|

市场调查报告书

商品编码

1699242

一次性温度计市场机会、成长动力、产业趋势分析及2025-2034年预测Disposable Thermometer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

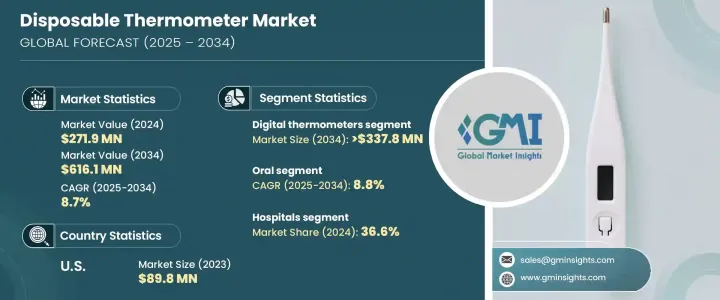

2024 年全球一次性温度计市场价值为 2.719 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.7%。不断增长的医疗保健需求、医疗技术的进步以及对感染控制的日益关注是市场扩张的主要驱动力。医院和诊所越来越多地采用一次性温度计来预防医院内感染。在新冠疫情期间,一次性温度计的需求激增,凸显了其在预防感染方面的重要性。随着人口老化和慢性病病例的增加,越来越多的人依赖一次性温度计进行常规健康监测。

由于技术进步,这些设备现在更加准确和用户友好,使其成为临床和家庭医疗保健环境的首选。随着家庭医疗保健的普及,尤其是在已开发国家,一次性温度计正成为不可或缺的工具。消费者青睐这些温度计,因为它们方便、安全且价格实惠,而越来越多的人将它们放入旅行和急救医疗包中。可支配收入的增加也促进了医疗保健支出,促进了市场成长。预计可支配收入和医疗支出之间的相关性将在未来几年加强对这些温度计的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.719亿美元 |

| 预测值 | 6.161亿美元 |

| 复合年增长率 | 8.7% |

市场按类型分为数位温度计和条形温度计,其中数位部分预计将以 8.5% 的复合年增长率扩张,到 2034 年将达到 3.378 亿美元以上。由于数位温度计的准确性、速度和易用性有所提高,消费者正在从传统温度计转向数位温度计。医疗保健提供者青睐使用数位温度计来最大限度地降低交叉污染风险,特别是在医院、诊所和疗养院。这场疫情进一步加速了它们在工作场所、学校和公共场所的采用。感测器技术的进步提高了准确性和反应时间,增加了医疗专业人员和家庭用户的可靠性。患有慢性疾病且需要经常监测体温的人更喜欢使用数位温度计,因为它们便于携带且高效。

根据目标区域,市场分为口腔、腋窝、直肠和其他部分,口腔温度计预计到 2034 年将达到 1.926 亿美元以上,复合年增长率为 8.8%。口腔温度计由于其易于使用和读数可靠,仍然是家庭和医疗机构的热门选择。它们舒适、经济高效,是医院感染控制的广泛选择。疫情期间对卫生的高度重视刺激了重症监护区对一次性口腔温度计的需求。

根据最终用途,市场分为医院、诊断中心、家庭护理和其他环境。受严格的卫生规程和有效感染控制需求的推动,医院在 2024 年占据了 36.6% 的最大市场份额。疫情进一步凸显了急诊室、加护病房和新生儿病房对一次性温度计的必要性。这些温度计无需每次使用之间进行消毒,从而节省了时间和资源,提供了一种经济高效的解决方案。

在美国,2021 年一次性温度计市场价值为 8,080 万美元。该国在 2023 年以 8,980 万美元的规模领先北美市场,高于 2022 年的 8,500 万美元。感染控制措施仍然是医疗机构的首要任务,越来越依赖一次性温度计来防止交叉污染。传染病、季节性疾病和慢性病的增加进一步推动了需求。人口老化以及医疗保健需求的增加导致医院和家庭医疗保健机构越来越多地采用一次性温度计。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 日益重视感染预防和控制

- 院内感染(HAI)增多

- 严格的医疗保健和卫生法规

- 居家照护服务需求不断成长

- 技术进步

- 产业陷阱与挑战

- 替代品的可用性

- 技术限制

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 差距分析

- 波特的分析

- PESTEL分析

- 未来市场趋势

- 价值链分析

- 一次性口腔体温计临床应用概况

- 不同体温测量技术的准确性与功能展望

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 数位温度计

- 条形温度计

第六章:市场估计与预测:按目标区域,2021 - 2034 年

- 主要趋势

- 口服

- 腋窝

- 直肠

- 其他目标区域

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 诊断中心

- 居家护理

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- 3M

- Acme United Corporation

- Advanced Meditech Internationals (AMI)

- American Diagnostics Corporation

- FIRST AID ONLY

- graham field

- HB Instrument

- Hopkins Medical Products

- LCR Hallcrest

- MEDICAL INDICATORS

- MEDLINE

- microlife corporation

- Protontek

- tempagenix

- Zeal

The Global Disposable Thermometer Market was valued at USD 271.9 million in 2024 and is projected to grow at a CAGR of 8.7% from 2025 to 2034. Increasing healthcare demands, advancements in medical technology, and the growing focus on infection control are key drivers of market expansion. Hospitals and clinics are increasingly adopting single-use thermometers to prevent hospital-acquired infections. The demand for disposable thermometers surged during the COVID-19 pandemic, reinforcing their importance in infection prevention. With aging populations and rising chronic disease cases, more people are relying on disposable thermometers for routine health monitoring.

