|

市场调查报告书

商品编码

1721474

浸润性乳管癌 (IDC) 治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Invasive Ductal Carcinoma (IDC) Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

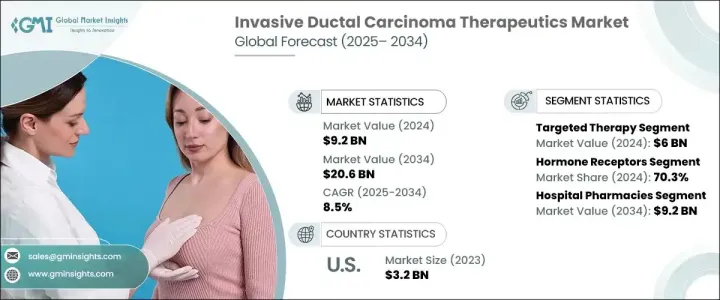

2024 年全球浸润性乳管癌治疗市场价值为 92 亿美元,预计到 2034 年将以 8.5% 的复合年增长率成长,达到 206 亿美元。这一强劲的成长前景受到全球乳癌盛行率持续上升的推动,其中浸润性乳管癌是最常见的诊断亚型。 IDC 占所有侵袭性乳癌病例的近 80%,是肿瘤学领域的重要关注领域。随着乳癌筛检计画的扩大和早期检测的改善,医疗保健提供者正在见证 IDC 诊断数量的显着增加。这反过来又继续推动对有效的、以患者为中心的治疗方法的需求,这些治疗方法不仅可以提高生存率,还可以提高生活品质。癌症负担日益加重,加速了治疗创新的需求,IDC 治疗领域正在快速发展,以先进的解决方案满足这一需求。患者和临床医生意识的提高、有利的报销方案以及已开发和新兴经济体医疗保健基础设施的扩大也促进了该市场的持续发展。

虽然传统化疗仍然是治疗 IDC 的关键组成部分,但向创新和标靶治疗的转变正在加速。基于荷尔蒙的疗法和生物製剂由于其疗效增强且毒性降低而成为首选的治疗选择。芳香化酶抑制剂和选择性雌激素受体降解剂 (SERD) 等疗法对荷尔蒙受体阳性 (HR+) IDC 病例特别有效,这类病例占诊断的很大一部分。这些治疗方法帮助患者更好地控制病情,减少副作用,促使医生和患者都倾向于这种先进的方法。因此,标靶治疗正在成为 IDC 护理方案中不可或缺的元素,进一步巩固了市场的上升趋势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 92亿美元 |

| 预测值 | 206亿美元 |

| 复合年增长率 | 8.5% |

IDC 治疗市场依最终用途分为医院、肿瘤诊所和其他医疗机构。由于医院能够提供全面癌症治疗、最先进的诊断系统以及多学科肿瘤学团队,预计到 2034 年医院的收入将达到 36 亿美元。这些环境支持涉及化疗、免疫疗法和精准医疗的复杂治疗方案的综合管理,仍然是 IDC 治疗的首选。

在北美,美国占据浸润性乳管癌治疗市场的领先份额,这得益于该地区的高发病率和强大的医疗保健框架。知名癌症治疗中心的存在和新型疗法的广泛普及推动了 IDC 治疗的采用。

该领域的领先公司包括 AbbVie、AstraZeneca、Bristol-Myers Squibb、Celldex Therapeutics、Eli Lilly、F. Hoffmann-La Roche、Janssen Pharmaceuticals、Macrogenics、Merck、Novartis 和 Pfizer。这些参与者正在大力投资研发,以推出能够带来更好临床效果和更少副作用的尖端免疫疗法和联合疗法。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 乳癌盛行率和认知度不断提高

- 改进的诊断技术

- 扩大治疗选择

- 产业陷阱与挑战

- 治疗费用高

- 副作用和对某些疗法的抵抗力

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 标靶治疗

- 阿贝马西利

- 阿多曲妥珠单抗

- 依维莫司

- 曲妥珠单抗

- 瑞博西利

- 帕博西利

- 帕妥珠单抗

- 奥拉帕尼

- 其他标靶治疗

- 荷尔蒙疗法

- 选择性雌激素受体调节剂(SERM)

- 芳香化酶抑制剂

- 选择性雌激素受体降解剂(SERD)

- 化疗

- 免疫疗法

第六章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 荷尔蒙受体

- HER2+

- 三阴性乳癌(TNBC)

