|

市场调查报告书

商品编码

1698584

蜂蜡市场机会、成长动力、产业趋势分析及 2025-2034 年预测Beeswax Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

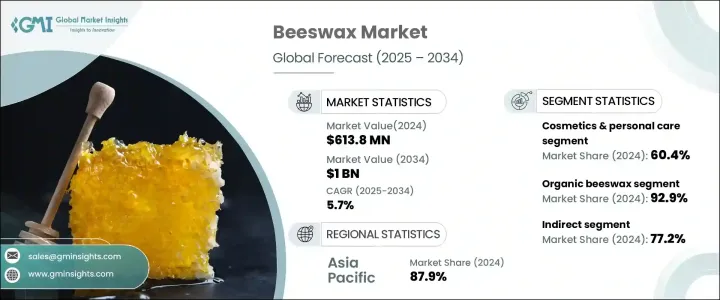

2024 年全球蜂蜡市场价值为 6.138 亿美元,预计 2025 年至 2034 年的复合年增长率为 5.7%。推动市场成长的主要因素是对天然和永续产品的需求不断增长,尤其是在美容、医疗保健和食品领域。随着消费者越来越意识到其对环境的影响,他们越来越多地转向有机和无化学替代品,尤其是在美容和个人护理产品方面。蜂蜡因其保湿和保护特性在个人护理中发挥着至关重要的作用,使其成为润唇膏、乳液和乳霜等产品中的关键成分。此外,它的抗菌和抗炎特性使其成为医用药膏和伤口护理产品中备受追捧的成分。

市场主要分为两种:有机蜂蜡和传统蜂蜡。有机蜂蜡处于领先地位,到 2024 年将占据近 93% 的市场份额,这得益于其在化妆品和个人护理产品中的广泛应用。由于其保湿和保护皮肤的特性,它被认为是护肤产品配方中必不可少的成分,而且由于消费者对天然、无农药产品的偏好日益增加,它的受欢迎程度也越来越高。随着越来越多的人不再使用塑胶替代品,蜂蜡在蜂蜡包装等环保食品包装中的作用日益增强,也促进了其需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6.138亿美元 |

| 预测值 | 10亿美元 |

| 复合年增长率 | 5.7% |

在市场应用方面,美容和个人护理领域占有最大份额,占2024年整个市场的60%以上。蜂蜡因其保持水分和提供皮肤保护的能力而被广泛用于润唇膏和保湿霜等产品中。然而,由于价格波动和素食替代品的竞争,市场面临挑战。儘管存在这些障碍,对天然配方的需求仍在持续增长,特别是随着消费者的环保意识增强并倾向于有机成分。

在分销方面,间接通路占据最大的市场份额,占总份额的77%以上。其中包括批发商和分销商,他们在推动化妆品、食品包装和蜡烛等各个领域的产品供应方面发挥着重要作用。亚太地区对蜂蜡的需求尤其高,占全球收入的近 88%。这种激增归因于可支配收入增加、城市化进程加快以及对永续产品的偏好日益增长等因素。此外,受提倡使用天然成分和永续实践的政策推动,北美也出现了类似的趋势。

目录

第一章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

- 初步研究和验证

- 主要来源

- 资料探勘来源

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 对天然和永续产品的需求不断增加

- 化妆品和个人护理行业

- 健康和医疗应用

- 产业陷阱与挑战

- 环境问题和蜜蜂数量下降

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 有机蜂蜡

- 常规蜂蜡

第六章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 化妆品和个人护理

- 製药

- 食品和饮料

- 工业和製造业

- 其他的

第七章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直接的

- 间接

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Bacofoil

- Charlotte Tilbury Source

- Koster Keunen LLC

- Strahl and Pitsch

- Hilltop

- British Wax Refining Company

- New Zealand Beeswax Ltd.

- Gustav Heess GmbH

The Global Beeswax Market was valued at USD 613.8 million in 2024 and is projected to grow at a CAGR of 5.7% from 2025 to 2034. The primary factor driving the market's growth is the increasing demand for natural and sustainable products, particularly in the beauty, healthcare, and food sectors. With consumers becoming more conscious of their environmental impact, there's a growing shift toward organic and chemical-free alternatives, especially in beauty and personal care products. Beeswax plays a vital role in personal care due to its moisturizing and protective properties, making it a key ingredient in items like lip balms, lotions, and creams. Furthermore, its antibacterial and anti-inflammatory benefits have made it a sought-after element in medical ointments and wound care products.

The market is categorized into two main types: organic beeswax and conventional beeswax. Organic beeswax is leading, making up nearly 93% of the market share in 2024, driven by its widespread use in cosmetics and personal care products. It's considered essential in the formulation of skincare products due to its moisturizing and skin-protecting properties, and its popularity is fueled by a rising consumer preference for natural, pesticide-free products. Beeswax's increasing role in eco-friendly food packaging, like beeswax wraps, has also contributed to its demand, as more people move away from plastic alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $613.8 Million |

| Forecast Value | $1 Billion |

| CAGR | 5.7% |

In terms of market applications, the beauty and personal care sector holds the largest share, accounting for over 60% of the total market in 2024. Beeswax is widely used in products such as lip balms and moisturizers because of its ability to retain moisture and provide skin protection. However, the market faces challenges due to price fluctuations and the competition from vegan substitutes. Despite these hurdles, the demand for natural formulations continues to grow, especially as consumers become more eco-conscious and inclined toward organic ingredients.

In terms of distribution, indirect channels account for the largest portion of the market, making up over 77% of the total share. These include wholesalers and distributors who play a significant role in driving product availability in various sectors, including cosmetics, food packaging, and candles. The demand for beeswax is especially high in the Asia Pacific region, which represents nearly 88% of the global revenue. This surge is attributed to factors like rising disposable income, increased urbanization, and a growing preference for sustainable products. Additionally, North America is seeing similar trends, driven by policies that promote the use of natural ingredients and sustainable practices.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for natural and sustainable products

- 3.6.1.2 Cosmetics and personal care industry

- 3.6.1.3 Health and medicinal applications

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental concerns and bee population decline

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Organic beeswax

- 5.3 Conventional beeswax

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cosmetics and personal care

- 6.3 Pharmaceuticals

- 6.4 Food and beverages

- 6.5 Industrial and manufacturing

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bacofoil

- 9.2 Charlotte Tilbury Source

- 9.3 Koster Keunen LLC

- 9.4 Strahl and Pitsch

- 9.5 Hilltop

- 9.6 British Wax Refining Company

- 9.7 New Zealand Beeswax Ltd.

- 9.8 Gustav Heess GmbH