|

市场调查报告书

商品编码

1721402

胃食道逆流症治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Gastroesophageal Reflux Disease Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

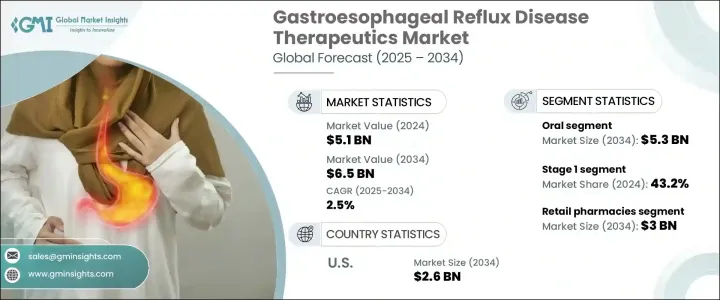

2024 年全球胃食道逆流症治疗市场价值为 51 亿美元,预计到 2034 年将以 2.5% 的复合年增长率成长,达到 65 亿美元。 GERD 持续对全球造成越来越大的健康负担,随着饮食模式的改变、酒精和烟草消费的增加、久坐的生活方式以及全球肥胖率的上升,GERD 病例不断增加。这种慢性疾病是由胃酸倒流到食道引起的,会导致胃灼热、胸痛和逆流等症状,如果不及时治疗,可能会导致食道炎甚至食道癌等併发症。随着人们对胃食道逆流症及其併发症的认识不断提高,越来越多的人开始寻求及时的医疗介入。

製药商正在改进药物开发技术,不仅可以缓解症状,还可以提供长期管理解决方案。新型质子帮浦抑制剂 (PPI)、缓释製剂和联合疗法的引入正在改善临床结果,同时也提高了患者的依从性。这些创新反映了业界向以患者为中心的解决方案的更广泛转变,公司优先考虑有效、可及且耐受性良好的治疗方法,以满足不同年龄层和风险状况的未满足的医疗需求。发展中市场医疗保健服务的普及以及非处方药零售通路的扩大也支持了全球市场的持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 51亿美元 |

| 预测值 | 65亿美元 |

| 复合年增长率 | 2.5% |

GERD 治疗市场按药物类别细分,包括 PPI、H2 受体拮抗剂 (H2RA)、抗酸剂、促动力剂等。 2024 年,光是抗酸剂就创造了 22 亿美元的收入。它们之所以受欢迎是因为它们能够快速缓解胃灼热和消化不良等症状,使其成为寻求立即缓解的患者的首选。它们作为非处方产品广泛普及,增加了它们的便利性和广泛的吸引力,使患者无需处方干预即可自行管理轻度 GERD 症状。

根据给药途径,GERD 治疗市场分为口服和注射部分。口服製剂,尤其是 PPI 和抗酸剂,在 2024 年占了 80% 的份额。人们对口服药物的强烈偏好归因于其易于使用、价格实惠且广泛可及。由于能够在柜檯购买许多口服药物,患者可以享受更快的治疗开始和更低的医疗保健成本,这可能会巩固该领域在 2034 年之前的主导地位。

预计到 2034 年,美国胃食道逆流治疗市场规模将达到 26 亿美元。 GERD 盛行率不断上升(部分原因是不良的饮食习惯和肥胖率上升)继续推动对先进治疗方法的需求。由于持续创新、不断加强的宣传活动以及强大的品牌和仿製药疗法(包括促动力剂等新兴选择),美国市场正在经历显着增长。

全球 GERD 治疗市场的知名参与者包括阿斯特捷利康、Camber Pharmaceuticals、卫材、强生、Onconic Therapeutics、辉瑞、Phathom Pharmaceuticals、Sebela Pharmaceuticals、武田製药、Teva Pharmaceuticals 和 Viatris。这些公司正在透过增强药物输送系统、临床研究和扩大分销管道积极创新。他们还投资与医疗保健提供者建立合作伙伴关係,以加强患者的就医机会并提高治疗效果。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 胃食道逆流症(GERD)盛行率上升

- 药物输送系统的技术进步

- 提高消费者意识

- 产业陷阱与挑战

- 副作用和安全问题

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按药物类别,2021 - 2034 年

- 主要趋势

- 质子帮浦抑制剂(PPI)

- H2受体拮抗剂(H2RAs)

