|

市场调查报告书

商品编码

1716612

钢筋市场机会、成长动力、产业趋势分析及2025-2034年预测Steel Rebar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

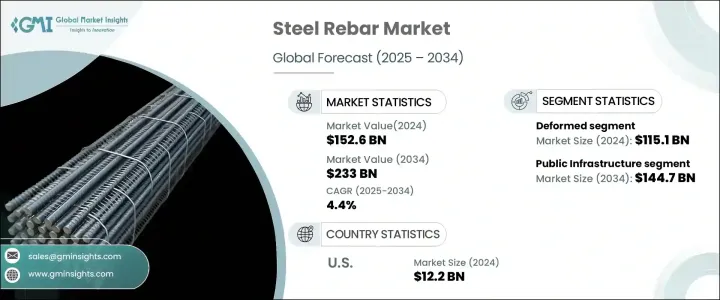

2024 年全球钢筋市场规模达 1,526 亿美元,预估 2025 年至 2034 年的复合年增长率为 4.4%。这一成长主要得益于基础建设的大量投资,尤其是在新兴经济体。随着各国不断实现交通系统的现代化、城市地区的扩张和公共设施的加强,对钢筋等可靠、高强度材料的需求持续激增。钢筋对于加固混凝土结构以及提高其强度、稳定性和寿命至关重要。快速的城市化和人口增长导致住宅和商业领域的建筑活动增加,进一步刺激了对钢筋的需求。此外,政府旨在升级老化基础设施和建造永续建筑的措施也为製造商创造了丰厚的机会。钢铁製造技术的进步以及改善与混凝土黏合的创新钢筋设计的引入也促进了市场的成长,从而能够建造耐用且有弹性的结构。

钢筋市场主要分为两类:异型钢筋和低碳钢筋。螺纹钢筋因其独特的表面纹理和优异的粘合性能而闻名,2024 年其市场价值为 1151 亿美元,预计到 2034 年复合年增长率将达到 4.4%。其对混凝土的增强黏合性可最大限度地减少滑移,并显着提高结构稳定性,使其成为高应力应用的首选。这一领域的主导地位归因于其在梁、柱和地基等钢筋混凝土结构建造中的广泛应用。随着高层建筑、桥樑、工业设施等大型基础设施项目的不断扩大,对螺纹钢的需求仍然强劲。此外,人们对永续建筑实践的日益重视以及对抗震结构的需求进一步扩大了螺纹钢筋的使用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1526亿美元 |

| 预测值 | 2330亿美元 |

| 复合年增长率 | 4.4% |

从应用角度来看,公共基础设施领域在2024年占据了61.6%的市场。许多国家正在向交通网络、机场和桥樑等大型基础设施项目投入资金,这些项目都需要大量钢筋进行结构加强。这些项目旨在创建能够承受环境压力并确保公共安全的持久耐用的基础设施。对基础设施现代化的高度重视,加上政府支持的措施和资金,正在推动公共基础设施项目对高品质钢筋的需求。随着全球经济体大力投资扩大城市景观和改善公共设施,对钢筋加强关键结构的依赖持续成长。

2024 年美国钢筋市场价值为 122 亿美元,预计受道路、桥樑和公共交通系统等基本基础设施建设和维护支出增加的推动,该市场将稳步增长。政府旨在振兴国家基础设施的倡议,加上对建筑材料的投资增加,正在推动美国对钢筋的需求。市场参与者正致力于增强产品供应,以满足大型公共工程和私人建筑项目所需的严格品质标准,确保现代基础设施的弹性和寿命。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 技术概述

- 监管格局

- 衝击力

- 成长动力

- 建筑业和房地产开发业蓬勃发展

- 增加房屋装修和改造

- 注重能源效率

- 都市化进程加快,可支配所得增加

- 产业陷阱与挑战

- 原物料成本和价格波动

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按产品,2021-2034

- 主要趋势

- 变形

- 轻微

第六章:市场估计与预测:依工艺,2021-2034

- 主要趋势

- 碱性氧气炼钢

- 电弧炉

第七章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 住宅建筑

- 公共基础设施

- 工业的

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Acerinox SA

- ArcelorMittal

- Commercial Metals Company

- Daido Steel Co Ltd

- Gerdau S/A

- HBIS Group

- Jiangsu Shagang Group

- JSW

- NIPPON STEEL CORPORATION

- NLMK

- Nucor

- POSCO HOLDINGS INC.

- SAIL

- Steel Dynamics, Inc

- Tata Steel

The Global Steel Rebar Market reached USD 152.6 billion in 2024 and is projected to grow at a CAGR of 4.4% from 2025 to 2034. This growth is primarily driven by substantial investments in infrastructure development, particularly across emerging economies. As countries continue to modernize their transportation systems, expand urban areas, and enhance public utilities, the demand for reliable, high-strength materials such as steel rebar continues to surge. Steel rebar is essential for reinforcing concrete structures and improving their strength, stability, and longevity. Rapid urbanization and population growth have led to increased construction activities in both residential and commercial sectors, further boosting the demand for steel rebar. Moreover, government initiatives aimed at upgrading aging infrastructure and constructing sustainable buildings are creating lucrative opportunities for manufacturers. Technological advancements in steel manufacturing and the introduction of innovative rebar designs that improve bonding with concrete have also contributed to the market's growth, enabling the construction of durable and resilient structures.

