|

市场调查报告书

商品编码

1699433

网路遥测市场机会、成长动力、产业趋势分析及 2025-2034 年预测Network Telemetry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

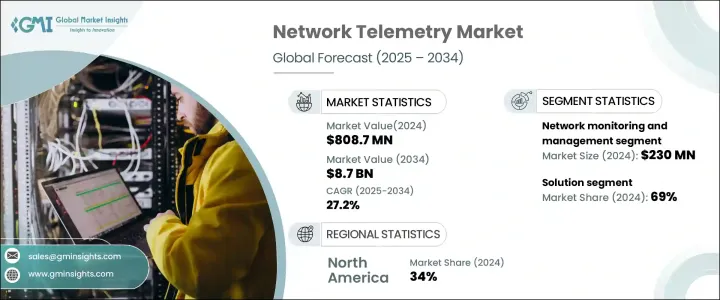

2024 年全球网路遥测市场价值为 8.087 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 27.2%。推动这一成长的关键因素是全球 5G 网路的快速扩张,增加了对先进网路监控解决方案的需求。随着 5G 提供更低的延迟和增强的频宽,企业正在采用即时网路遥测解决方案来优化效能、监控拥塞并提高讯号品质。此外,对数位化营运和基于云端的服务的依赖日益增加,促使企业实施网路遥测,以主动检测和缓解问题。

随着各行各业对高速连线的需求不断增长,网路遥测对于维护网路健康和可靠性变得至关重要。物联网设备和云端运算的日益普及进一步加强了对自动监控系统的需求。随着网路复杂性的增加,公司正在从传统的监控方法转向遥测驱动的解决方案,以提高安全性、效率和数据驱动的决策。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 8.087亿美元 |

| 预测值 | 87亿美元 |

| 复合年增长率 | 27.2% |

在应用方面,市场包括网路监控和管理、网路安全监控、流量分析、故障排除和根本原因分析。 2024年,网路监控和管理将占据超过29%的市场份额,创造约2.3亿美元的收入。业务营运对网路服务的日益依赖推动了对持续效能评估、减少停机时间和确保无缝连接的需求。自动监控工具可提供网路拥塞、安全漏洞和效能波动的即时警报,使企业能够保持营运稳定。

组件部分由解决方案和服务组成,其中解决方案在 2024 年占据主导地位,占据约 69% 的市场份额。各组织正在将人工智慧分析整合到网路管理工具中,以增强监控能力。这些解决方案有助于即时资料收集、分析和视觉化,解决现代网路挑战。随着云端服务、物联网设备和 5G 技术的日益普及,企业正在投资一体化遥测解决方案,以简化部署并简化网路最佳化。

根据企业规模,市场分为中小型企业 (SME) 和大型企业,大型企业在 2024 年将处于领先地位。由于业务范围广泛且网路基础设施复杂,大型公司需要先进的遥测工具来管理效能、正常运作时间和安全性。这些企业产生大量资料,需要高频宽应用程式和强大的网路监控系统来防止中断。安全问题、合规性要求以及停机的财务影响进一步推动了遥测解决方案的大规模采用。

从部署角度来看,市场分为本地部署和云端解决方案,其中云端解决方案在 2024 年将占据相当大的份额。云端平台提供可扩展性,使企业能够有效地管理不断增长的资料流量,并将遥测解决方案与现有的云端环境整合。基于云端的遥测解决方案还提供经济高效的基于订阅的模型,减少前期投资,同时确保长期节省。云端平台的灵活性使其成为寻求强大、即时监控功能且无需额外基础设施负担的企业的理想选择。

从地区来看,北美占据网路遥测市场的主导地位,占超过 34% 的份额,其中美国在 2024 年的市场规模约为 1.426 亿美元,位居第一。各行业的快速数字化转型、云端服务的采用率不断提高以及对安全网路管理的推动正在加速市场成长。政府加强 5G 基础设施和电信的措施进一步推动了对网路遥测解决方案的需求,确保了各行业的网路安全、高效能运作。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 网路遥测解决方案供应商

- 服务提供者

- 网路安全供应商

- 系统整合商

- 最终用途

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 即时网路监控需求

- 采用云端和虚拟化网络

- 5G部署不断增加

- 网路优化和效能管理的需求

- 产业陷阱与挑战

- 实施和维护成本高

- 与现有基础设施整合的复杂性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 解决方案

- 服务

- 专业服务

- 託管服务

第六章:市场估计与预测:按部署,2021 - 2034 年

- 主要趋势

- 本地部署

- 云

第七章:市场估计与预测:依企业规模,2021 - 2034 年

- 主要趋势

- 大型企业

- 中小企业

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 网路监控与管理

- 网路安全监控

- 交通分析与工程

- 故障排除和根本原因分析

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Anuta Networks International

- Apcela

- Arista

- Broadcom

- Check Point Software

- Cisco

- ExtraHop Networks

- F5 Networks

- Fortinet

- Gigamon

- Juniper

- Kentik

- Keysight Technologies

- Marvell Technology Group

- Mellanox Technologies

- NetAcquire

- Riverbed Technology

- VOLANSYS Technologies

- Waystream

The Global Network Telemetry Market was valued at USD 808.7 million in 2024 and is projected to expand at a CAGR of 27.2% from 2025 to 2034. A key factor driving this growth is the rapid expansion of 5G networks worldwide, increasing the need for advanced network monitoring solutions. With 5G offering reduced latency and enhanced bandwidth, businesses are adopting real-time network telemetry solutions to optimize performance, monitor congestion, and improve signal quality. Additionally, rising dependence on digital operations and cloud-based services is pushing enterprises to implement network telemetry for proactive issue detection and mitigation.

