|

市场调查报告书

商品编码

1699357

大肠直肠癌诊断市场机会、成长动力、产业趋势分析及预测(2025-2034)Colorectal Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

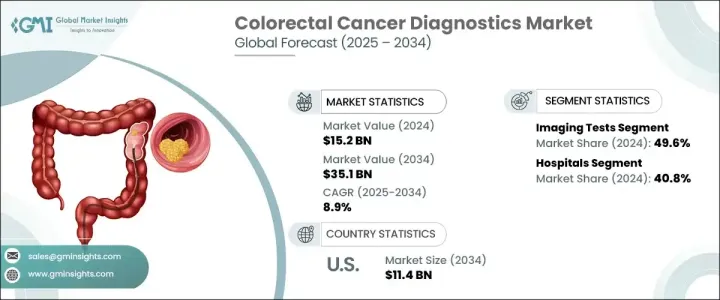

2024 年全球大肠直肠癌诊断市场价值为 152 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.9%。大肠直肠癌 (CRC) 是全球最常见的癌症之一,每年影响数百万人。随着 CRC 发病率的上升,尤其是在年轻人中,对准确、高效和早期诊断解决方案的需求从未如此迫切。早期发现可显着提高存活率,因此先进的诊断技术对于及时介入至关重要。

由于影像技术、液体活检和人工智慧诊断工具的不断进步,大肠直肠癌诊断市场正在迅速扩大。重点地区不断加强的宣传活动和政府支持的 CRC 筛检计划进一步推动了对可靠且易于获取的诊断方法的需求。领先的市场参与者正在积极投资开发适合临床环境和家庭筛检的高精度、非侵入性检测解决方案。粪便 DNA 检测、血液生物标记筛检和人工智慧影像解决方案的日益普及正在彻底改变 CRC 诊断,确保患者能够得到早期和准确的评估。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 152亿美元 |

| 预测值 | 351亿美元 |

| 复合年增长率 | 8.9% |

大肠直肠癌诊断市场按测试类型细分,包括血液检查、粪便测试、影像学检查、活检和其他诊断方法。由于对早期癌症检测和准确疾病评估的需求不断增长,影像学检查在 2024 年占据了 49.6% 的市场份额,占据主导地位。先进的影像技术,尤其是 PET-CT 扫描和 AI 辅助放射学,在早期发现大肠直肠恶性肿瘤方面发挥着至关重要的作用。这些高精度工具提高了诊断的准确性,促进了个人化的治疗方法。粪便隐血检测和 CRC DNA 筛检等粪便检测也因其非侵入性而越来越受到关注,使其成为大规模筛检计画的首选。

市场根据最终用途进一步分类,其中医院、诊断影像中心和癌症研究机构成为关键部分。 2024 年,医院占据了 40.8% 的市场份额,这主要归功于其先进的肿瘤科和胃肠科。完善的诊断设施、熟练的医疗专业人员以及综合的 CRC 筛检计画使医院成为领先的诊断机构。世界各国政府继续实施全国性的大肠癌筛检计划,进一步推动医院的诊断测试。

2024 年,美国大肠直肠癌诊断市场产值达到 50 亿美元,反映出对早期检测解决方案的强劲需求。年轻族群中 CRC 发生率的上升,加上人们对早期筛检重要性的认识不断提高,正在推动市场扩张。随着血液生物标记和粪便检测等家庭诊断解决方案的普及,CRC 筛检变得更加容易,人们可以采取主动措施进行早期发现。随着技术进步继续影响诊断领域,对高度准确、非侵入性和人工智慧驱动的结直肠癌筛检解决方案的需求预计将激增,巩固美国作为全球市场关键成长中心的地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 大肠直肠癌发生率和盛行率不断上升

