|

市场调查报告书

商品编码

1721457

血浆蛋白酶 C1 抑制剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Plasma Protease C1-inhibitor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

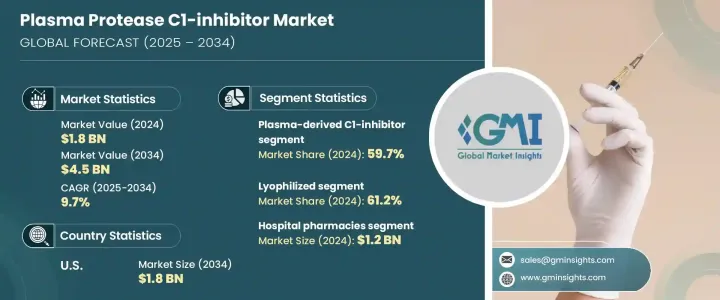

2024 年全球血浆蛋白酶 C1 抑制剂市值为 18 亿美元,预计到 2034 年将以 9.7% 的复合年增长率成长至 45 亿美元。血浆蛋白酶 C1 抑制剂在控制人体内补体和接触系统的活化方面发挥着至关重要的作用。这些来自血浆的蛋白质对于治疗遗传性血管性水肿(HAE)等罕见遗传疾病至关重要。随着医疗保健系统的不断发展,人们对罕见疾病管理的认识不断提高,这极大地促进了对 C1 抑制剂等有效和专业疗法的需求。

血浆分离和收集方法的技术进步正在透过提高血浆衍生疗法的产量和纯度来重塑生物製剂的模式。反过来,这些发展使得医疗服务提供者和患者更容易获得治疗,治疗费用更低,治疗规模也更大。随着临床兴趣的不断增长和个人化医疗的出现,市场有望在发炎和自体免疫疾病等新治疗应用方面取得更大的渗透。已开发经济体和新兴经济体的监管支持和不断增加的医疗保健基础设施进一步促进了市场扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 45亿美元 |

| 复合年增长率 | 9.7% |

就药物类别而言,血浆衍生的 C1 抑制剂领域占据市场主导地位,占 2024 年全球份额的 59.7%。虽然也有选择性缓激肽 B2 受体拮抗剂和激肽释放酶抑制剂等替代方案,但目前它们在市场中所占份额较小。血浆衍生製剂仍然是首选,因为它们具有已确定的安全性,并且在管理 HAE 的急性和预防性治疗方面已证明有效。

从剂型来看,冷冻干燥 C1 抑制剂将继续引领市场,2024 年的市占率为 61.2%。这些冷冻干燥製剂因其较长的保质期而受到青睐,并且不需要冷藏,非常适合在可靠冷链基础设施有限的地区使用。这一优势在农村医疗保健环境和中低收入国家尤其重要,因为这些地方保持一致的储存条件可能是一个挑战。

美国血浆蛋白酶 C1 抑制剂市场正在经历强劲成长。 2024 年的价值为 7.294 亿美元,预计到 2034 年将达到 18 亿美元。推动这一增长的因素包括 HAE 盛行率的上升、基因筛检的改善、早期诊断意识的提高以及罕见疾病治疗机会的扩大。美国 FDA 对孤儿药(特别是针对 HAE 等疾病的孤儿药)的持续支持正在加速产品审批并鼓励该领域的更多创新。

市场的主要参与者包括 BioCryst Pharmaceuticals、武田製药公司、KalVista、Ionis Pharmaceuticals、CSL Behring、Fresenius Kabi、Pharming、Pharvaris 和 Astria。这些公司正在大力投资研发,以发现 C1 抑制剂的新适应症,尤其是在免疫学和发炎领域。策略合作也透过扩大产品线和加速下一代疗法来推动成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 遗传性血管性水肿 (HAE) 和补体系统疾病盛行率上升

