|

市场调查报告书

商品编码

1716716

阴道炎治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Vaginitis Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

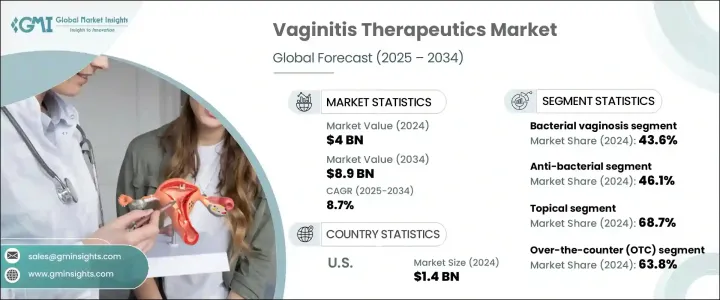

2024 年全球阴道炎治疗市场规模达 40 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 8.7%。阴道感染的发病率上升,加上人们对女性健康的认识不断提高以及可用治疗方案的进步,显着加速了市场成长。随着全球越来越多的女性寻求及时治疗阴道感染,对先进治疗方案的需求持续增加。此外,人们对预防性医疗保健、定期妇科检查和早期诊断的日益重视为治疗创新创造了良好的环境。

医疗保健提供者和製药公司也致力于推出解决復发性感染和提高患者依从性的新配方,例如控释药物和与益生菌的联合疗法。远距医疗和电子药局平台的扩展进一步使城市和农村地区的女性更容易获得这些治疗方法。随着对细菌性阴道炎、念珠菌病和滴虫病等常见阴道感染的了解不断加深,人们对安全有效的药物的需求也越来越大。非处方药 (OTC) 和处方药的日益普及在塑造阴道炎治疗行业的整体格局方面发挥着关键作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 40亿美元 |

| 预测值 | 89亿美元 |

| 复合年增长率 | 8.7% |

市场依疾病类型分为细菌性阴道炎、念珠菌病、滴虫病和其他类型的阴道炎。其中,细菌性阴道炎占据全球主导地位,2024 年的市占率为 43.6%。细菌性阴道炎復发率高,是育龄妇女最常见的感染之一,已成为治疗需求的主要动力。患有復发性细菌性阴道炎的女性通常需要持续治疗,这增加了对处方药和非处方药的需求。细菌性阴道炎率的不断上升以及其慢性特征促使人们对有效且长期的治疗方案产生持续的需求,这使得细菌性阴道炎成为製药商关注的焦点,他们致力于开发创新的解决方案,以最大程度地减少復发并改善患者的预后。

治疗市场也依药物类别分类,包括抗霉菌药、抗菌药、抗原虫药和其他药物类型。抗菌疗法占最大份额,2024 年占 46.1% 的市场。甲硝唑和克林霉素等抗生素因其已被证实的有效性和临床成功率,仍被广泛用于治疗细菌性阴道炎。这些抗生素仍然是治疗阴道炎的第一线选择,推动了高处方率并促进了抗菌药物领域的成长。对抗菌解决方案的强烈偏好反映了对能够有效治疗严重和復发性感染的标靶治疗的需求。

2024 年,北美阴道炎治疗市场规模达到 14 亿美元,这得益于新型抗生素和抗真菌药物的稳步获批,尤其是那些与控释胶囊和益生菌相结合以提高疗效的药物。该地区对能够提供长期缓解并最大限度降低復发率的先进疗法的需求正在激增。随着製药公司专注于创新药物输送机制,监管机构促进下一代疗法的批准,北美将继续占据主导地位,预计仅在 2024 年就将创造 15 亿美元的市场规模。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 阴道感染盛行率高

