|

市场调查报告书

商品编码

1699326

插入式商用电涌保护装置市场机会、成长动力、产业趋势分析及 2025-2034 年预测Plug-In Commercial Surge Protection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

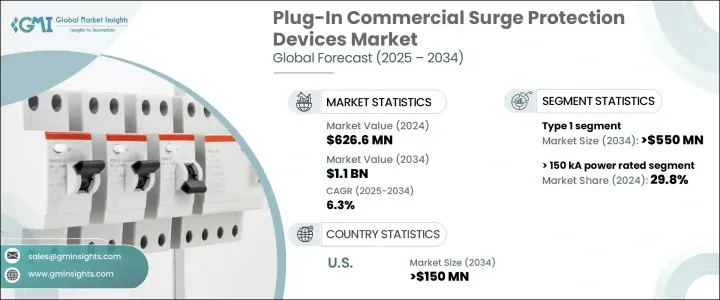

2024 年全球插入式商用电涌保护装置市值为 6.266 亿美元,预计 2025 年至 2034 年期间的复合年增长率将达到 6.3%,这得益于保护敏感电气系统免受电涌影响的需求不断增长。随着各行各业继续严重依赖自动化、云端运算和先进机械,对可靠的电涌保护解决方案的需求正在加速成长。各行业的企业都优先考虑电涌保护,以最大限度地减少停机时间、防止资料遗失并降低因电力波动造成的财务风险。商业设施中广泛采用先进的电子基础设施进一步加强了市场成长。

由于极端天气条件、电网故障以及高科技设备的日益普及,电力中断次数激增,使得电涌保护装置成为企业的重要投资。资料中心、医疗机构和工业设施正在越来越多地部署这些解决方案,以确保不间断运作。此外,强制进行电能品质管理的监管架构正在推动企业实施先进的保护机制。由于高度重视营运效率,各行各业都在采用尖端的浪涌保护技术,以提供更快的响应时间和增强的电压箝位能力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6.266亿美元 |

| 预测值 | 11亿美元 |

| 复合年增长率 | 6.3% |

1 型插入式商用电涌保护装置的需求正在稳步增长,预计到 2034 年该领域的需求将达到 5.5 亿美元。这种成长主要归因于对能够承受高压电涌并为关键系统提供强大安全性的综合保护解决方案的需求。越来越多的企业选择高性能电涌保护系统来满足不断发展的行业标准并保护宝贵资产免受不可预见的电气干扰。

依额定功率细分,市场涵盖以下类别:<= 50 kA、> 50 kA 至 100 kA、> 100 kA 至 150 kA 和 > 150 kA。 2024 年,额定功率 > 150 kA 的部分将占据 29.8% 的份额,这反映出用于保护重要基础设施的高浪涌电流额定係统的实施日益增多。受资料中心、医疗设施和 IT 中心对稳定电力环境需求不断增长的推动,<= 50 kA 细分市场的规模预计到 2034 年将达到 1.9 亿美元。雷击、雷暴和其他环境因素的频率不断增加,不断增加各产业对强大的突波保护解决方案的需求。

2024 年,美国插入式商用电涌保护装置市场规模达到 8,610 万美元,预计到 2034 年将达到 1.5 亿美元。随着各行各业对先进电气保护技术进行投资,对保护关键基础设施的需求不断增长,推动了美国市场的扩张。在电网现代化倡议和商业空间中敏感电子设备日益增多的推动下,到 2034 年,北美的成长率预计将超过 5.5%。资料中心、自动化製造工厂和医疗保健机构仍然是主要的最终用户,推动采用电涌保护系统来减轻与电压突波和功率波动相关的风险。

目录

第一章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依技术分类,2021 - 2034 年

- 主要趋势

- 类型 1

- 类型 2

- 类型 3

第六章:市场规模及预测:依功率等级,2021 - 2034 年

- 主要趋势

- ≤50千安

- > 50 kA 至 100 kA

- > 100 kA 至 150 kA

- > 150 千安

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 西班牙

- 荷兰

- 奥地利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 纽西兰

- 马来西亚

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 埃及

- 南非

- 奈及利亚

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 秘鲁

- 阿根廷

第八章:公司简介

- ABB

- Belkin

- Eaton

- Emerson Electric

- Havells India

- Hubbell

- Infineon Technologies

- JMV

- Legrand

- Leviton Manufacturing

- Maxivolt

- Phoenix Contact

- Schneider Electric

- Signify Holding

- Socomec

- Weidmuller Electronics India

- WenZhou Chuangjie Lightning Protection Electrical

- Wenzhou Wanlai Electric

The Global Plug-In Commercial Surge Protection Devices Market was valued at USD 626.6 million in 2024 and is projected to expand at a CAGR of 6.3% from 2025 to 2034, driven by the increasing need to safeguard sensitive electrical systems from power surges. As industries continue to rely heavily on automation, cloud computing, and advanced machinery, the demand for reliable surge protection solutions is accelerating. Businesses across various sectors are prioritizing surge protection to minimize downtime, prevent data loss, and reduce financial risks caused by electrical fluctuations. The widespread adoption of sophisticated electronic infrastructure in commercial facilities is further strengthening market growth.