- 抗酸药

- 促动力剂

- 其他药物类别

第六章:市场估计与预测:按管理路线,2021 - 2034 年

- 主要趋势

- 口服

- 注射剂

第七章:市场估计与预测:按阶段,2021 - 2034 年

- 主要趋势

- 第一阶段

- 第 2 阶段

- 第 3 阶段

- 第四阶段

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- AstraZeneca

- Camber Pharmaceuticals

- Eisai

- Johnson & Johnson

- Onconic Therapeutics

- Pfizer

- Phathom Pharmaceuticals

- Sebela Pharmaceuticals

- Takeda Pharmaceutical Company

- Teva Pharmaceuticals

- Viatris

The Global Gastroesophageal Reflux Disease Therapeutics Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 2.5% to reach USD 6.5 billion by 2034. GERD continues to pose a growing health burden worldwide, with a rising cases driven by shifting dietary patterns, increased alcohol and tobacco consumption, sedentary lifestyles, and the global rise in obesity. This chronic condition, caused by the backward flow of stomach acid into the esophagus, leads to symptoms like heartburn, chest pain, and regurgitation, and if left untreated, may result in complications such as esophagitis and even esophageal cancer. As awareness around GERD and its complications grows, more individuals are seeking timely medical interventions.

Pharmaceutical manufacturers are responding with improved drug development technologies that not only relieve symptoms but also offer long-term management solutions. The introduction of novel proton pump inhibitors (PPIs), extended-release formulations, and combination therapies is improving clinical outcomes while also enhancing patient compliance. These innovations reflect a broader industry shift toward patient-centric solutions, with companies prioritizing effective, accessible, and well-tolerated therapeutics to meet unmet medical needs across different age groups and risk profiles. Increasing access to healthcare in developing markets and expanding retail availability of over-the-counter options are also supporting sustained market growth on a global scale.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $6.5 Billion |

| CAGR | 2.5% |

The market for GERD therapeutics is segmented by drug class, including PPIs, H2 receptor antagonists (H2RAs), antacids, prokinetic agents, and others. In 2024, antacids alone generated USD 2.2 billion in revenue. Their popularity stems from their ability to offer quick relief from symptoms such as heartburn and acid indigestion, making them the go-to choice for patients seeking immediate comfort. Their wide availability as over-the-counter products adds to their convenience and broad appeal, allowing patients to self-manage mild GERD symptoms without prescription intervention.

By route of administration, the GERD therapeutics market is divided into oral and injectable segments. Oral formulations, particularly PPIs and antacids, accounted for an 80% share in 2024. This strong preference for oral drugs is attributed to their ease of use, affordability, and widespread accessibility. With the ability to purchase many oral therapies over the counter, patients benefit from faster treatment initiation and lower healthcare costs, which will likely reinforce the dominance of this segment through 2034.

The U.S. Gastroesophageal Reflux Disease Therapeutics Market is projected to reach USD 2.6 billion by 2034. The increasing prevalence of GERD, partly driven by poor dietary habits and rising obesity rates, continues to drive demand for advanced treatments. The U.S. market is witnessing significant growth thanks to continuous innovation, increasing awareness campaigns, and a strong pipeline of branded and generic therapies, including emerging options like prokinetic agents.

Notable players in the Global GERD Therapeutics Market include AstraZeneca, Camber Pharmaceuticals, Eisai, Johnson & Johnson, Onconic Therapeutics, Pfizer, Phathom Pharmaceuticals, Sebela Pharmaceuticals, Takeda Pharmaceutical Company, Teva Pharmaceuticals, and Viatris. These companies are actively innovating through enhanced drug delivery systems, clinical research, and expanded distribution channels. They are also investing in partnerships with healthcare providers to strengthen patient access and elevate treatment outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of gastroesophageal reflux disease (GERD)

- 3.2.1.2 Technological advancements in drug delivery systems

- 3.2.1.3 Increasing consumer awareness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects and safety concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Future market trends

- 3.6 Gap analysis

- 3.7 Porter’s analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Proton pump inhibitors (PPIs)

- 5.3 H2 receptor antagonists (H2RAs)

- 5.4 Antacids

- 5.5 Prokinetic agents

- 5.6 Other drug classes

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Injectable

Chapter 7 Market Estimates and Forecast, By Stage, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stage 1

- 7.3 Stage 2

- 7.4 Stage 3

- 7.5 Stage 4

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AstraZeneca

- 10.2 Camber Pharmaceuticals

- 10.3 Eisai

- 10.4 Johnson & Johnson

- 10.5 Onconic Therapeutics

- 10.6 Pfizer

- 10.7 Phathom Pharmaceuticals

- 10.8 Sebela Pharmaceuticals

- 10.9 Takeda Pharmaceutical Company

- 10.10 Teva Pharmaceuticals

- 10.11 Viatris