- 与癌症筛检测试相关的政府措施和政策

- 癌症诊断领域的技术进步

- 早期诊断意识不断增强

- 产业陷阱与挑战

- 诊断测试和程序成本高昂

- 缺乏诊断测试的报销政策

- 成长动力

- 成长潜力分析

- 技术格局

- 监管格局

- 差距分析

- 专利分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按测试类型,2021 年至 2034 年

- 主要趋势

- 血液检查

- 粪便检查

- 粪便潜血试验(FOBT)

- 粪便生物标记检测

- CRC DNA筛检测试

- 影像学检查

- CT

- 超音波

- 磁振造影

- 宠物

- 大肠镜检查

- 其他影像学检查

- 活检

- 其他测试类型

第六章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 诊断影像中心

- 癌症研究中心

- 其他最终用途

第七章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Abbott Laboratories

- Becton, Dickinson and Company

- Danaher Corporation

- Exact Sciences Corporation

- F-Hoffmann-La Roche

- Fujirebio

- GE Healthcare

- Geneoscopy

- Guardant Health

- Hologic

- NeoGenomics Laboratories

- Qiagen

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fischer Scientific

The Global Colorectal Cancer Diagnostics Market was valued at USD 15.2 billion in 2024 and is projected to grow at a CAGR of 8.9% from 2025 to 2034. Colorectal cancer (CRC) is one of the most commonly diagnosed cancers worldwide, affecting millions of individuals each year. With CRC incidence rates rising, particularly among younger adults, the need for accurate, efficient, and early diagnostic solutions has never been more critical. Early detection significantly improves survival rates, making advanced diagnostic technologies essential for timely intervention.

The market for colorectal cancer diagnostics is expanding rapidly due to continuous advancements in imaging technologies, liquid biopsy, and AI-powered diagnostic tools. Increasing awareness campaigns and government-backed CRC screening programs across key regions are further driving demand for reliable and accessible diagnostic methods. Leading market players are actively investing in the development of high-precision, non-invasive testing solutions that cater to both clinical settings and at-home screening. The growing adoption of stool-based DNA tests, blood biomarker screenings, and AI-driven imaging solutions is revolutionizing CRC diagnostics, ensuring patients receive early and accurate assessments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.2 Billion |

| Forecast Value | $35.1 Billion |

| CAGR | 8.9% |

The colorectal cancer diagnostics market is segmented by test type, including blood tests, stool tests, imaging tests, biopsies, and other diagnostic methods. Imaging tests dominated the market with a 49.6% share in 2024, driven by the rising demand for early cancer detection and accurate disease assessment. Advanced imaging technologies, particularly PET-CT scans and AI-assisted radiology, play a crucial role in detecting colorectal malignancies at an early stage. These high-precision tools enhance diagnostic accuracy, facilitating personalized treatment approaches. Stool-based tests, including fecal occult blood tests and CRC DNA screenings, are also gaining traction due to their non-invasive nature, making them a preferred choice for large-scale screening programs.

The market is further categorized based on end use, with hospitals, diagnostic imaging centers, and cancer research institutions emerging as key segments. Hospitals accounted for 40.8% of the market share in 2024, primarily due to their advanced oncology and gastroenterology departments. The availability of comprehensive diagnostic facilities, skilled healthcare professionals, and integrated CRC screening programs has positioned hospitals as the leading diagnostic setting. Governments worldwide continue to implement nationwide colorectal cancer screening initiatives, further fueling hospital-based diagnostic testing.

The U.S. colorectal cancer diagnostics market generated USD 5 billion in 2024, reflecting a strong demand for early detection solutions. The rising incidence of CRC among younger populations, combined with growing awareness of the importance of early screening, is driving market expansion. The increased availability of at-home diagnostic solutions, such as blood biomarkers and stool-based tests, has made CRC screening more accessible, allowing individuals to take proactive steps toward early detection. As technological advancements continue to shape the diagnostic landscape, demand for highly accurate, non-invasive, and AI-powered colorectal cancer screening solutions is expected to surge, solidifying the U.S. as a key growth hub for the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence and prevalence of colorectal cancer

