|

市场调查报告书

商品编码

1716592

视讯对讲设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Video Intercom Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

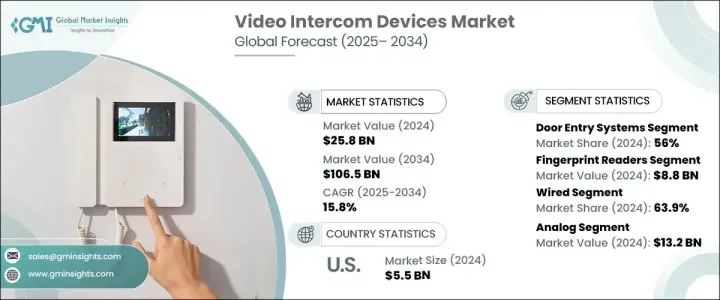

2024 年全球视讯对讲设备市场价值为 258 亿美元,预计 2025 年至 2034 年的复合年增长率为 15.8%。市场快速成长的动力来自于对先进家庭安全系统日益增长的需求以及无线通讯技术的不断创新。消费者对安全的关注度不断提高,对智慧家庭安全解决方案的需求也越来越高。可支配收入的增加和家庭安全研发投资的增加进一步推动了全球对这些系统的应用。人工智慧与智慧家庭技术的结合,使得系统更有效率、安全、使用者友好,增强了可视对讲设备的吸引力。随着基于云端和无线的安全系统日益普及,消费者正在从传统解决方案转向采用透过行动装置提供即时通知和远端控制的系统。随着城市人口迁移的加速以及双收入家庭对远端监控系统的追求,对智慧安全解决方案的需求持续上升。

市场根据设备类型分为手持设备、门禁系统和视讯婴儿监视器。受住宅和商业建筑对高级安全功能需求不断增长的推动,门禁系统领域在 2024 年占据了全球视讯对讲设备市场的 56%。物联网和基于人工智慧的存取控制系统的整合透过实现用户身份验证、远端管理和持续监控增强了安全性。人们越来越关注智慧安全解决方案以应对日益严重的安全威胁,这推动了门禁系统的采用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 258亿美元 |

| 预测值 | 1065亿美元 |

| 复合年增长率 | 15.8% |

根据存取控制,市场分为指纹读取器、密码存取、感应卡和无线存取。 2024 年指纹辨识器市场价值为 88 亿美元,反映出人们对生物辨识安全系统的偏好日益增加。随着住宅、商业和工业环境中的安全问题日益严重,业主们纷纷选择基于生物辨识的控制系统,因为它们可靠、易用,并且能够防止未经授权的存取。指纹辨识器提供非接触式、快速且安全的身份验证,降低凭证被盗或滥用的风险。人工智慧与指纹识别、基于云端的存取和行动身份验证的整合进一步增强了这些系统的安全性和便利性。

根据系统类型,市场分为有线和无线。 2024 年,有线市场占据了 63.9% 的市场份额,因为高安全性环境青睐有线解决方案,因为它们可靠且具有抵御网路威胁的能力。政府设施、军事基地和关键基础设施站点需要最高程度的安全,与无线方案相比,有线系统可以更好地防止资料外洩和系统中断。

技术部分分为模拟系统和基于 IP 的系统。由于类比技术在低频宽环境的可靠性,其市场规模到 2024 年将达到 132 亿美元。与依赖互联网连接的基于 IP 的系统不同,模拟系统独立运行,因此非常适合宽频普及率有限的老建筑和农村地区。

根据最终用途,市场分为汽车、商业、政府、住宅和其他。受智慧办公室和共享办公空间对自动门禁控制需求不断增长的推动,商业领域将在 2024 年以 93 亿美元的规模引领市场。基于物联网的办公环境的日益普及推动了对非接触式进入、访客记录以及透过视讯对讲系统提高安全性的需求。 2024 年,美国市场规模达 55 亿美元,对整合物联网、人工智慧和基于云端的监控系统以提高住宅安全性的复杂家庭安全解决方案的需求不断增长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 家庭安全系统需求不断成长

- 无线通讯技术的进步

- 智慧家庭普及率不断上升

- 都市化和住宅小区不断扩大

- 与物联网和自动化集成

- 产业陷阱与挑战

- 初始安装和维护成本高

- 隐私和资料安全问题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依设备类型,2021-2034

- 主要趋势

- 门禁系统

- 手持装置

- 视讯婴儿监视器

第六章:市场估计与预测:按存取控制,2021-2034

- 主要趋势

- 指纹辨识器

- 密码访问

- 感应卡

- 无线存取

第七章:市场估计与预测:按系统,2021-2034

- 主要趋势

- 有线

- 无线的

第八章:市场估计与预测:依技术,2021-2034 年

- 主要趋势

- 模拟

- 基于IP

第九章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 汽车

- 商业的

- 政府

- 住宅

- 其他的

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- ABB Ltd

- Aiphone

- Axis Communications AB

- ButterflyMX Inc.

- Comelit Group

- Commend International GmbH

- Dahua Technologies Co. Ltd

- Doorbird

- Fermax

- Godrej & Boyce Mfg. Co. Ltd.

