|

市场调查报告书

商品编码

1708186

金属化阻隔膜包装市场机会、成长动力、产业趋势分析及2025-2034年预测Metalized Barrier Film Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

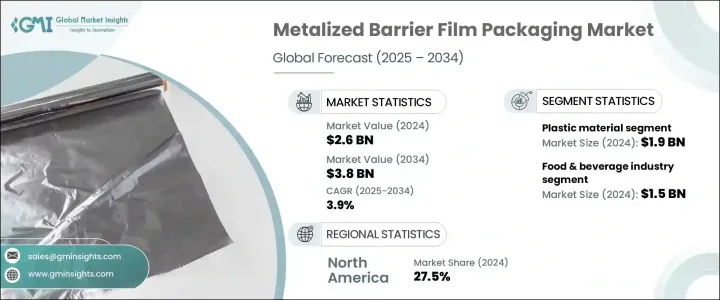

2024 年全球金属化阻隔膜包装市场价值为 26 亿美元,预估 2025 年至 2034 年的复合年增长率为 3.9%。这一成长主要受製药业需求成长和各行业对延长保质期的需求不断增长的推动。金属化阻隔膜可有效抵抗环境因素,维持包装食品的新鲜度、风味和营养品质。随着全球化和消费者对包装和加工食品的偏好不断增加,製造商开始使用这些薄膜来确保产品在延长的运输时间内的完整性。製药业尤其受益于泡罩包装和医用袋中的这些薄膜,确保敏感药物的保护。专注于高门槛解决方案和遵守监管标准的製造商将会看到该领域的采用率不断提高。

对更长保质期的需求是推动市场扩张的另一个重要因素。这些薄膜可以有效地保护包装食品、药品和化妆品,防止变质并长期维持品质。随着消费者生活节奏越来越快,他们越来越倾向于即食食品和加工食品,推动了对先进包装解决方案的需求。此外,电子商务和全球贸易的兴起也增加了对坚固的阻隔膜的需求,以便在运输和储存过程中保护产品。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 26亿美元 |

| 预测值 | 38亿美元 |

| 复合年增长率 | 3.9% |

市场按材料细分,其中塑胶占据主导地位,到 2024 年市场规模将达到 19 亿美元。塑胶基金属化薄膜因其重量轻、成本效益高和灵活性而受到青睐。随着消费者越来越多地选择便携、便捷的包装,柔性塑胶薄膜越来越受到青睐。它们能够减少对防腐剂的需求,同时保持产品新鲜度,使其成为大量应用的理想选择。即食食品和饮料的日益普及进一步支持了这一趋势,这些食品和饮料需要优质的包装来保持其品质。

按终端用途产业划分,食品和饮料产业是最大的贡献者,2024 年的估值为 15 亿美元。该行业的成长归因于快速的城市化和消费者习惯的改变,消费者更青睐包装和即食产品。金属化阻隔膜广泛应用于零食、咖啡、乳製品和其他包装食品,无需依赖化学防腐剂即可保持新鲜、防止变质。监管部门对永续包装的日益重视以及消费者对环保解决方案的需求进一步推动了这一领域的采用。

受高阻隔包装需求不断增长和电子商务行业快速增长的推动,北美将在 2024 年占据全球 27.5% 的市场份额。政府对采用永续包装材料的支持,加上消费者偏好的变化,正在推动金属化阻隔膜包装的采用。美国引领区域市场,2024 年市场规模达 5.239 亿美元,这得益于对包装食品日益增长的需求,这些食品需要高性能包装来维持产品在运输过程中的完整性。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 延长保存期限的需求不断增长

- 可持续阻隔涂层的进展

- 蓬勃发展的电子商务和食品配送服务

- 快速的城市化和忙碌的生活方式

- 药品包装需求不断成长

- 产业陷阱与挑战

- 有限的回收和永续性问题

- 来自可生物降解替代品的竞争

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按材料,2021 年至 2034 年

- 主要趋势

- 塑胶

- 聚丙烯(PP)

- 聚对苯二甲酸乙二酯(PET)

- 聚酰胺(PA)

- 聚乙烯(PE)

- 尼龙

- 其他的

- 金属

第六章:市场估计与预测:依最终用途产业,2021 年至 2034 年

- 主要趋势

- 食品和饮料

- 製药

- 电子产品

- 个人护理和化妆品

- 其他的

第七章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第八章:公司简介

- Aerolam Group

- Amcor

- Cosmo Films

- Dunmore

- Ester Industries

- Finfoil

- Flex Films

- Jindal Films

- Kolon Industries

- Nahar PolyFilms

- PC Laminations

- SRF

- Sumilon Group

- Taghleef Industries

- Toray

- Zhejiang Changyu New Materials

The Global Metalized Barrier Film Packaging Market, valued at USD 2.6 billion in 2024, is expected to grow at a CAGR of 3.9% from 2025 to 2034. This growth is primarily driven by rising demand from the pharmaceutical industry and the increasing need for extended shelf life across various sectors. Metalized barrier films provide high protection against environmental factors, preserving the freshness, flavor, and nutritional quality of packaged goods. As globalization and consumer preferences for packaged and processed foods increase, manufacturers are turning to these films to ensure product integrity during extended transit times. The pharmaceutical sector, in particular, benefits from these films in blister packs and medical pouches, ensuring the protection of sensitive drugs. Manufacturers focusing on high-barrier solutions and adherence to regulatory standards will see increased adoption in this sector.