- 人们对女性健康和有效治疗的认识不断提高

- 药物研发的进展

- 癌症病例增加

- 产业陷阱与挑战

- 抗生素抗药性日益增强

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 差距分析

- 技术格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 竞争定位矩阵

- 供应商矩阵分析

- 策略仪表板

第五章:市场估计与预测:依疾病类型,2021 年至 2034 年

- 主要趋势

- 细菌性阴道炎

- 念珠菌病

- 滴虫病

- 其他疾病类型

第六章:市场估计与预测:依治疗类型,2021 年至 2034 年

- 主要趋势

- 抗菌

- 抗真菌

- 抗原虫

- 其他治疗类型

第七章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 外用

第八章:市场估计与预测:按模式,2021 年至 2034 年

- 主要趋势

- 场外交易(OTC)

- 处方

第九章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 义大利

- 西班牙

- 亚太地区

- 日本

- 中国

- 印度

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Astellas Pharma

- Bayer

- Cipla

- Dare Bioscience

- Dr. Reddy's Laboratories

- Lupin Pharmaceuticals

- Merck

- Novartis

- Pfizer

- Sanofi

- Sun Pharmaceuticals

- Takeda Pharmaceuticals

The Global Vaginitis Therapeutics Market reached USD 4 billion in 2024 and is projected to grow at a CAGR of 8.7% between 2025 and 2034. The rising incidence of vaginal infections, coupled with growing awareness about women's health and advancements in available treatment options, is significantly accelerating market growth. As more women worldwide seek timely medical care for vaginal infections, the demand for advanced therapeutic solutions continues to increase. Additionally, the growing focus on preventive healthcare, regular gynecological check-ups, and early diagnosis has created a favorable environment for therapeutic innovations.

Healthcare providers and pharmaceutical companies are also focusing on introducing novel formulations that address recurrent infections and enhance patient compliance, such as controlled-release drugs and combination therapies with probiotics. The expansion of telemedicine and e-pharmacy platforms is further making these therapeutics more accessible to women in both urban and rural areas. With a growing understanding of common vaginal infections such as bacterial vaginosis, candidiasis, and trichomoniasis, there is a heightened need for safe and effective medications. The increasing acceptance of over-the-counter (OTC) solutions and prescription medications is playing a pivotal role in shaping the overall landscape of the vaginitis therapeutics industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $8.9 Billion |

| CAGR | 8.7% |

The market is segmented by disease type into bacterial vaginosis, candidiasis, trichomoniasis, and other types of vaginitis. Among these, bacterial vaginosis dominated the global landscape, accounting for a 43.6% market share in 2024. Known for its high recurrence rate and being one of the most common infections among women of reproductive age, bacterial vaginosis has become a major driver of therapeutic demand. Women suffering from recurring episodes of bacterial vaginosis often require ongoing treatment, boosting the need for both prescription-based and OTC medications. This increasing prevalence and the chronic nature of the condition are fueling continuous demand for effective and long-term therapeutic options, making bacterial vaginosis a key focus for pharmaceutical manufacturers aiming to develop innovative solutions that minimize recurrence and improve patient outcomes.

The therapeutics market is also categorized by drug class, including anti-fungal, anti-bacterial, anti-protozoal, and other drug types. Anti-bacterial therapeutics held the largest share, accounting for 46.1% of the market in 2024. Antibiotics such as metronidazole and clindamycin remain widely prescribed for bacterial vaginosis due to their proven effectiveness and clinical success. These antibiotics continue to be the first-line choice for treating vaginitis, driving high prescription rates and fueling the growth of the anti-bacterial segment. The strong preference for anti-bacterial solutions reflects the need for targeted therapies that can address severe and recurrent infections efficiently.