As demand for high-speed connectivity grows across industries, network telemetry is becoming essential for maintaining network health and reliability. The rising adoption of IoT devices and cloud computing is further strengthening the need for automated monitoring systems. With network complexities increasing, companies are shifting from traditional monitoring methods to telemetry-driven solutions for improved security, efficiency, and data-driven decision-making.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $808.7 Million |

| Forecast Value | $8.7 Billion |

| CAGR | 27.2% |

In terms of application, the market includes network monitoring & management, network security monitoring, traffic analysis, troubleshooting, and root cause analysis. In 2024, network monitoring and management accounted for over 29% of the market, generating approximately USD 230 million. Growing reliance on network services for business operations is fueling demand for continuous performance assessment, reducing downtime, and ensuring seamless connectivity. Automated monitoring tools provide real-time alerts on network congestion, security breaches, and performance fluctuations, allowing businesses to maintain operational stability.

The component segment consists of solutions and services, with solutions dominating in 2024, holding around 69% of the market. Organizations are integrating AI-powered analytics into network management tools to enhance monitoring capabilities. These solutions facilitate real-time data collection, analysis, and visualization, addressing modern networking challenges. With the increasing adoption of cloud services, IoT devices, and 5G technology, enterprises are investing in all-in-one telemetry solutions that simplify deployment and streamline network optimization.

By enterprise size, the market is categorized into small and medium enterprises (SMEs) and large enterprises, with large enterprises leading in 2024. Due to their expansive operations and complex network infrastructures, large companies require advanced telemetry tools to manage performance, uptime, and security. These enterprises generate vast amounts of data, necessitating high-bandwidth applications and robust network monitoring systems to prevent disruptions. Security concerns, compliance requirements, and financial implications of downtime further drive large-scale adoption of telemetry solutions.

Deployment-wise, the market is divided into on-premise and cloud solutions, with the cloud segment holding a significant share in 2024. Cloud platforms offer scalability, allowing businesses to efficiently manage growing data traffic and integrate telemetry solutions with existing cloud environments. Cloud-based telemetry solutions also offer cost-effective, subscription-based models, reducing upfront investment while ensuring long-term savings. The flexibility of cloud platforms makes them ideal for enterprises seeking robust, real-time monitoring capabilities without additional infrastructure burdens.

Regionally, North America dominated the network telemetry market, capturing over 34% of the share, with the US leading at approximately USD 142.6 million in 2024. Rapid digital transformation across sectors, increased adoption of cloud services, and the push for secure network management are accelerating market growth. Government initiatives to enhance 5G infrastructure and strengthen telecommunications are further fueling demand for network telemetry solutions, ensuring secure and high-performance network operations across industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Network telemetry solution providers

- 3.2.2 Service providers

- 3.2.3 Network security providers

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Demand for real-time network monitoring

- 3.8.1.2 Adoption of cloud and virtualized networks

- 3.8.1.3 Rising 5G rollout

- 3.8.1.4 Need for network optimization and performance management

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High implementation and maintenance costs

- 3.8.2.2 Complexity of integration with existing infrastructure

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Service

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premise

- 6.3 Cloud

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Large enterprises

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Network monitoring & management

- 8.3 Network security monitoring

- 8.4 Traffic analysis and engineering

- 8.5 Troubleshooting and root cause analysis

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Anuta Networks International

- 10.2 Apcela

- 10.3 Arista

- 10.4 Broadcom

- 10.5 Check Point Software

- 10.6 Cisco

- 10.7 ExtraHop Networks

- 10.8 F5 Networks

- 10.9 Fortinet

- 10.10 Gigamon

- 10.11 Juniper

- 10.12 Kentik

- 10.13 Keysight Technologies

- 10.14 Marvell Technology Group

- 10.15 Mellanox Technologies

- 10.16 NetAcquire

- 10.17 Riverbed Technology

- 10.18 VOLANSYS Technologies

- 10.19 Waystream

网路遥测市场:按组件、部署类型、组织规模、最终用户和应用程式划分-2026年至2032年全球市场预测

网路遥测市场:按组件、部署类型、组织规模、最终用户和应用程式划分-2026年至2032年全球市场预测 2026年全球网路遥测市场报告

2026年全球网路遥测市场报告 网路遥测市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

网路遥测市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 网路遥测市场规模、份额和成长分析(按组件、部署模式、企业规模、应用和地区划分)—2026-2033年产业预测

网路遥测市场规模、份额和成长分析(按组件、部署模式、企业规模、应用和地区划分)—2026-2033年产业预测 网路遥测市场-全球产业规模、份额、趋势、机会和预测(按组件、组织规模、最终用户、地区和竞争格局划分,2020-2030 年预测)

网路遥测市场-全球产业规模、份额、趋势、机会和预测(按组件、组织规模、最终用户、地区和竞争格局划分,2020-2030 年预测) 网路遥测市场成长、规模和趋势分析 - 按组件、部署、公司规模和应用 - 区域展望、竞争策略和细分预测(至 2034 年)

网路遥测市场成长、规模和趋势分析 - 按组件、部署、公司规模和应用 - 区域展望、竞争策略和细分预测(至 2034 年) 网路遥测市场报告:2030 年趋势、预测与竞争分析

网路遥测市场报告:2030 年趋势、预测与竞争分析