These devices are now more accurate and user-friendly due to technological advancements, making them a preferred choice for both clinical and home healthcare settings. As home-based medical care gains traction, particularly in developed nations, disposable thermometers are becoming essential tools. Consumers favor these thermometers for their convenience, safety, and affordability, while more individuals include them in travel and emergency medical kits. Rising disposable income is also boosting healthcare spending, contributing to market growth. The correlation between disposable income and medical expenditures is expected to strengthen demand for these thermometers in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $271.9 Million |

| Forecast Value | $ 616.1 Million |

| CAGR | 8.7% |

The market is segmented by type into digital and strip thermometers, with the digital segment projected to expand at a CAGR of 8.5%, reaching over USD 337.8 million by 2034. Consumers are shifting from traditional to digital thermometers due to their improved accuracy, speed, and ease of use. Healthcare providers favor digital thermometers to minimize cross-contamination risks, particularly in hospitals, clinics, and nursing homes. The pandemic further accelerated their adoption in workplaces, schools, and public spaces. Advancements in sensor technology have enhanced accuracy and response times, increasing reliability for both medical professionals and home users. Individuals with chronic conditions requiring frequent temperature monitoring prefer digital thermometers for their portability and efficiency.

Based on target area, the market is categorized into oral, axilla, rectal, and other segments, with oral thermometers expected to reach over USD 192.6 million by 2034 at a CAGR of 8.8%. Oral thermometers remain a popular choice for homes and healthcare facilities due to their ease of use and reliable readings. They are comfortable, cost-effective, and widely preferred in hospitals for infection control. The heightened focus on hygiene during the pandemic fueled demand for disposable oral thermometers in critical care areas.

By end use, the market is divided into hospitals, diagnostic centers, homecare, and other settings. Hospitals held the largest market share of 36.6% in 2024, driven by stringent hygiene protocols and the need for efficient infection control. The pandemic reinforced the necessity of disposable thermometers in emergency rooms, intensive care units, and neonatal wards. These thermometers offer a cost-effective solution by eliminating the need for sterilization between uses, saving time and resources.

In the U.S., the disposable thermometer market was valued at USD 80.8 million in 2021. The country led the North America market in 2023 with USD 89.8 million, up from USD 85 million in 2022. Infection control measures remain a priority for healthcare facilities, increasing reliance on single-use thermometers to prevent cross-contamination. The rise in infectious diseases, seasonal illnesses, and chronic conditions has further propelled demand. An aging population with higher healthcare needs has led to greater adoption of disposable thermometers in hospitals and home healthcare settings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing emphasis on infection prevention and control

- 3.2.1.2 Rising hospital acquired infections (HAIs)

- 3.2.1.3 Strict healthcare and sanitation regulations

- 3.2.1.4 Rising demand for home-based care services

- 3.2.1.5 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Availability of substitutes

- 3.2.2.2 Technical limitation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Value chain analysis

- 3.11 Overview on disposable oral thermometer in clinical use

- 3.12 Outlook on the accuracy and function of different thermometry techniques for measuring body temperature

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Digital thermometers

- 5.3 Strip thermometers

Chapter 6 Market Estimates and Forecast, By Target Area, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Axilla

- 6.4 Rectal

- 6.5 Other target areas

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic centers

- 7.4 Homecare

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 Acme United Corporation

- 9.3 Advanced Meditech Internationals (AMI)

- 9.4 American Diagnostics Corporation

- 9.5 FIRST AID ONLY

- 9.6 graham field

- 9.7 H-B Instrument

- 9.8 Hopkins Medical Products

- 9.9 LCR Hallcrest

- 9.10 MEDICAL INDICATORS

- 9.11 MEDLINE

- 9.12 microlife corporation

- 9.13 Protontek

- 9.14 tempagenix

- 9.15 Zeal

温度计市场:按产品、红外线和应用划分-全球预测,2026-2032年SF6露点分析仪市场:依应用程式、产品类型、终端用户产业、侦测方式、通路划分,全球预测(2026-2032年)冷却镜式SF6露点仪市场:按类型、技术、应用和最终用户划分,全球预测,2026-2032年冷却镜露点仪市场:依露点范围、安装类型、校准类型、终端用户产业、应用程式和销售管道-全球预测,2026-2032年宠物体温计市场:依产品类型、动物类型、通路和最终用户划分-2025-2032年全球预测

温度计市场:按产品、红外线和应用划分-全球预测,2026-2032年SF6露点分析仪市场:依应用程式、产品类型、终端用户产业、侦测方式、通路划分,全球预测(2026-2032年)冷却镜式SF6露点仪市场:按类型、技术、应用和最终用户划分,全球预测,2026-2032年冷却镜露点仪市场:依露点范围、安装类型、校准类型、终端用户产业、应用程式和销售管道-全球预测,2026-2032年宠物体温计市场:依产品类型、动物类型、通路和最终用户划分-2025-2032年全球预测 全球参考温度计市场全球露点仪市场

全球参考温度计市场全球露点仪市场 全球数位电子体温计市场规模(按产品类型、应用、最终用户、区域范围和预测)

全球数位电子体温计市场规模(按产品类型、应用、最终用户、区域范围和预测) 温度计市场规模、份额、成长分析、按产品、按应用、按地区 - 产业预测,2025-2032 年实验室温度计的全球市场

温度计市场规模、份额、成长分析、按产品、按应用、按地区 - 产业预测,2025-2032 年实验室温度计的全球市场