|

市场调查报告书

商品编码

1708181

免疫毒素市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Immunotoxins Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

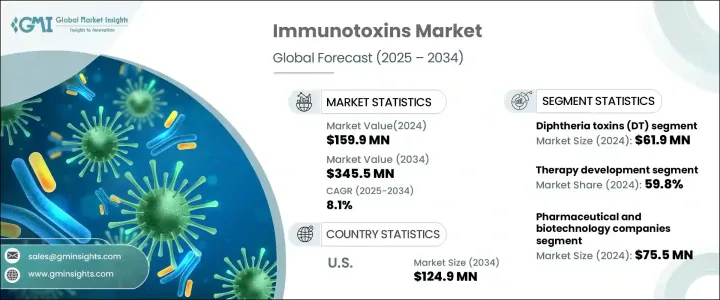

2024 年全球免疫毒素市场规模达到 1.599 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.1%。免疫毒素是将单株抗体或标靶分子与强效毒素结合的治疗剂。它们的机制涉及将抗体与目标细胞(例如癌细胞或病变细胞)表面的抗原结合。然后毒素成分透过破坏重要的细胞过程来杀死目标细胞。针对慢性病的标靶治疗的日益普及是市场成长的主要驱动力。标靶疗法,包括免疫毒素,专门攻击致病细胞,减少不良反应并改善患者的治疗效果。这些益处推动了基于免疫毒素的治疗在癌症和慢性病管理中的应用增加,从而促进了市场扩张。

市场根据毒素类型分为白喉毒素 (DT)、炭疽毒素、假单胞菌外毒素 (PE)、核醣体失活蛋白免疫毒素和其他免疫毒素。白喉毒素 (DT) 部分在 2024 年的价值为 6,190 万美元,预计在预测期内的复合年增长率为 8.1%。这种增长归因于白喉毒素强大的治疗潜力,其透过抑制目标细胞中的蛋白质合成,导致细胞死亡。 Denileukin diftitox 是一种将白喉毒素与 IL-2 受体靶向片段结合在一起的融合蛋白,它体现了强化 DT 片段生长的杀细胞作用。正在进行的研究和监管部门的批准,特别是基于白喉毒素的免疫毒素的研究和监管部门的批准,进一步促进了这一领域的扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.599亿美元 |

| 预测值 | 3.455亿美元 |

| 复合年增长率 | 8.1% |

根据应用,市场分为生物医学研究和治疗开发。治疗开发领域在 2024 年占据 59.8% 的市场份额,占据市场主导地位。其主导地位是由于癌症盛行率的上升以及临床环境中免疫毒素的使用增加。白血病、淋巴瘤和多发性骨髓瘤等血液系统恶性肿瘤发生率的不断上升,推动了对免疫毒素疗法的需求,进一步推动了市场成长。

根据最终用途,市场分为製药和生物技术公司、CRO 和 CMO、学术和研究机构以及其他最终用户。 2024 年,製药和生物技术公司以 7,550 万美元的市场规模占据该领域的主导地位。这些公司在研发方面投入了大量资金,以创造针对癌症和慢性疾病的先进免疫毒素疗法,并专注于针对患病细胞同时保护健康细胞。他们与 CRO、CMO 和学术机构的合作加速了产品商业化和开发,为市场成长做出了重大贡献。

预计美国免疫毒素市场将大幅成长,到 2034 年将达到 1.249 亿美元。癌症盛行率的上升和死亡率的上升推动了对基于免疫毒素的标靶治疗的需求,从而进一步增强了该国的市场地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 癌症和慢性病发生率上升

- 扩大对新型免疫毒素疗法的监管批准

- 越来越关注标靶治疗

- 产业陷阱与挑战

- 免疫毒素研发中与细胞毒性和製造相关的挑战

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按毒素类型,2021 年至 2034 年

- 主要趋势

- 白喉毒素(DT)

- 炭疽毒素

- 假单胞菌外毒素(PE)