- 生物技术和药物开发的进步

- 有利的政府法规和报销政策

- 罕见疾病研发投资不断增加

- 产业陷阱与挑战

- C1抑制剂疗法成本高昂

- 供应有限和供应链限制

- 成长动力

- 成长潜力分析

- 监管格局

- 差距分析

- 专利分析

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按药物类别,2021 年至 2034 年

- 主要趋势

- 血浆衍生的C1抑制剂

- 选择性缓激肽B2受体拮抗剂

- 激肽释放酶抑制剂

第六章:市场估计与预测:按剂型,2021 年至 2034 年

- 主要趋势

- 冷冻干燥

- 注射剂

第七章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 电子商务

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Astria

- BioCryst Pharmaceuticals

- CSL Behring

- Fresenius Kabi

- Ionis Pharmaceuticals

- KalVista

- Pharming

- Pharvaris

- Takeda Pharmaceutical Company

The Global Plasma Protease C1-Inhibitor Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 9.7% to reach USD 4.5 billion by 2034. Plasma protease C1-inhibitors serve a vital role in controlling the activation of the complement and contact systems within the human body. These proteins, derived from blood plasma, are crucial in the treatment of rare genetic disorders such as Hereditary Angioedema (HAE). As healthcare systems continue to evolve, there is increasing awareness surrounding rare disease management, which is significantly contributing to the demand for effective and specialized therapies like C1-inhibitors.

Technological progress in plasma fractionation and collection methods is reshaping the landscape of biologics by enhancing the yield and purity of plasma-derived therapies. In turn, these developments are making treatments more accessible, affordable, and scalable for healthcare providers and patients alike. With growing clinical interest and the emergence of personalized medicine, the market is poised to witness greater penetration across new therapeutic applications, such as inflammatory and autoimmune diseases. Regulatory support and increasing healthcare infrastructure in both developed and emerging economies are further bolstering market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 9.7% |

In terms of drug classes, the plasma-derived C1-inhibitor segment dominated the market, accounting for 59.7% of the global share in 2024. While alternative options like selective bradykinin B2 receptor antagonists and Kallikrein inhibitors are also available, they currently serve as smaller segments within the market. Plasma-derived formulations remain the preferred option due to their established safety profiles and proven efficacy in managing acute and prophylactic treatment for HAE.

When looking at dosage forms, lyophilized C1-inhibitors continue to lead the market with a 61.2% share in 2024. These freeze-dried formulations are favored for their extended shelf life and do not require refrigeration, making them ideal for use in regions with limited access to reliable cold chain infrastructure. This advantage is particularly critical in rural healthcare settings and low-to-middle-income countries where consistent storage conditions can be a challenge.

The U.S. Plasma Protease C1-Inhibitor Market is experiencing robust growth. Valued at USD 729.4 million in 2024, it is projected to reach USD 1.8 billion by 2034. The expansion is driven by the rising prevalence of HAE, improvements in genetic screening, increased awareness of early diagnosis, and broader access to rare disease treatments. The U.S. FDA's continued support for orphan drugs, particularly for conditions like HAE, is accelerating product approvals and encouraging more innovation in this space.

Key players in the market include BioCryst Pharmaceuticals, Takeda Pharmaceutical Company, KalVista, Ionis Pharmaceuticals, CSL Behring, Fresenius Kabi, Pharming, Pharvaris, and Astria. These companies are heavily investing in R&D to discover new indications for C1-inhibitors, especially in the fields of immunology and inflammation. Strategic collaborations are also fueling growth by expanding product pipelines and fast-tracking next-generation therapies.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of hereditary angioedema (HAE) and complement system disorders

- 3.2.1.2 Advancements in biotechnology and drug development

- 3.2.1.3 Favorable government regulations and reimbursement policies

- 3.2.1.4 Growing investment in rare disease research and development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of C1-inhibitor therapies

- 3.2.2.2 Limited availability and supply chain constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Gap analysis

- 3.6 Patent analysis

- 3.7 Pipeline analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Plasma-derived C1-inhibitor

- 5.3 Selective bradykinin B2 receptor antagonist

- 5.4 Kallikrein inhibitor

Chapter 6 Market Estimates and Forecast, By Dosage Form, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lyophilized

- 6.3 Injectables

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Astria

- 9.2 BioCryst Pharmaceuticals

- 9.3 CSL Behring

- 9.4 Fresenius Kabi

- 9.5 Ionis Pharmaceuticals

- 9.6 KalVista

- 9.7 Pharming

- 9.8 Pharvaris

- 9.9 Takeda Pharmaceutical Company