- 3.2.1.2 Government initiatives and policies associated with cancer screening tests

- 3.2.1.3 Technological advancements in field of cancer diagnostics

- 3.2.1.4 Growing awareness regarding early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diagnostic tests and procedures

- 3.2.2.2 Lack of reimbursement policies for diagnostic tests

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.5 Regulatory landscape

- 3.6 Gap analysis

- 3.7 Patent analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood tests

- 5.3 Stool tests

- 5.3.1 Fecal occult blood test (FOBT)

- 5.3.2 Fecal biomarker test

- 5.3.3 CRC DNA screening test

- 5.4 Imaging tests

- 5.4.1 CT

- 5.4.2 Ultrasound

- 5.4.3 MRI

- 5.4.4 PET

- 5.4.5 Colonoscopy

- 5.4.6 Other imaging tests

- 5.5 Biopsy

- 5.6 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic imaging centers

- 6.4 Cancer research centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Becton, Dickinson and Company

- 8.3 Danaher Corporation

- 8.4 Exact Sciences Corporation

- 8.5 F-Hoffmann-La Roche

- 8.6 Fujirebio

- 8.7 GE Healthcare

- 8.8 Geneoscopy

- 8.9 Guardant Health

- 8.10 Hologic

- 8.11 NeoGenomics Laboratories

- 8.12 Qiagen

- 8.13 Siemens Healthineers

- 8.14 Sysmex Corporation

- 8.15 Thermo Fischer Scientific

转移性大肠直肠癌市场(按药物类别和地区)分析与预测(2025-2035)

转移性大肠直肠癌市场(按药物类别和地区)分析与预测(2025-2035) 大肠癌筛检和诊断市场—全球产业规模、份额、趋势、机会和预测(按筛检、诊断、最终用户、地区和竞争细分,2020-2030 年)

大肠癌筛检和诊断市场—全球产业规模、份额、趋势、机会和预测(按筛检、诊断、最终用户、地区和竞争细分,2020-2030 年) 大肠直肠癌筛检和诊断市场(按类型、产品、应用和最终用户划分)—2025 年至 2030 年全球预测转移性大肠直肠癌药物市场-全球产业规模、份额、趋势、机会及预测(按药物类别、配销通路、地区和竞争情况划分,2020-2030 年预测)

大肠直肠癌筛检和诊断市场(按类型、产品、应用和最终用户划分)—2025 年至 2030 年全球预测转移性大肠直肠癌药物市场-全球产业规模、份额、趋势、机会及预测(按药物类别、配销通路、地区和竞争情况划分,2020-2030 年预测) 大肠癌筛检与诊断:全球市场

大肠癌筛检与诊断:全球市场 微卫星稳定大肠直肠癌市场,按阶段、给药途径、产品、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测大肠直肠癌药物市场:按药物类别、治疗类型、给药途径、分销管道划分 - 全球预测 2025-2030

微卫星稳定大肠直肠癌市场,按阶段、给药途径、产品、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测大肠直肠癌药物市场:按药物类别、治疗类型、给药途径、分销管道划分 - 全球预测 2025-2030 大肠癌症 - KOL的见解

大肠癌症 - KOL的见解 大肠直肠癌治疗药物市场规模、份额、成长分析、按药物类别、按癌症类型、按分销管道、按地区 - 行业预测,2024-2031 年

大肠直肠癌治疗药物市场规模、份额、成长分析、按药物类别、按癌症类型、按分销管道、按地区 - 行业预测,2024-2031 年 大肠直肠癌治疗市场规模 - 按治疗(免疫疗法、化疗)、癌症类型(大肠直肠腺癌、胃肠道类癌)、治疗提供者(医院、专科诊所)和预测,2024 - 2032 年

大肠直肠癌治疗市场规模 - 按治疗(免疫疗法、化疗)、癌症类型(大肠直肠腺癌、胃肠道类癌)、治疗提供者(医院、专科诊所)和预测,2024 - 2032 年