- 核醣体灭活蛋白类免疫毒素

- 其他毒素类型

第六章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 生物医学研究

- 治疗发展

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 製药和生物技术公司

- CRO 和 CMO

- 学术和研究机构

- 其他最终用途

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Abcam

- Bio-Techne

- Cayman Chemical

- Creative Biolabs

- Enzo Biochem

- List Biological Labs

- Merck KGaA

- Quadratech Diagnostics

- Santa Cruz Biotechnology

- The Native Antigen Company

- Thermo Fisher Scientific

The Global Immunotoxins Market reached USD 159.9 million in 2024 and is expected to grow at a CAGR of 8.1% from 2025 to 2034. Immunotoxins are therapeutic agents that combine a monoclonal antibody or a targeting molecule with a potent toxin. Their mechanism involves binding the antibody to antigens present on the surface of target cells, such as cancerous or diseased cells. The toxin component then kills the targeted cells by disrupting essential cellular processes. The increasing adoption of targeted therapies for chronic conditions is a major driver of market growth. Targeted therapies, including immunotoxins, specifically attack disease-causing cells, reducing adverse reactions and improving patient outcomes. These benefits are driving the increased use of immunotoxin-based treatments in cancer and chronic disease management, fueling market expansion.

The market is segmented by toxin type into diphtheria toxins (DT), anthrax-based toxins, pseudomonas exotoxins (PE), ribosome-inactivating protein-based immunotoxins, and other immunotoxins. The diphtheria toxins (DT) segment accounted for USD 61.9 million in 2024 and is expected to grow at a CAGR of 8.1% during the forecast period. This growth is attributed to the strong therapeutic potential of diphtheria toxins, which work by inhibiting protein synthesis in targeted cells, leading to cell death. Denileukin diftitox, a fusion protein that combines diphtheria toxin with an IL-2 receptor-targeting fragment, exemplifies the cytocidal action that reinforces the growth of the DT segment. Ongoing research and regulatory approvals, particularly for diphtheria toxin-based immunotoxins, further contribute to the expansion of this segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $159.9 Million |

| Forecast Value | $345.5 Million |

| CAGR | 8.1% |

By application, the market is categorized into biomedical research and therapy development. The therapy development segment led the market with a 59.8% share in 2024. Its dominance is driven by the increasing prevalence of cancer and the rising use of immunotoxins in clinical settings. The growing incidence of hematological malignancies such as leukemia, lymphoma, and multiple myeloma is boosting the demand for immunotoxin-based therapies, further propelling market growth.

Based on end use, the market is divided into pharmaceutical and biotechnology companies, CROs and CMOs, academic and research institutes, and other end users. Pharmaceutical and biotechnology companies dominated the segment with USD 75.5 million in 2024. These companies invest extensively in research and development to create advanced immunotoxin therapies for cancer and chronic diseases, focusing on targeting diseased cells while preserving healthy ones. Their collaborations with CROs, CMOs, and academic institutions accelerate product commercialization and development, contributing significantly to market growth.

The U.S. immunotoxins market is expected to witness substantial growth, reaching USD 124.9 million by 2034. The increasing prevalence of cancer and rising mortality rates are driving demand for targeted immunotoxin-based therapies, further strengthening the country's market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of cancer and chronic diseases

- 3.2.1.2 Expanding regulatory approvals for new immunotoxin therapies

- 3.2.1.3 Growing focus on targeted therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Challenges related to cytotoxicity and manufacturing in the development of immunotoxins

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Toxin Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Diphtheria toxins (DT)

- 5.3 Anthrax based toxins

- 5.4 Pseudomonas exotoxins (PE)

- 5.5 Ribosomes inactivating protein based immunotoxins

- 5.6 Other toxin types

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Biomedical research

- 6.3 Therapy development

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical and biotechnology companies

- 7.3 CROs and CMOs

- 7.4 Academic and research institutes

- 7.5 Other End Use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abcam

- 9.2 Bio-Techne

- 9.3 Cayman Chemical

- 9.4 Creative Biolabs

- 9.5 Enzo Biochem

- 9.6 List Biological Labs

- 9.7 Merck KGaA

- 9.8 Quadratech Diagnostics

- 9.9 Santa Cruz Biotechnology

- 9.10 The Native Antigen Company

- 9.11 Thermo Fisher Scientific