|

市场调查报告书

商品编码

1716722

加氢植物油市场机会、成长动力、产业趋势分析及2025-2034年预测Hydrotreated Vegetable Oil Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

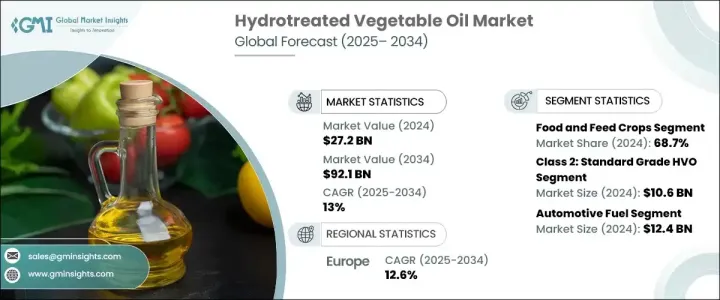

2024 年全球加氢植物油市场规模达到 272 亿美元,预计 2025 年至 2034 年期间的复合年增长率将达到 13%。向再生能源的日益转变正在迅速提升 HVO 作为各行各业可持续燃料替代品的作用。随着全球经济转向减少对化石燃料的依赖,HVO 正成为实现脱碳目标的关键解决方案。它可以作为传统柴油的直接替代品,加上更清洁的燃烧和更低的温室气体排放,正在推动交通运输、航空和工业发电等主要行业的需求。

一些国家的政府,特别是北美和欧洲的政府,正在透过税收抵免、混合授权和排放上限等政策框架加强削减碳排放的授权,直接鼓励使用 HVO。这些政策为 HVO 生产商开闢了新的成长机会,并加强了它们在全球向绿色能源转变的重要性。随着企业探索扩大 HVO 生产规模并保持成本竞争力的创新方法,公共和私人对先进生物燃料和下一代原料的投资不断增加,进一步增强了市场前景。随着越来越多的产业寻求 ESG(环境、社会和治理)目标,对 HVO 等清洁燃烧、低碳替代品的关注度不断加大,推动了已开发经济体和新兴经济体的快速采用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 272亿美元 |

| 预测值 | 921亿美元 |

| 复合年增长率 | 13% |

2024 年,粮食和饲料作物占据 HVO 市场的 68.7%,预计到 2034 年将以 12.4% 的复合年增长率增长。粮食和饲料作物在 HVO 生产中的广泛使用很大程度上是由于其丰富的供应、强大的供应链以及完善的农业框架的支持。大豆和油菜籽等作物对于高效生产 HVO 所需的油脂供应至关重要,可确保稳定的原料供应以满足日益增长的生物燃料需求。儘管人们对粮食安全和土地使用的担忧日益受到关注,但各地区的政策仍支持以农作物为基础的生物燃料,进一步推动了市场成长。

市场也按等级细分,包括高级、标准级、基础级和特种级。其中,标准级 HVO 市场在 2024 年创造了 106 亿美元的收入,预计在 2025 年至 2034 年期间的复合年增长率将达到 12.7%。标准级因其成本、性能和多功能性的平衡而越来越受到青睐,使其成为运输、工业运营和发电的理想选择。与通常用于利基高性能领域的高端优质产品相比,它符合严格的排放标准,同时保持经济可行性。

从地区来看,欧洲加氢植物油市场规模在 2024 年达到 103 亿美元,预计到 2034 年将以 12.6% 的复合年增长率成长。在强有力的监管支持和对再生燃料不断增长的需求的推动下,欧洲继续引领全球加氢植物油市场。欧盟的RED II指令和不断增加的生物燃料混合要求极大地加速了HVO的整合,使欧洲处于全球向低碳能源转型努力的前沿。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- HVO生产技术的进步

