|

市场调查报告书

商品编码

1699307

商业电压调节器市场机会、成长动力、产业趋势分析及 2025-2034 年预测Commercial Voltage Regulator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

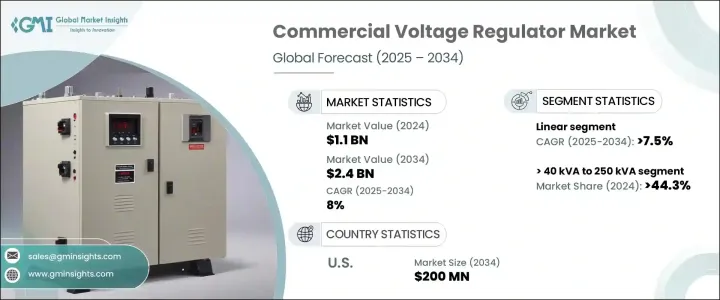

2024 年全球商用电压调节器市场规模达到 11 亿美元,预计 2025 年至 2034 年的复合年增长率为 8%。推动这一增长的因素包括对电能品质管理的日益重视以及对保护精密设备的需求日益增加。世界各地的企业都在投资先进的电力稳定技术,以防止中断并确保无缝运作。对人工智慧驱动的电压稳定的日益依赖正在进一步彻底改变产业,提高能源管理系统的效率、自动化和可靠性。政府在提高能源效率方面也发挥关键作用,鼓励采用电压调节器来优化能源消耗并降低营运成本。向数位化和可程式电压调节系统的转变正在增强各行业的电力稳定性,促进市场扩张。

对高效能电压调节解决方案的需求不断增长,推动了线性和开关调节器的采用。按产品进行市场细分凸显了这些先进电源管理解决方案的不断扩大的影响力。线性电压调节器以其精确度和低噪音运作而闻名,在医疗技术、电信和航太等需要高精度的行业中越来越受欢迎。预计到 2034 年,该领域的复合年增长率将达到 7.5%,凸显了其在敏感应用中维持稳定电压供应的关键作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 11亿美元 |

| 预测值 | 24亿美元 |

| 复合年增长率 | 8% |

基于电压的细分将市场分为三个主要组别:<= 40 kVA、> 40 kVA 至 250 kVA 和 > 250 kVA。其中,> 40 kVA 至 250 kVA 部分在 2024 年占据 44.3% 的主导市场份额,凸显了对中型电力解决方案的日益依赖。商业基础设施的扩张,特别是医疗保健和资料中心等领域的扩张,正在加速对这些监管机构的需求。随着企业优先考虑不间断供电和高效的能源分配,电力基础设施的投资持续增加,并加强了商业应用的市场渗透率。商业空间日益数位化,加上对电力系统的依赖性增强,预计将维持该领域的强劲成长。

美国商用电压调节器市场也正在强劲扩张,2024年市场规模将达到1.104亿美元,预计2034年将超过2亿美元。美国资料中心和医疗设施的快速发展,推动了对稳定且高效的配电解决方案的需求。旨在提高能源效率的政府措施和资助计画正在进一步推动产业进步。对不间断能源供应的日益增长的需求,加上人工智慧驱动的电压稳定技术的创新,将为美国市场在未来十年的持续成长奠定基础。该地区的企业正在投资尖端的电压调节解决方案,以提高运作可靠性、减少能源浪费并确保电力管理的长期永续性。

目录

第一章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依产品,2021 年至 2034 年

- 主要趋势

- 线性

- 交换

第六章:市场规模及预测:依阶段,2021 年至 2034 年

- 主要趋势

- 单相

- 三相

第七章:市场规模及预测:按电压,2021 年至 2034 年

- 主要趋势

- ≤40千伏安

- > 40 千伏安至 250 千伏安

- > 250千伏安

第八章:市场规模及预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 西班牙

- 荷兰

- 奥地利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 马来西亚

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 埃及

- 南非

- 奈及利亚

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 秘鲁

- 阿根廷

第九章:公司简介

- Analog Devices

- Basler Electric Company

- Eaton

- General Electric

- Hindustan Power Control System

- Infineon Technologies AG

- Legrand

- MaxLinear

- Microchip Technology Inc.

- NXP Semiconductors

- Renesas Electronics Corporation

- Ricoh USA

- Selvon Instruments

- SEMTECH

- Siemens Energy

- Sollatek

- STMicroelectronics

- TOREX SEMICONDUCTOR

- Vicor

- Vishay Intertechnology, Inc.

The Global Commercial Voltage Regulator Market reached USD 1.1 billion in 2024 and is estimated to grow at a CAGR of 8% from 2025 to 2034. The growth is driven by the rising emphasis on power quality management and the increasing need to protect precision equipment. Businesses worldwide are investing in advanced power stabilization technologies to prevent disruptions and ensure seamless operations. The growing reliance on AI-driven voltage stabilization is further revolutionizing the industry, offering improved efficiency, automation, and reliability in energy management systems. Governments are also playing a critical role in promoting energy efficiency, encouraging the adoption of voltage regulators to optimize energy consumption and reduce operational costs. The transition toward digital and programmable voltage regulation systems is enhancing power stability across industries, fostering market expansion.