The need for longer shelf life is another significant factor fueling market expansion. These films effectively safeguard packaged foods, pharmaceuticals, and cosmetics, preventing spoilage and maintaining quality over time. As consumer lifestyles become more fast-paced, there is a greater inclination toward ready-to-eat and processed food products, driving demand for advanced packaging solutions. In addition, the rise in e-commerce and global trade has heightened the need for robust barrier films to protect products during transportation and storage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 3.9% |

The market is segmented by material, with plastic dominating this space, accounting for USD 1.9 billion in 2024. Plastic-based metalized films are preferred due to their lightweight nature, cost-efficiency, and flexibility. As consumers increasingly opt for portable and convenient packaging, flexible plastic films gain traction. Their ability to reduce the need for preservatives while maintaining product freshness makes them ideal for high-volume applications. This trend is further supported by the growing popularity of ready-to-eat foods and beverages, which require superior packaging to retain their quality.

By end-use industry, the food and beverage segment is the largest contributor, with a valuation of USD 1.5 billion in 2024. The segment's growth is attributed to rapid urbanization and changing consumer habits, which favor packaged and ready-to-eat products. Metalized barrier films are widely used in snacks, coffee, dairy, and other packaged foods, preserving freshness and preventing spoilage without relying on chemical preservatives. Increasing regulatory emphasis on sustainable packaging and consumer demand for eco-friendly solutions further boost adoption in this segment.

North America held 27.5% of the global market share in 2024, driven by the rising need for high-barrier packaging and the rapid growth of the e-commerce sector. Government support for adopting sustainable packaging materials, combined with changing consumer preferences, is promoting the adoption of metalized barrier film packaging. The United States led the regional market, accounting for USD 523.9 million in 2024, fueled by the growing demand for packaged foods that require high-performance packaging to maintain product integrity during transportation.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for extended shelf life

- 3.2.1.2 Advancements in sustainable barrier coatings

- 3.2.1.3 Booming e-commerce & food delivery services

- 3.2.1.4 Rapid urbanization and busy lifestyles

- 3.2.1.5 Growing demand in pharmaceutical packaging

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited recycling & sustainability issues

- 3.2.2.2 Competition from biodegradable alternatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Polypropylene (PP)

- 5.2.2 Polyethylene Terephthalate (PET)

- 5.2.3 Polyamide (PA)

- 5.2.4 Polyethylene (PE)

- 5.2.5 Nylon

- 5.2.6 Others

- 5.3 Metals

Chapter 6 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Food & beverage

- 6.3 Pharmaceuticals

- 6.4 Electronics

- 6.5 Personal care and cosmetics

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Aerolam Group

- 8.2 Amcor

- 8.3 Cosmo Films

- 8.4 Dunmore

- 8.5 Ester Industries

- 8.6 Finfoil

- 8.7 Flex Films

- 8.8 Jindal Films

- 8.9 Kolon Industries

- 8.10 Nahar PolyFilms

- 8.11 PC Laminations

- 8.12 SRF

- 8.13 Sumilon Group

- 8.14 Taghleef Industries

- 8.15 Toray

- 8.16 Zhejiang Changyu New Materials

2026年全球金属化薄膜市场报告

2026年全球金属化薄膜市场报告 金属化薄膜市场:依应用、薄膜类型、厚度、涂层和金属化技术划分-2025-2032年全球预测

金属化薄膜市场:依应用、薄膜类型、厚度、涂层和金属化技术划分-2025-2032年全球预测 金属化薄膜市场-全球产业规模、份额、趋势、机会及预测,依金属、材料(聚丙烯、聚对苯二甲酸乙二酯等)、最终用途、地区及竞争情形细分,2020-2030 年预测

金属化薄膜市场-全球产业规模、份额、趋势、机会及预测,依金属、材料(聚丙烯、聚对苯二甲酸乙二酯等)、最终用途、地区及竞争情形细分,2020-2030 年预测 金属化薄膜市场规模、份额、趋势分析报告:按金属、材料、最终用途、地区、细分市场预测,2025-2030 年

金属化薄膜市场规模、份额、趋势分析报告:按金属、材料、最终用途、地区、细分市场预测,2025-2030 年 2024 年至 2031 年金属化薄膜市场(按材料、金属、最终用户产业和地区划分)

2024 年至 2031 年金属化薄膜市场(按材料、金属、最终用户产业和地区划分) 金属化聚酯薄膜市场报告:2030 年趋势、预测与竞争分析

金属化聚酯薄膜市场报告:2030 年趋势、预测与竞争分析 金属化薄膜市场:成长,未来展望,竞争分析,2024~2032年

金属化薄膜市场:成长,未来展望,竞争分析,2024~2032年