|

市场调查报告书

商品编码

1708153

商用车 ADAS 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Commercial Vehicle ADAS Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

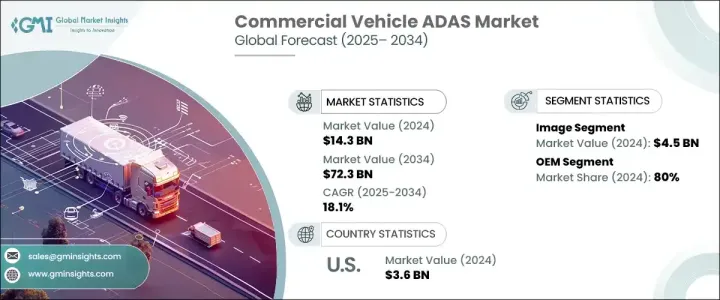

2024 年全球商用车 ADAS 市值为 143 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 18.1%。随着全球安全法规的收紧,促使商业车队营运商采用先进驾驶辅助系统(ADAS),市场正在显着扩张。随着人们对道路安全、事故预防和法规遵循的关注日益增加,北美、欧洲和亚洲部分地区对 ADAS 解决方案的需求激增。各国政府正在实施严格的政策,强制采用监控驾驶员疲劳、分心和车道维持的整合系统,进一步加速 ADAS 的采用。这些技术对于减少人为错误造成的事故至关重要,特别是在长途货运和城市商业运输。此外,人工智慧驱动的 ADAS 功能的不断整合提高了安全性和营运效率,使其成为现代商用车的重要组成部分。

市场根据感测器类型进行分类,包括雷达、光达、超音波、影像和其他感测器。其中,影像感测器领域占据30%的份额,2024年创造了45亿美元的市场规模。影像感测器对于基于视觉的ADAS功能(例如车道偏离警告、交通标誌识别和碰撞侦测)至关重要。这些感测器透过即时视讯捕捉和处理发挥作用,帮助商业驾驶员安全应对复杂的交通状况。随着自动化和机器学习能力的进步,商用车 ADAS 对高解析度影像感测器的依赖日益增加,从而提高了车辆的反应能力和事故预防能力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 143亿美元 |

| 预测值 | 723亿美元 |

| 复合年增长率 | 18.1% |

根据分销管道,商用车 ADAS 市场细分为OEM (原始设备製造商)和售后市场解决方案。 2024 年, OEM领域占据主导地位,占有 80% 的市场。原始设备製造商 (OEM) 在製造过程中将 ADAS 技术直接整合到车辆中,确保基本安全功能是标准配置或作为选用配备。由于车队所有者优先考虑可靠性、效率和对监管要求的遵守,对工厂安装的安全系统的日益偏好正在推动OEM占据主导地位。这种内建集成为商用车配备尖端 ADAS 技术提供了一种无缝且高效的方法。

北美以 35% 的份额领先商用车 ADAS 市场,光是美国在 2024 年的市场价值就达到 36 亿美元。美国拥有庞大的商用车队,包括长途卡车、送货货车和公共交通车辆,这导致对 ADAS 解决方案的需求很高。安全性改进、营运效率的提高和燃料消耗的降低是推动美国采用 ADAS 技术的主要因素,车队营运商正在大力投资这些系统,以提高道路安全性、降低保险成本并提高整体驾驶表现。随着技术的不断发展,在监管支援、技术进步和不断增强的安全意识的推动下,商用车 ADAS 市场有望持续成长。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 零件供应商

- 技术提供者

- 製造商

- 经销商

- 最终用途

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 成本分析

- 衝击力

- 成长动力

- 加强道路安全法规

- 自动驾驶技术进步

- 改进车队管理

- 车辆安全的需求不断成长

- 产业陷阱与挑战

- 旧车改装复杂度高

- ADAS技术的初始成本高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按系统,2021 - 2034 年

- 主要趋势

- 自适应巡航控制

- 盲点侦测

- 车道偏离预警系统

- 自动紧急煞车(AEM)