The steel rebar market is segmented into two primary categories: deformed and mild steel rebar. Deformed steel rebar, known for its superior bonding properties due to its distinct surface patterns, generated USD 115.1 billion in 2024 and is projected to grow at a CAGR of 4.4% through 2034. Its enhanced adhesion to concrete minimizes slippage and significantly improves structural stability, making it the preferred choice in high-stress applications. This segment's dominance is attributed to its extensive use in the construction of reinforced concrete structures such as beams, columns, and foundations. As large-scale infrastructure projects, including high-rise buildings, bridges, and industrial facilities, continue to expand, the demand for deformed steel rebar remains robust. Additionally, the growing emphasis on sustainable construction practices and the need for earthquake-resistant structures are further amplifying the use of deformed steel rebar.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $152.6 Billion |

| Forecast Value | $233 Billion |

| CAGR | 4.4% |

In terms of application, the public infrastructure segment accounted for a 61.6% share of the market in 2024. Numerous countries are channeling investments into large-scale infrastructure projects such as transportation networks, airports, and bridges, all of which require significant quantities of steel rebar for structural reinforcement. These projects aim to create long-lasting, durable infrastructure that can withstand environmental stress and ensure public safety. The strong focus on infrastructure modernization, coupled with government-backed initiatives and funding, is fueling the demand for high-quality steel rebar in public infrastructure projects. As global economies invest heavily in expanding their urban landscapes and improving public utilities, the reliance on steel rebar to fortify critical structures continues to grow.

The U.S. steel rebar market was valued at USD 12.2 billion in 2024, with projections indicating steady growth driven by increased spending on the construction and maintenance of essential infrastructure, including roads, bridges, and public transportation systems. Government initiatives aimed at revitalizing the nation's infrastructure, combined with increased investments in building materials, are propelling the demand for steel rebar in the U.S. Market players are focusing on enhancing product offerings to meet the stringent quality standards required for large-scale public works and private construction projects, ensuring the resilience and longevity of modern infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technological overview

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising construction and real estate development

- 3.6.1.2 Increasing home renovation and remodeling

- 3.6.1.3 Focus on energy efficiency

- 3.6.1.4 Rising urbanization and rising disposable income

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Raw material costs and price volatility

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Million) (Million Tones)

- 5.1 Key trends

- 5.2 Deformed

- 5.3 Mild

Chapter 6 Market Estimates & Forecast, By Process, 2021-2034 (USD Million) (Million Tones)

- 6.1 Key trends

- 6.2 Basic oxygen steelmaking

- 6.3 Electric arc furnace

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Million Tones)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.3 Public infrastructure

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Million Tones)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Acerinox S.A

- 9.2 ArcelorMittal

- 9.3 Commercial Metals Company

- 9.4 Daido Steel Co Ltd

- 9.5 Gerdau S/A

- 9.6 HBIS Group

- 9.7 Jiangsu Shagang Group

- 9.8 JSW

- 9.9 NIPPON STEEL CORPORATION

- 9.10 NLMK

- 9.11 Nucor

- 9.12 POSCO HOLDINGS INC.

- 9.13 SAIL

- 9.14 Steel Dynamics, Inc

- 9.15 Tata Steel

2026年全球钢筋市场报告

2026年全球钢筋市场报告 特种不锈钢棒材市场:依产品类型、製造流程、等级、应用和通路划分,全球预测(2026-2032年)轧延钢棒材及型材市场:依产品、材质等级、最终用途及通路划分-2026-2032年全球预测

特种不锈钢棒材市场:依产品类型、製造流程、等级、应用和通路划分,全球预测(2026-2032年)轧延钢棒材及型材市场:依产品、材质等级、最终用途及通路划分-2026-2032年全球预测 日本钢筋市场规模、份额、趋势及预测(依产品类型、製程、表面处理类型、最终用途及地区划分,2026-2034年)

日本钢筋市场规模、份额、趋势及预测(依产品类型、製程、表面处理类型、最终用途及地区划分,2026-2034年) 钢筋市场规模、份额及成长分析(按最终用户、类型、涂层和地区划分)-产业预测(2026-2033)热机械处理钢筋市场(按等级、尺寸范围、最终用户和分销管道)—2025-2032 年全球预测

钢筋市场规模、份额及成长分析(按最终用户、类型、涂层和地区划分)-产业预测(2026-2033)热机械处理钢筋市场(按等级、尺寸范围、最终用户和分销管道)—2025-2032 年全球预测 钢筋市场:按类型、涂层类型、应用和地区划分钢筋市场按产品类型、材料、製程类型、钢筋尺寸、应用和最终用途产业划分-2025-2030 年全球预测

钢筋市场:按类型、涂层类型、应用和地区划分钢筋市场按产品类型、材料、製程类型、钢筋尺寸、应用和最终用途产业划分-2025-2030 年全球预测 TMT钢筋市场-全球产业规模、份额、趋势、机会及预测(依等级、直径、应用、地区及竞争细分,2020-2030年)2025-2033年钢筋市场报告,依产品类型(变形钢筋、低碳钢筋)、製程(碱性氧气炼钢、电弧炉)、精加工类型(环氧、涂装、黑色)、最终用途(住宅、商业、工业)及地区划分

TMT钢筋市场-全球产业规模、份额、趋势、机会及预测(依等级、直径、应用、地区及竞争细分,2020-2030年)2025-2033年钢筋市场报告,依产品类型(变形钢筋、低碳钢筋)、製程(碱性氧气炼钢、电弧炉)、精加工类型(环氧、涂装、黑色)、最终用途(住宅、商业、工业)及地区划分