- 对再生能源的需求不断增长

- 汽车产业需求不断成长

- 产业陷阱与挑战

- 生产成本高

- 来自其他再生燃料的竞争

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场规模及预测:依原料来源,2021 年至 2034 年

- 主要趋势

- 粮食和饲料作物

- 大豆油

- 菜籽油

- 葵花籽油

- 棕榈油

- 其他的

- 动物脂肪

- 脂

- 猪油

- 废弃食用油

- 棕榈油厂废水

- 其他的

第六章:市场规模及预测:依等级,2021 年至 2034 年

- 主要趋势

- 第 1 类:优质 HVO

- 第 2 类:标准级 HVO

- 第 3 类:基础级 HVO

- 第 4 类:特种级 HVO

第七章:市场规模及预测:依技术分类,2021 年至 2034 年

- 主要趋势

- 独立加氢处理技术

- 协同处理技术

第 8 章:市场规模与预测:按应用,2021 年至 2034 年

- 主要趋势

- 永续航空燃料

- 汽车燃料

- 船用燃料

- 工业发电

- 加热燃料

- 农业设备燃料

- 润滑剂

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- ALFA LAVAL

- Cepsa

- Desmet

- DIAMOND GREEN DIESEL

- Neste

- Preem

- Repsol

- Shell

- TotalEnergies

- UPM Biofuels

- Valero Energy

- World Energy

The Global Hydrotreated Vegetable Oil Market reached USD 27.2 billion in 2024 and is projected to expand at a CAGR of 13% between 2025 and 2034. The growing shift toward renewable energy sources is rapidly elevating HVO's role as a sustainable fuel alternative across industries. As global economies pivot to reducing dependence on fossil fuels, HVO is emerging as a critical solution for meeting decarbonization goals. Its ability to serve as a drop-in replacement for traditional diesel, combined with cleaner combustion and lower greenhouse gas emissions, is pushing demand among major sectors, including transportation, aviation, and industrial power generation.

Several governments, particularly in North America and Europe, are stepping up mandates to cut carbon emissions with policy frameworks like tax credits, blending mandates, and emission caps that directly encourage the use of HVO. These policies are opening new growth opportunities for HVO producers and reinforcing their importance in the global shift toward greener energy. Increasing public and private investments in advanced biofuels and next-generation feedstocks are further enhancing the market outlook as companies explore innovative ways to scale HVO production while keeping costs competitive. As more industries seek to meet ESG (Environmental, Social, and Governance) goals, the focus on clean-burning, low-carbon alternatives like HVO continues to intensify, fueling rapid adoption across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.2 Billion |

| Forecast Value | $92.1 Billion |

| CAGR | 13% |

In 2024, the food and feed crops segment dominated the HVO market with a 68.7% share and is anticipated to grow at a CAGR of 12.4% through 2034. The widespread use of food and feed crops in HVO production is largely driven by their abundant availability, robust supply chains, and the well-established agricultural framework supporting them. Crops like soybeans and rapeseed are pivotal in supplying the oils required for efficient HVO production, ensuring a steady feedstock supply to meet growing biofuel demand. While concerns around food security and land use are gaining attention, policies across regions still back crop-based biofuels, further propelling market growth.

The market is also segmented by grade, covering premium grade, standard grade, basic grade, and specialty grade. Among these, the standard grade HVO segment generated USD 10.6 billion in 2024 and is set to grow at a CAGR of 12.7% from 2025 to 2034. Standard grade is increasingly preferred due to its balance of cost, performance, and versatility, making it an ideal choice for transportation, industrial operations, and power generation. It meets stringent emission norms while remaining economically viable compared to higher-end premium grades that are typically used in niche, high-performance sectors.

Regionally, Europe's Hydrotreated Vegetable Oil Market reached USD 10.3 billion in 2024 and is projected to grow at a CAGR of 12.6% through 2034. Europe continues to lead the global HVO landscape, driven by powerful regulatory backing and escalating demand for renewable fuels. The European Union's RED II directive and rising biofuel blending mandates have greatly accelerated HVO integration, positioning Europe at the forefront of global efforts to transition to low-carbon energy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Advancements in HVO production technology

- 3.6.1.2 Growing demand for renewable energy sources

- 3.6.1.3 Increasing demand from the automotive sector

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High production costs

- 3.6.2.2 Competition from other renewable fuels

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Source of Feedstock, 2021 – 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Food and feed crops

- 5.2.1 Soybean oil

- 5.2.2 Canola oil

- 5.2.3 Sunflower oil

- 5.2.4 Palm oil

- 5.2.5 Others

- 5.3 Animal fats

- 5.3.1 Tallow

- 5.3.2 Lard

- 5.4 Used cooking oils

- 5.5 Palm oil mill effluent

- 5.6 Others

Chapter 6 Market Size and Forecast, By Grade, 2021 – 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Class 1: premium grade HVO

- 6.3 Class 2: standard grade HVO

- 6.4 Class 3: basic grade HVO

- 6.5 Class 4: specialty grade HVO

Chapter 7 Market Size and Forecast, By Technology, 2021 – 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Standalone hydrotreating technology

- 7.3 Co-Processing technology

Chapter 8 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Sustainable aviation fuel

- 8.3 Automotive fuel

- 8.4 Marine fuel

- 8.5 Industrial power generation

- 8.6 Heating fuel

- 8.7 Agricultural equipment fuel

- 8.8 Lubricants

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 ALFA LAVAL

- 10.2 Cepsa

- 10.3 Desmet

- 10.4 DIAMOND GREEN DIESEL

- 10.5 Neste

- 10.6 Preem

- 10.7 Repsol

- 10.8 Shell

- 10.9 TotalEnergies

- 10.10 UPM Biofuels

- 10.11 Valero Energy

- 10.12 World Energy