The increasing demand for high-performance voltage regulation solutions is propelling the adoption of both linear and switching regulators. Market segmentation by product highlights the expanding footprint of these advanced power management solutions. Linear voltage regulators, known for their precision and low-noise operation, are gaining traction in industries requiring high accuracy, such as medical technology, telecommunications, and aerospace. This segment is expected to witness a CAGR of 7.5% through 2034, underscoring its critical role in maintaining a stable voltage supply in sensitive applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 8% |

Voltage-based segmentation categorizes the market into three key groups: <= 40 kVA, > 40 kVA to 250 kVA, and > 250 kVA. Among these, the > 40 kVA to 250 kVA segment held a dominant 44.3% market share in 2024, highlighting the increasing reliance on medium-scale power solutions. The expansion of commercial infrastructure, particularly in sectors such as healthcare and data centers, is accelerating demand for these regulators. With businesses prioritizing uninterrupted power supply and efficient energy distribution, investments in power infrastructure continue to rise, strengthening market penetration across commercial applications. The growing digitalization of commercial spaces, coupled with the heightened dependency on electrical systems, is expected to sustain robust growth in this segment.

The U.S. commercial voltage regulator market is also witnessing strong expansion, with market size reaching USD 110.4 million in 2024 and expected to surpass USD 200 million by 2034. The country's rapid development of data centers and healthcare facilities is fueling demand for stable and efficient power distribution solutions. Government initiatives and funding programs aimed at improving energy efficiency are further driving industry advancements. The increasing need for uninterrupted energy supply, along with innovations in AI-driven voltage stabilization, is positioning the U.S. market for sustained growth over the next decade. Businesses across the region are investing in cutting-edge voltage regulation solutions to enhance operational reliability, reduce energy wastage, and ensure long-term sustainability in power management.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Linear

- 5.3 Switching

Chapter 6 Market Size and Forecast, By Phase, 2021 – 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Voltage, 2021 – 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 ≤ 40 kVA

- 7.3 > 40 kVA to 250 kVA

- 7.4 > 250 kVA

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 New Zealand

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Kuwait

- 8.5.8 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 Analog Devices

- 9.2 Basler Electric Company

- 9.3 Eaton

- 9.4 General Electric

- 9.5 Hindustan Power Control System

- 9.6 Infineon Technologies AG

- 9.7 Legrand

- 9.8 MaxLinear

- 9.9 Microchip Technology Inc.

- 9.10 NXP Semiconductors

- 9.11 Renesas Electronics Corporation

- 9.12 Ricoh USA

- 9.13 Selvon Instruments

- 9.14 SEMTECH

- 9.15 Siemens Energy

- 9.16 Sollatek

- 9.17 STMicroelectronics

- 9.18 TOREX SEMICONDUCTOR

- 9.19 Vicor

- 9.20 Vishay Intertechnology, Inc.

电压调节器市场规模、份额和成长分析(按电压、应用、技术、类型、相数和地区划分)-2026-2033年产业预测

电压调节器市场规模、份额和成长分析(按电压、应用、技术、类型、相数和地区划分)-2026-2033年产业预测 汽车电压调节器市场规模、份额和成长分析(按类型、应用、分销管道和地区划分)—产业预测(2026-2033 年)

汽车电压调节器市场规模、份额和成长分析(按类型、应用、分销管道和地区划分)—产业预测(2026-2033 年) 步进电压调节器 - 全球市场份额和排名、总收入和需求预测(2025-2031年)

步进电压调节器 - 全球市场份额和排名、总收入和需求预测(2025-2031年) 电压稳压器市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、形式、材料类型、装置及最终用户

电压稳压器市场分析及预测(至2034年):类型、产品、服务、技术、组件、应用、形式、材料类型、装置及最终用户 三相住宅电压调节器市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、额定功率、地区和竞争细分,2020-2030 年)

三相住宅电压调节器市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、额定功率、地区和竞争细分,2020-2030 年) 空调市场按产品类型、机制、工作原理、材料类型、最终用途行业和分销管道划分 - 全球预测 2025-2030

空调市场按产品类型、机制、工作原理、材料类型、最终用途行业和分销管道划分 - 全球预测 2025-2030 全球住宅线性电压调节器市场全球线性商用电压调节器市场全球商用电压调节器市场三相电压调节器市场 - 全球产业规模、份额、趋势、机会与预测(细分、按类型、按安装类型、按相、按最终用户产业、按地区、按竞争,2020-2030 年预测)

全球住宅线性电压调节器市场全球线性商用电压调节器市场全球商用电压调节器市场三相电压调节器市场 - 全球产业规模、份额、趋势、机会与预测(细分、按类型、按安装类型、按相、按最终用户产业、按地区、按竞争,2020-2030 年预测)