- 前方碰撞警告

- 夜视系统

- 驾驶员监控

- 轮胎压力监测系统

- 抬头显示器

- 停车辅助系统

- 其他的

第六章:市场估计与预测:按感测器,2021 - 2034 年

- 主要趋势

- 雷达

- 光达

- 超音波

- 影像

- 其他的

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 轻型商用车

- 丙型肝炎病毒

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Applied Intuition

- Autoliv

- Bosch

- Continental

- Daimler

- Ford

- Gauzy

- Harman

- HL Mando

- Imagination Technologies

- Kenworth Trucks

- KUS Americas

- MAN

- Masstrans

- Scania

- Starkenn

- Valeo

- Vignal Group

- Volvo

- ZF Friedrichshafen

The Global Commercial Vehicle ADAS Market was valued at USD 14.3 billion in 2024 and is projected to grow at a CAGR of 18.1% between 2025 and 2034. The market is witnessing significant expansion as safety regulations tighten worldwide, prompting commercial fleet operators to adopt advanced driver assistance systems (ADAS). With increasing concerns over road safety, accident prevention, and regulatory compliance, the demand for ADAS solutions is surging across North America, Europe, and parts of Asia. Governments are implementing stringent policies to mandate integrated systems that monitor driver fatigue, distraction, and lane-keeping, further accelerating ADAS adoption. These technologies are proving essential in reducing accidents caused by human error, particularly in long-haul trucking and urban commercial transport. Additionally, the rising integration of AI-driven ADAS features enhances safety and operational efficiency, making them a vital component in modern commercial vehicles.

The market is categorized based on sensor types, including radar, LiDAR, ultrasonic, image, and other sensors. Among these, the image sensor segment accounted for a 30% share and generated USD 4.5 billion in 2024. Image sensors are critical in vision-based ADAS features such as lane departure warnings, traffic sign recognition, and collision detection. These sensors function through real-time video capturing and processing, helping commercial drivers navigate complex traffic conditions safely. As automation and machine learning capabilities advance, the reliance on high-resolution image sensors in commercial vehicle ADAS is increasing, improving vehicle responsiveness and accident prevention.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.3 Billion |

| Forecast Value | $72.3 Billion |

| CAGR | 18.1% |

Based on distribution channels, the commercial vehicle ADAS market is segmented into OEM (original equipment manufacturer) and aftermarket solutions. In 2024, the OEM segment dominated with an 80% market share. OEMs integrate ADAS technologies directly into vehicles during manufacturing, ensuring that essential safety features are either standard or available as optional equipment. The increasing preference for factory-fitted safety systems is driving OEM dominance as fleet owners prioritize reliability, efficiency, and compliance with regulatory mandates. This built-in integration offers a seamless and efficient approach to equipping commercial vehicles with cutting-edge ADAS technologies.

North America led the commercial vehicle ADAS market with a 35% share, and the U.S. alone was valued at USD 3.6 billion in 2024. The United States has a vast commercial vehicle fleet, including long-haul trucks, delivery vans, and public transport vehicles, contributing to the high demand for ADAS solutions. Safety improvements, enhanced operational efficiency, and fuel consumption reduction are primary factors driving the adoption of ADAS technologies in the U.S. Fleet operators are investing heavily in these systems to enhance road safety, lower insurance costs, and improve overall driver performance. As technology continues to evolve, the commercial vehicle ADAS market is poised for continued growth, driven by regulatory support, technological advancements, and increasing safety awareness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Technology providers

- 3.2.3 Manufacturers

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Cost analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing road safety regulations

- 3.9.1.2 Technological advancements in autonomous driving

- 3.9.1.3 Improved vehicle fleet management

- 3.9.1.4 Rising demand for vehicle safety

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High complexity in retrofitting older vehicles

- 3.9.2.2 High initial cost of ADAS technologies

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By System, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Adaptive cruise control

- 5.3 Blind spot detection

- 5.4 Lane departure warning system

- 5.5 Automatic emergency braking (AEM)

- 5.6 Forward collision warning

- 5.7 Night vision system

- 5.8 Driver monitoring

- 5.9 Tire pressure monitoring system

- 5.10 Head-up display

- 5.11 Park assist system

- 5.12 Others

Chapter 6 Market Estimates & Forecast, By Sensor, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Radar

- 6.3 Lidar

- 6.4 Ultrasonic

- 6.5 Image

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 LCV

- 7.3 HCV

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Applied Intuition

- 10.2 Autoliv

- 10.3 Bosch

- 10.4 Continental

- 10.5 Daimler

- 10.6 Ford

- 10.7 Gauzy

- 10.8 Harman

- 10.9 HL Mando

- 10.10 Imagination Technologies

- 10.11 Kenworth Trucks

- 10.12 KUS Americas

- 10.13 MAN

- 10.14 Masstrans

- 10.15 Scania

- 10.16 Starkenn

- 10.17 Valeo

- 10.18 Vignal Group

- 10.19 Volvo

- 10.20 ZF Friedrichshafen

商用车ADAS市场:按ADAS功能、自动化程度、感测器类型、车辆类型、最终用户和应用划分 - 全球预测(2025-2032年)

商用车ADAS市场:按ADAS功能、自动化程度、感测器类型、车辆类型、最终用户和应用划分 - 全球预测(2025-2032年) 全球商用车ADAS市场

全球商用车ADAS市场 商用车 ADAS 市场,全球 2025-2029

商用车 ADAS 市场,全球 2025-2029