|

市场调查报告书

商品编码

1716538

新鲜无花果市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Fresh Figs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

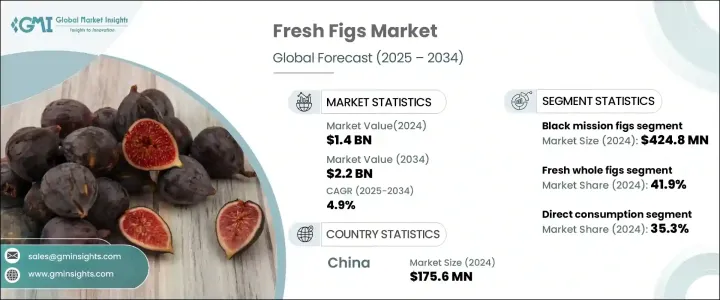

2024 年全球新鲜无花果市场价值为 14 亿美元,预计 2025 年至 2034 年期间将以 4.9% 的复合年增长率稳步增长。需求的增长归因于新鲜无花果提供的众多健康益处,包括其丰富的纤维含量,有助于消化并有助于控制体重。每 100 克新鲜无花果含有每日建议纤维摄取量的 14%,以及支持整体健康的必需维生素。研究表明,经常食用新鲜无花果可以降低血压和胆固醇水平,增加了其作为健康饮食选择的吸引力。提供有机、从农场到家庭农产品的线上杂货平台的日益普及也促进了新鲜无花果市场的发展,扩大了消费者获取这些营养丰富的水果的管道。此外,它们在各种烹饪应用中的多功能性(从糕点到美味佳餚)进一步增加了需求。新鲜无花果因其有助于控製糖尿病和心臟病的能力而受到特别重视,使其成为注重增强免疫健康的消费者的热门选择。

根据产品类型,新鲜无花果市场分为黑色使命无花果、棕色火鸡无花果、卡多塔无花果、卡利米尔纳无花果、亚得里亚海无花果等。黑无花果市场表现突出,2024 年产值达 4.248 亿美元,复合年增长率高达 5.9%。这些无花果以其甜美的口感和较长的保质期而闻名,成为国内和出口市场的首选。此外,它们在主要无花果种植区的广泛种植保证了稳定的供应,满足了人们对天然甜味剂和更健康食品选择日益增长的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14亿美元 |

| 预测值 | 22亿美元 |

| 复合年增长率 | 4.9% |

市场也按形式划分,新鲜无花果部分在 2024 年将占据 41.9% 的显着份额。越来越多的消费者选择新鲜无花果作为精製糖的更健康替代品。无花果可用于各种菜餚,从沙拉、甜点到美食,因此很受欢迎。与干无花果相比,新鲜无花果具有加工程度最低的额外优势,因此对于注重健康的消费者来说,新鲜无花果是一种更具吸引力的选择。

就最终用途而言,直接消费在 2024 年占据了最大的市场份额,为 35.3%。新鲜无花果以其天然形式广受喜爱,无论去皮与否,并被加入到各种食品中,如果酱、蛋糕和酱汁。它们的营养成分丰富,富含纤维、抗氧化剂和钾、镁等矿物质,促使人们越来越意识到它们的健康益处。随着植物性饮食和超级食品趋势的兴起,对新鲜无花果的需求预计将持续上升。

在中国,新鲜无花果市场在 2024 年的产值达到 1.756 亿美元,预计到 2034 年将达到 3.333 亿美元,复合年增长率为 4.8%。儘管有气候和交通方面的挑战,消费者对新鲜无花果的兴趣日益浓厚,推动着市场成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 提高消费者对健康益处的认知

- 网路杂货和有机食品市场的扩张

- 功能性和药用食品的需求不断增长

- 产业陷阱与挑战

- 保存期限短和易腐烂问题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依产品类型,2021 年至 2034 年