North America Vaginitis Therapeutics Market generated USD 1.4 billion in 2024, driven by the steady approval of new antibiotics and anti-fungals, especially those integrated with controlled-release capsules and probiotics for improved efficacy. The region is witnessing an upsurge in demand for advanced therapeutics that offer long-lasting relief and minimize recurrence rates. With pharmaceutical companies focusing on innovative drug delivery mechanisms and regulatory bodies facilitating the approval of next-gen therapeutics, North America is positioned to remain a dominant player, projected to generate USD 1.5 billion in 2024 alone.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High prevalence of vaginal infections

- 3.2.1.2 Growing awareness about women's health and the availability of effective treatments

- 3.2.1.3 Advancements in drug development

- 3.2.1.4 Increasing cases of cancer

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Growing antibiotic resistance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Technology landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Vendor matrix analysis

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bacterial vaginosis

- 5.3 Candidiasis

- 5.4 Trichomoniasis

- 5.5 Other disease type

Chapter 6 Market Estimates and Forecast, By Treatment Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Anti-bacterial

- 6.3 Anti-fungal

- 6.4 Anti-protozoal

- 6.5 Other treatment type

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Topical

Chapter 8 Market Estimates and Forecast, By Mode, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Over-the-counter (OTC)

- 8.3 Prescription

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacy

- 9.3 Retail pharmacy

- 9.4 Online pharmacy

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Astellas Pharma

- 11.2 Bayer

- 11.3 Cipla

- 11.4 Dare Bioscience

- 11.5 Dr. Reddy’s Laboratories

- 11.6 Lupin Pharmaceuticals

- 11.7 Merck

- 11.8 Novartis

- 11.9 Pfizer

- 11.10 Sanofi

- 11.11 Sun Pharmaceuticals

- 11.12 Takeda Pharmaceuticals

全球阴道炎诊断市场规模、份额、趋势和成长分析报告(2026-2034年)全球女性性功能障碍 (FSD) 治疗市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区划分的分析以及未来预测 (2026-2034)

全球阴道炎诊断市场规模、份额、趋势和成长分析报告(2026-2034年)全球女性性功能障碍 (FSD) 治疗市场:市场规模、占有率、成长率、行业分析、依类型、应用和地区划分的分析以及未来预测 (2026-2034) 阴道炎治疗药物市场规模、份额和成长分析(按疾病、产品、通路和地区划分)-2026-2033年产业预测

阴道炎治疗药物市场规模、份额和成长分析(按疾病、产品、通路和地区划分)-2026-2033年产业预测 妇科药物市场-全球产业规模、份额、趋势、机会和预测,依治疗方法、适应症、配销通路、地区和竞争格局划分,2020-2030年预测

妇科药物市场-全球产业规模、份额、趋势、机会和预测,依治疗方法、适应症、配销通路、地区和竞争格局划分,2020-2030年预测 外阴痛治疗市场(按治疗类型、给药途径和最终用户划分)—2025-2032 年全球预测阴道炎治疗市场依治疗方法、给药途径、产品类型、通路和最终用户群划分-2025-2032年全球预测卵巢早衰治疗市场(按治疗类型、最终用户和分销管道)—全球预测 2025-2030

外阴痛治疗市场(按治疗类型、给药途径和最终用户划分)—2025-2032 年全球预测阴道炎治疗市场依治疗方法、给药途径、产品类型、通路和最终用户群划分-2025-2032年全球预测卵巢早衰治疗市场(按治疗类型、最终用户和分销管道)—全球预测 2025-2030 妇产科手术器具市场,规模,占有率,趋势,产业分析报告:各类型,各用途,各终端用户,各地区,2025年~2034年的市场预测

妇产科手术器具市场,规模,占有率,趋势,产业分析报告:各类型,各用途,各终端用户,各地区,2025年~2034年的市场预测 美国性传染感染和阴道炎 PCR 检测市场规模、份额、趋势分析报告:疾病状况、检测类型、最终用途、细分市场预测,2025-2030 年全球性行为感染(STI) 和阴道炎 PCR 检测市场:市场规模、份额、趋势分析(按症状、检测类型、最终用途和地区)、细分市场预测(2025-2030 年)

美国性传染感染和阴道炎 PCR 检测市场规模、份额、趋势分析报告:疾病状况、检测类型、最终用途、细分市场预测,2025-2030 年全球性行为感染(STI) 和阴道炎 PCR 检测市场:市场规模、份额、趋势分析(按症状、检测类型、最终用途和地区)、细分市场预测(2025-2030 年)