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 肿瘤诊所

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AbbVie

- AstraZeneca

- Bristol-Myers Squibb Company

- Celldex Therapeutics

- Eli Lilly and Company

- F. Hoffmann-La Roche

- Gilead Sciences

- Janssen Pharmaceuticals

- Macrogenics

- Merck

- Novartis

- Pfizer

The Global Invasive Ductal Carcinoma Therapeutics Market was valued at USD 9.2 billion in 2024 and is projected to grow at a CAGR of 8.5% to reach USD 20.6 billion by 2034. This robust growth outlook is fueled by the consistently rising prevalence of breast cancer worldwide, with invasive ductal carcinoma being the most frequently diagnosed subtype. IDC accounts for nearly 80% of all invasive breast cancer cases, making it a significant area of focus in oncology. As breast cancer screening programs expand and early detection improves, healthcare providers are witnessing a notable increase in the number of IDC diagnoses. This, in turn, continues to drive demand for effective, patient-centric therapies that not only improve survival rates but also enhance the quality of life. The growing burden of cancer has accelerated the need for treatment innovation, and the IDC therapeutics space is rapidly evolving to meet that need with advanced solutions. Increasing awareness among patients and clinicians, favorable reimbursement scenarios, and expanding healthcare infrastructure across developed and emerging economies are also contributing to this market's sustained momentum.

While conventional chemotherapy remains a key component in managing IDC, the shift toward innovative and targeted therapies is gaining speed. Hormone-based therapies and biologics are becoming the preferred treatment options due to their enhanced efficacy and reduced toxicity profiles. Therapies such as aromatase inhibitors and selective estrogen receptor degraders (SERDs) are especially effective in hormone receptor-positive (HR+) IDC cases, which represent a significant portion of diagnoses. These treatments are helping patients achieve better disease control with fewer side effects, prompting both physicians and patients to lean toward such advanced approaches. As a result, targeted therapeutics are becoming an indispensable element in IDC care protocols, further reinforcing the market's upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $20.6 Billion |

| CAGR | 8.5% |

The IDC therapeutics market is segmented by end-use into hospitals, oncology clinics, and other healthcare facilities. Hospitals are expected to generate USD 3.6 billion by 2034, owing to their ability to provide integrated cancer care, state-of-the-art diagnostic systems, and access to multidisciplinary oncology teams. These environments support comprehensive management of complex treatment regimens involving chemotherapy, immunotherapy, and precision medicines, thereby remaining the go-to option for IDC treatment.

In North America, the U.S. holds a leading share of the invasive ductal carcinoma therapeutics market, backed by the region's high disease prevalence and strong healthcare framework. The presence of renowned cancer treatment centers and widespread access to novel therapeutics are driving the adoption of IDC treatments.

Leading companies in this space include AbbVie, AstraZeneca, Bristol-Myers Squibb, Celldex Therapeutics, Eli Lilly, F. Hoffmann-La Roche, Janssen Pharmaceuticals, Macrogenics, Merck, Novartis, and Pfizer. These players are investing heavily in R&D to introduce cutting-edge immunotherapies and combination therapies that deliver better clinical outcomes and fewer side effects.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence and awareness of breast cancer

- 3.2.1.2 Improved diagnostic technologies

- 3.2.1.3 Expanding therapeutic options

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment cost

- 3.2.2.2 Side effects and resistance to certain therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Targeted therapy

- 5.2.1 Abemaciclib

- 5.2.2 Ado-trastuzumab emtansine

- 5.2.3 Everolimus

- 5.2.4 Trastuzumab

- 5.2.5 Ribociclib

- 5.2.6 Palbociclib

- 5.2.7 Pertuzumab

- 5.2.8 Olaparib

- 5.2.9 Other targeted therapies

- 5.3 Hormone therapy

- 5.3.1 Selective estrogen receptor modulators (SERMs)

- 5.3.2 Aromatase inhibitors

- 5.3.3 Selective estrogen receptor degraders (SERDs)

- 5.4 Chemotherapy

- 5.5 Immunotherapy

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hormone receptor

- 6.3 HER2+

- 6.4 Triple-negative breast cancer (TNBC)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 AstraZeneca

- 9.3 Bristol-Myers Squibb Company

- 9.4 Celldex Therapeutics

- 9.5 Eli Lilly and Company

- 9.6 F. Hoffmann-La Roche

- 9.7 Gilead Sciences

- 9.8 Janssen Pharmaceuticals

- 9.9 Macrogenics

- 9.10 Merck

- 9.11 Novartis

- 9.12 Pfizer

浸润性乳管癌治疗市场-全球产业规模、份额、趋势、机会、预测:治疗方法、类型、分销管道、地区和竞争格局划分,2021-2031年

浸润性乳管癌治疗市场-全球产业规模、份额、趋势、机会、预测:治疗方法、类型、分销管道、地区和竞争格局划分,2021-2031年 浸润性乳管癌治疗市场规模、份额、趋势分析报告:按治疗方法、类型、分销管道、地区和细分市场进行预测,2025-2030 年

浸润性乳管癌治疗市场规模、份额、趋势分析报告:按治疗方法、类型、分销管道、地区和细分市场进行预测,2025-2030 年