- 主要趋势

- 黑色使命无花果

- 棕色火鸡无花果

- 角田无花果

- 卡利米尔纳无花果

- 亚得里亚海无花果

- 其他的

第六章:市场估计与预测:依形式,2021 年至 2034 年

- 主要趋势

- 新鲜无花果

- 无花果干

- 无花果酱/无花果泥

- 无花果酱/果冻

- 无花果糖浆

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 直接消费

- 烘焙和糖果

- 乳製品

- 零食和谷物

- 饮料

- 冰沙

- 果汁

- 烹饪应用

- 其他的

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 超市和大卖场

- 专卖店

- 线上零售商

- 餐饮服务提供者

- 其他的

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Alara Agri Business

- Athos Agricola

- California Figs

- Earl's Organic Produce

- FruitLips Jiaherb

- Hadley Fruit Orchards

- Mafpack

- Meurens Natural

- Roland Foods

- Valley Fig Growers

The Global Fresh Figs Market was valued at USD 1.4 billion in 2024 and is projected to grow at a steady CAGR of 4.9% from 2025 to 2034. The rise in demand is attributed to the numerous health benefits fresh figs offer, including their rich fiber content, which aids digestion and helps with weight management. Each 100-gram serving of fresh figs contains 14% of the recommended daily fiber intake, along with essential vitamins that support overall wellness. Studies have shown that regular consumption of fresh figs can lower blood pressure and cholesterol levels, adding to their appeal as a healthy dietary option. The market for fresh figs is also bolstered by the growing popularity of online grocery platforms that offer organic, farm-to-home produce, expanding consumer access to these nutrient-rich fruits. Additionally, their versatility in various culinary applications-from pastries to savory dishes-further increases demand. Fresh figs are particularly valued for their ability to help manage diabetes and heart conditions, making them a sought-after option for consumers focused on boosting their immune health.

By product type, the fresh figs market is segmented into black mission figs, brown turkey figs, Kadota figs, Calimyrna figs, Adriatic figs, and others. The black mission figs segment has been a standout performer, generating USD 424.8 million in 2024, with a robust CAGR of 5.9%. These figs are known for their sweet taste and superior shelf life, making them a preferred choice in both domestic and export markets. Furthermore, their widespread cultivation in key fig-growing regions supports a consistent supply, aligning with the increasing demand for natural sweeteners and healthier food options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 4.9% |

The market is also divided by form, with the fresh whole figs segment accounting for a significant share of 41.9% in 2024. Consumers are increasingly turning to fresh whole figs as a healthier alternative to refined sugar. These figs are consumed in a variety of dishes, from salads and desserts to gourmet meals, driving their popularity. Fresh figs offer the added benefit of being minimally processed compared to dried figs, making them a more attractive option for health-conscious consumers.

Regarding end-use, direct consumption held the largest market share at 35.3% in 2024. Fresh figs are widely enjoyed in their natural form, whether peeled or unpeeled, and incorporated into various food products such as jams, cakes, and sauces. Their nutrient profile, rich in fiber, antioxidants, and minerals like potassium and magnesium, has contributed to the growing awareness of their health benefits. With the rise of plant-based diets and the superfood trend, the demand for fresh figs is expected to continue to rise.

In China, the fresh figs market generated USD 175.6 million in 2024 and is projected to reach USD 333.3 million by 2034, growing at a CAGR of 4.8%. Despite challenges related to climate and transportation, the increasing consumer interest in fresh figs is driving market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing consumer awareness of health benefits

- 3.6.1.2 Expansion of online grocery and organic food markets

- 3.6.1.3 Rising demand in functional and medicinal foods

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Short shelf life and perishability issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Black mission figs

- 5.3 Brown turkey figs

- 5.4 Kadota figs

- 5.5 Calimyrna figs

- 5.6 Adriatic figs

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Form, 2021 – 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Fresh whole figs

- 6.3 Dried figs

- 6.4 Fig paste/puree

- 6.5 Fig jam/jelly

- 6.6 Fig syrup

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Direct consumption

- 7.3 Bakery and confectionery

- 7.4 Dairy products

- 7.5 Snacks and cereals

- 7.6 Beverages

- 7.6.1 Smoothies

- 7.6.2 Juices

- 7.7 Culinary applications

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores

- 8.4 Online retailers

- 8.5 Foodservice providers

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alara Agri Business

- 10.2 Athos Agricola

- 10.3 California Figs

- 10.4 Earl's Organic Produce

- 10.5 FruitLips Jiaherb

- 10.6 Hadley Fruit Orchards

- 10.7 Mafpack

- 10.8 Meurens Natural

- 10.9 Roland Foods

- 10.10 Valley Fig Growers

全球新鲜无花果市场规模、份额、趋势和成长分析报告(2026-2034年)

全球新鲜无花果市场规模、份额、趋势和成长分析报告(2026-2034年) 新鲜无花果市场成长、规模和趋势分析(按产品类型、形态和最终用户划分)-区域展望、竞争策略和细分市场预测(至2034年)

新鲜无花果市场成长、规模和趋势分析(按产品类型、形态和最终用户划分)-区域展望、竞争策略和细分市场预测(至2034年) 新鲜无花果世界市场

新鲜无花果世界市场