The surge in power disruptions due to extreme weather conditions, grid failures, and the growing penetration of high-tech equipment has made surge protection devices a crucial investment for enterprises. Data centers, healthcare institutions, and industrial facilities are increasingly deploying these solutions to ensure uninterrupted operations. Additionally, regulatory frameworks mandating power quality management are pushing businesses to implement advanced protection mechanisms. With a strong emphasis on operational efficiency, industries are adopting cutting-edge surge protection technologies that offer faster response times and enhanced voltage clamping capabilities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $626.6 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.3% |

The demand for Type 1 plug-in commercial surge protection devices is experiencing steady growth, with projections estimating the segment to generate USD 550 million by 2034. This expansion is largely attributed to the need for comprehensive protection solutions that can withstand high-voltage surges and provide robust safety for critical systems. Businesses are increasingly opting for high-performance surge protection systems to meet evolving industry standards and protect valuable assets from unforeseen electrical disturbances.

Segmented by power ratings, the market encompasses categories including <= 50 kA, > 50 kA to 100 kA, > 100 kA to 150 kA, and > 150 kA. In 2024, the > 150 kA power-rated segment accounted for a 29.8% share, reflecting the rising implementation of high-surge current-rated systems designed to protect essential infrastructure. The <= 50 kA segment is projected to reach USD 190 million by 2034, fueled by increasing demand from data centers, healthcare facilities, and IT hubs requiring stable power environments. The growing frequency of lightning strikes, thunderstorms, and other environmental factors continues to amplify the need for robust surge protection solutions across industries.

The U.S. plug-in commercial surge protection devices market reached USD 86.1 million in 2024 and is expected to generate USD 150 million by 2034. The country's market expansion is fueled by the heightened demand for safeguarding critical infrastructure, with industries investing in advanced electrical protection technologies. North America is set to grow at a rate exceeding 5.5% through 2034, supported by power grid modernization initiatives and the increasing deployment of sensitive electronic equipment in commercial spaces. Data centers, automated manufacturing plants, and healthcare institutions remain key end-users, driving the adoption of surge protection systems to mitigate risks associated with voltage surges and power fluctuations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Type 1

- 5.3 Type 2

- 5.4 Type 3

Chapter 6 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 ≤ 50 kA

- 6.3 > 50 kA to 100 kA

- 6.4 > 100 kA to 150 kA

- 6.5 > 150 kA

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 Russia

- 7.3.4 UK

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Netherlands

- 7.3.8 Austria

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Australia

- 7.4.6 New Zealand

- 7.4.7 Malaysia

- 7.4.8 Indonesia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Egypt

- 7.5.5 South Africa

- 7.5.6 Nigeria

- 7.5.7 Kuwait

- 7.5.8 Oman

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Peru

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Belkin

- 8.3 Eaton

- 8.4 Emerson Electric

- 8.5 Havells India

- 8.6 Hubbell

- 8.7 Infineon Technologies

- 8.8 JMV

- 8.9 Legrand

- 8.10 Leviton Manufacturing

- 8.11 Maxivolt

- 8.12 Phoenix Contact

- 8.13 Schneider Electric

- 8.14 Signify Holding

- 8.15 Socomec

- 8.16 Weidmuller Electronics India

- 8.17 WenZhou Chuangjie Lightning Protection Electrical

- 8.18 Wenzhou Wanlai Electric

全球静电放电 (ESD) 防护装置市场规模、份额、趋势和成长分析报告(2026-2034 年)

全球静电放电 (ESD) 防护装置市场规模、份额、趋势和成长分析报告(2026-2034 年) 按元件类型、安装方式、电压范围、额定电流、最终用户和应用分類的PESD保护元件市场-2026-2032年全球预测

按元件类型、安装方式、电压范围、额定电流、最终用户和应用分類的PESD保护元件市场-2026-2032年全球预测 静电放电 (ESD) 保护二极体:全球市场份额和排名、总收入和需求预测(2025-2031 年)

静电放电 (ESD) 保护二极体:全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球静电放电 (ESD) 抑制二极体市场(至 2035 年):依产品类型、应用、封装类型、箝位电压/工作电压和额定功率划分

全球静电放电 (ESD) 抑制二极体市场(至 2035 年):依产品类型、应用、封装类型、箝位电压/工作电压和额定功率划分 全球暂态电压抑制器(TVS)闸流体市场全球瞬态电压抑制二极体市场

全球暂态电压抑制器(TVS)闸流体市场全球瞬态电压抑制二极体市场 2 型商用电涌保护装置市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

2 型商用电涌保护装置市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 暂态电压抑制二极体市场报告:趋势、预测和竞争分析(至 2031 年)线路商用电涌保护装置市场机会、成长动力、产业趋势分析与预测 2025 - 2034插入式住宅电涌保护装置市场机会、成长驱动因素、产业趋势分析与预测 2024 - 2032 年

暂态电压抑制二极体市场报告:趋势、预测和竞争分析(至 2031 年)线路商用电涌保护装置市场机会、成长动力、产业趋势分析与预测 2025 - 2034插入式住宅电涌保护装置市场机会、成长驱动因素、产业趋势分析与预测 2024 - 2032 年