- Hangzhou Hikvision Digital Technology Co. Ltd

- Honeywell

- KOCOM Co., Ltd.

- Legrand

- Mivanta

- MOX Group Limited

- Panasonic Holdings Corporation

- Ring

- Siedle & Sohne OHG

- Xiamen Leelen Technology Co., Ltd

- Zicom

- ZKTeco

The Global Video Intercom Devices Market was valued at USD 25.8 billion in 2024 and is anticipated to grow at a CAGR of 15.8% from 2025 to 2034. The rapid growth of the market is driven by the increasing demand for advanced home security systems and rising innovations in wireless communication technology. Consumers are more concerned about safety, leading to a higher demand for smart home security solutions. Rising disposable income and growing investments in research and development for home security have further fueled the adoption of these systems globally. The integration of AI with smart home technologies has enabled more efficient, secure, and user-friendly systems, enhancing the appeal of video intercom devices. With the increasing popularity of cloud-based and wireless security systems, consumers are shifting away from conventional solutions to adopt systems that offer real-time notifications and remote control through mobile devices. As urban migration accelerates and dual-income families seek remote surveillance systems, demand for intelligent security solutions continues to rise.

The market is segmented by device type into handheld devices, door entry systems, and video baby monitors. The door entry systems segment captured 56% of the global video intercom devices market in 2024, driven by the increasing need for advanced security features in residential and commercial buildings. Integration of IoT and AI-based access control systems has enhanced security by enabling user identity verification, remote management, and continuous surveillance. The growing focus on smart security solutions to address rising security threats is boosting the adoption of door entry systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $25.8 Billion |

| Forecast Value | $106.5 Billion |

| CAGR | 15.8% |

By access control, the market is divided into fingerprint readers, password access, proximity cards, and wireless access. The fingerprint readers segment was valued at USD 8.8 billion in 2024, reflecting the increasing preference for biometric security systems. As security concerns grow in residential, commercial, and industrial settings, property owners are opting for biometric-based control systems due to their reliability, ease of use, and ability to prevent unauthorized access. Fingerprint readers offer contactless, fast, and secure authentication, reducing the risk of credential theft or misuse. The integration of AI with fingerprint recognition, cloud-based access, and mobile authentication further enhances the security and convenience of these systems.

The market is bifurcated by system type into wired and wireless. The wired segment held 63.9% of the market share in 2024, as high-security environments favor wired solutions due to their reliability and resilience against cyber threats. Government facilities, military bases, and critical infrastructure sites require maximum security, and wired systems offer better protection against data breaches and system disruptions compared to wireless alternatives.

The technology segment is divided into analog and IP-based systems. The analog segment accounted for USD 13.2 billion in 2024 due to its reliability in low-bandwidth environments. Unlike IP-based systems that rely on internet connectivity, analog systems operate independently, making them ideal for older buildings and rural areas where broadband penetration is limited.

By end use, the market is segmented into automotive, commercial, government, residential, and others. The commercial segment led the market with USD 9.3 billion in 2024, driven by the rising demand for automated access control in smart offices and co-working spaces. Increased adoption of IoT-based office environments has fueled the need for contactless entry, visitor logging, and improved security through video intercom systems. In 2024, the US market accounted for USD 5.5 billion, with growing demand for sophisticated home security solutions that integrate IoT, AI, and cloud-based monitoring systems to improve residential security.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand for home security systems

- 3.6.1.2 Advancements in wireless communication technology

- 3.6.1.3 Rising adoption in smart homes

- 3.6.1.4 Growing urbanization and residential complexes

- 3.6.1.5 Integration with IoT and automation

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial installation and maintenance costs

- 3.6.2.2 Privacy and data security concerns

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Device Type, 2021-2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Door entry systems

- 5.3 Handheld devices

- 5.4 Video baby monitors

Chapter 6 Market Estimates & Forecast, By Access control, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Fingerprint readers

- 6.3 Password access

- 6.4 Proximity cards

- 6.5 Wireless access

Chapter 7 Market Estimates & Forecast, By System, 2021-2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Wired

- 7.3 Wireless

Chapter 8 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Analog

- 8.3 IP-based

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 Automotive

- 9.3 Commercial

- 9.4 Government

- 9.5 Residential

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB Ltd

- 11.2 Aiphone

- 11.3 Axis Communications AB

- 11.4 ButterflyMX Inc.

- 11.5 Comelit Group

- 11.6 Commend International GmbH

- 11.7 Dahua Technologies Co. Ltd

- 11.8 Doorbird

- 11.9 Fermax

- 11.10 Godrej & Boyce Mfg. Co. Ltd.

- 11.11 Hangzhou Hikvision Digital Technology Co. Ltd

- 11.12 Honeywell

- 11.13 KOCOM Co., Ltd.

- 11.14 Legrand

- 11.15 Mivanta

- 11.16 MOX Group Limited

- 11.17 Panasonic Holdings Corporation

- 11.18 Ring

- 11.19 Siedle & Sohne OHG

- 11.20 Xiamen Leelen Technology Co., Ltd

- 11.21 Zicom

- 11.22 ZKTeco