技术提供者。 BFSI、医疗保健和零售等行业处于采用编排解决方案的前沿,利用自动化来简化营运并提高效率。政府支持数位转型的倡议进一步加速了流程编排工具的采用,巩固了该地区在市场上的领导地位。透过对创新和产品开发的持续投资,北美仍然是全球流程编排领域的主要成长动力。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 软体供应商

- 服务提供者

- 经销商

- 最终用途

- 供应商格局

- 利润率分析

- 专利格局

- 成本明细

- 技术与创新格局

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 业务流程中越来越多地采用自动化和人工智慧

- 对即时营运效率和流程优化的需求不断增长

- 各产业数位转型措施的成长

- 低程式码/无程式码平台的扩展,实现更广泛的可访问性

- 产业陷阱与挑战

- 中小企业实施成本高

- 流程编排与遗留系统整合的复杂性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 软体

- 服务

- 专业服务

- 託管服务

第六章:市场估计与预测:按部署,2021 - 2034 年

- 主要趋势

- 本地

- 基于云端

第七章:市场估计与预测:依组织规模,2021 - 2032 年

- 主要趋势

- 中小企业(SME)

- 大型企业

第八章:市场估计与预测:按产业垂直划分,2021 - 2032 年

- 主要趋势

- 金融服务业

- 卫生保健

- 零售与电子商务

- IT产业

- 製造业

- 能源与公用事业

- 后勤

- 公部门

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Appian

- BMC Software

- CA Technologies

- Camunda

- Celonis

- Cortex

- Dell Technologies

- Fujitsu

- HCL Technologies

- IBM

- Kyndryl

- Micro Focus

- Microsoft

- Newgen Software

- Oracle

- Pega

- SAP

- ServiceNow

- Software AG

- Wipro

The Global Process Orchestration Market, valued at USD 8.4 billion in 2024, is projected to expand at a CAGR of 18.1% from 2025 to 2034, driven by the increasing demand for automation to enhance operational efficiency and reduce reliance on manual tasks. Organizations across industries are prioritizing AI-driven orchestration tools to streamline workflows, improve productivity, and enable real-time decision-making. The integration of artificial intelligence (AI) and machine learning (ML) into industrial processes has become essential for automating operations, reducing costs, and optimizing business performance. With digital transformation initiatives gaining traction worldwide, businesses are increasingly adopting process orchestration solutions to enhance agility, scalability, and competitiveness.

The demand for process orchestration solutions is fueled by several factors, including the rising adoption of cloud computing, the growing need for regulatory compliance, and the push for intelligent process automation. As organizations navigate complex operational landscapes, they seek advanced tools that can automate workflows, integrate disparate systems, and deliver data-driven insights. Companies are investing in AI-powered orchestration platforms to gain real-time visibility into processes, allowing for predictive analytics and proactive decision-making. These solutions not only improve efficiency but also enhance customer experience by ensuring seamless, error-free operations. As digital ecosystems continue to evolve, businesses that leverage process orchestration will be well-positioned to capitalize on emerging opportunities and drive long-term growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $43.2 Billion |

| CAGR | 18.1% |

In terms of market components, the process orchestration industry is segmented into software and services. The software segment accounted for 70% of the market share in 2024, with strong momentum expected to continue in the coming years. Scalable, customizable, and cost-effective software solutions play a pivotal role in optimizing business operations. The integration of AI and ML enables software platforms to provide predictive insights, automate repetitive tasks, and facilitate data-driven decision-making. Meanwhile, the services segment is projected to grow at a CAGR of approximately 18% through 2034 as organizations increasingly seek specialized support for implementing and managing orchestration tools.

The market is also categorized by industry verticals, with key sectors including BFSI, healthcare, retail and e-commerce, IT, manufacturing, energy and utilities, logistics, and the public sector. The BFSI segment held a 25% market share in 2024, driven by the need for efficient, secure, and automated operations to manage complex financial transactions and regulatory requirements. As financial institutions strive to enhance customer experience and improve operational efficiency, process orchestration solutions are becoming essential for real-time data processing, fraud detection, and risk management.

Regionally, North America leads the global process orchestration market, generating USD 2.6 billion in revenue in 2024. By 2034, the regional market is projected to reach USD 11 billion, with the United States playing a dominant role. The country benefits from a strong technological infrastructure and a high concentration of leading technology providers. Industries such as BFSI, healthcare, and retail are at the forefront of adopting orchestration solutions, leveraging automation to streamline operations and improve efficiency. Government initiatives supporting digital transformation further accelerate the adoption of process orchestration tools, reinforcing the region's leadership in the market. With ongoing investments in innovation and product development, North America remains a key growth driver in the global process orchestration landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Software providers

- 3.1.2 Service providers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Patent landscape

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing adoption of automation and AI in business processes

- 3.9.1.2 Rising demand for real-time operational efficiency and process optimization

- 3.9.1.3 Growth in digital transformation initiatives across industries

- 3.9.1.4 Expansion of low-code/no-code platforms enabling broader accessibility

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High implementation costs for small and medium-sized enterprises (SME)

- 3.9.2.2 Complexity in integrating process orchestration with legacy systems

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-Based

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2032 ($Bn)

- 7.1 Key trends

- 7.2 Small and Medium-Sized Enterprises (SME)

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021 - 2032 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Healthcare

- 8.4 Retail & e-Commerce

- 8.5 IT Sector

- 8.6 Manufacturing

- 8.7 Energy & utilities

- 8.8 Logistics

- 8.9 Public sector

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Appian

- 10.2 BMC Software

- 10.3 CA Technologies

- 10.4 Camunda

- 10.5 Celonis

- 10.6 Cortex

- 10.7 Dell Technologies

- 10.8 Fujitsu

- 10.9 HCL Technologies

- 10.10 IBM

- 10.11 Kyndryl

- 10.12 Micro Focus

- 10.13 Microsoft

- 10.14 Newgen Software

- 10.15 Oracle

- 10.16 Pega

- 10.17 SAP

- 10.18 ServiceNow

- 10.19 Software AG

- 10.20 Wipro

2026年全球流程协作市场报告

2026年全球流程协作市场报告 流程协作市场:依产品类型、技术、应用、最终用户和通路划分-2026-2032年全球预测

流程协作市场:依产品类型、技术、应用、最终用户和通路划分-2026-2032年全球预测 流程协作市场 - 全球产业规模、份额、趋势、机会及预测(按组件、组织规模、部署、垂直产业、地区和竞争格局划分,2021-2031 年)

流程协作市场 - 全球产业规模、份额、趋势、机会及预测(按组件、组织规模、部署、垂直产业、地区和竞争格局划分,2021-2031 年) 流程协作市场规模、份额和成长分析(按组件、部署类型、企业规模、最终用途和地区划分)-2026-2033年产业预测

流程协作市场规模、份额和成长分析(按组件、部署类型、企业规模、最终用途和地区划分)-2026-2033年产业预测 流程协作市场规模、份额、趋势分析报告:按组件、按部署、按公司规模、按最终用途、按地区、按细分市场、预测,2025-2030 年

流程协作市场规模、份额、趋势分析报告:按组件、按部署、按公司规模、按最终用途、按地区、按细分市场、预测,2025-2030 年 流程协作市场:各零件,各部署,不同企业规模,各业界,各地区,2024年~2031年

流程协作市场:各零件,各部署,不同企业规模,各业界,各地区,2024年~2031年