|

市场调查报告书

商品编码

1721614

专用商用车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Specialty Commercial Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

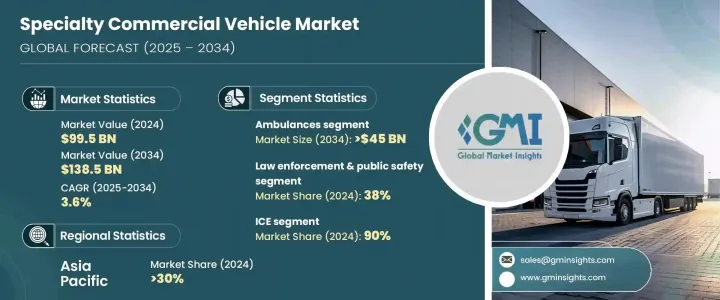

2024 年全球专用商用车市场价值为 995 亿美元,预计到 2034 年将以 3.6% 的复合年增长率成长,达到 1,385 亿美元。该市场的成长轨迹受到针对紧急应变、医疗保健和公共安全的专业运输解决方案不断增长的需求的推动。随着城市化进程的加速和医疗保健系统的发展,人们越来越依赖能够直接为社区提供基本服务的行动医疗单位。政府和私人组织正在扩大其车队,以提高可及性和回应能力,特别是在服务不足和偏远地区。慢性病负担加重、老龄化人口不断增加以及对预防保健的日益重视,促使当局投资配备智慧医疗功能的车辆。此外,在后疫情时代,感染控制和远端诊断已成为核心考虑因素,进一步刺激了对符合现代医疗标准的专用车辆的需求。从高科技救护车到行动诊所和消防救援队,全球市场正在经历由创新、技术整合以及向分散护理和公共安全运营的更广泛转变所推动的转型。

随着对先进紧急应变系统(包括下一代救护车和行动医疗单位)的投资不断增加,对专用车辆的需求持续上升。公众健康意识的增强,加上向农村和偏远地区提供医疗服务的再度推动,正在推动移动 ICU 车和护理车辆的部署。感染控制协议和远距医疗工具的日益普及进一步加速了全球市场对现代专用车辆的需求。同时,天灾和气候引发的紧急情况日益频繁,促使各国加强消防队和公共安全车辆基础设施。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 995亿美元 |

| 预测值 | 1385亿美元 |

| 复合年增长率 | 3.6% |

2024 年,救护车占全球市场的 40%,预计到 2034 年将创造 450 亿美元的市场价值。政府和私人医疗保健营运商优先考虑缩短紧急应变时间,并为车辆配备最先进的通讯系统、5G 连接和即时病患监控解决方案。这些创新实现了医院在运输过程中的无缝协调和更好的患者治疗效果。随着数位医疗的不断发展,智慧救护车技术有望在下一代紧急应变策略中发挥关键作用。

2024 年,执法和公共安全车辆占据了 38% 的市场份额,承担着从移动诊断实验室到偏远地区治疗单位等多种角色。随着医疗保健服务模式日益分散,提供诊断、门诊护理和透析的行动服务发展势头强劲。这些车辆支援家庭护理服务并增强了资源匮乏地区的医疗服务,推动了专用车辆设计的新一轮创新浪潮。

到 2024 年,亚太地区将占全球市场的 30%,这主要得益于中国快速的基础建设和对智慧移动的投资。受政府支持清洁、永续车队的激励政策推动,该地区对救护车、消防车和多用途货车的需求不断增长。

Farber Specialty Vehicles、Mercedes-Benz、Volvo、五十铃、Traton、Pierce、REV、LDV、Oshkosh Corporation 和 NFI 等主要参与者正在透过电气化、模组化设计和人工智慧诊断突破极限。与市政当局和医疗保健提供者的策略合作正在帮助这些公司加强当地影响力并满足各地区日益增长的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件供应商

- 製造商

- 服务提供者

- 经销商

- 最终用途

- 川普政府关税的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响

- 需求面影响

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 价格趋势

- 成本細項分析

- 衝击力

- 成长动力

- 全球紧急医疗服务需求不断成长

- 增加政府对灾害应变的投资

- 远程工业活动日益增多

- 休閒旅游激增

- 产业陷阱与挑战

- 初始成本高且生产週期长

- 严格的监管和认证要求

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 救护车

- 消防车

- 移动式燃油运输油罐车

- 其他的

第六章:市场估计与预测:以推进方式,2021 - 2034 年

- 主要趋势

- 冰

- 电的

- 纯电动车

- 油电混合车

- 插电式混合动力

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 医疗保健

- 执法与公共安全

- 休閒车

- 市政服务

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Arctic Cat

- Cargotec

- Case New Holland

- Demers Ambulances

- Eicher

- Emergency One

- Farber Specialty Vehicles

- Hino Motors

- Isuzu

- LDV

- Matthews Specialty Vehicles

- Mercedes-Benz

- NFI

- Oshkosh Corporation

- Pierce

- REV

- Rosenbauer International

- Specialty Vehicles

- Traton

- Volvo

The Global Specialty Commercial Vehicle Market was valued at USD 99.5 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 138.5 billion by 2034. The growth trajectory of this market is being driven by rising demand for specialized transportation solutions tailored to emergency response, healthcare delivery, and public safety. As urbanization accelerates and healthcare systems evolve, there is a growing reliance on mobile units that can bring essential services directly to communities. Governments and private organizations are expanding their fleets to enhance accessibility and responsiveness, particularly in underserved and remote regions. The growing burden of chronic illnesses, a rising aging population, and the increasing emphasis on preventive care are pushing authorities to invest in vehicles equipped with smart healthcare capabilities. Moreover, in the post-pandemic landscape, infection control and remote diagnostics have become core considerations, further fueling demand for specialty vehicles that align with modern healthcare standards. From high-tech ambulances to mobile clinics and fire-rescue units, the global market is witnessing a transformation driven by innovation, technology integration, and a broader shift toward decentralized care and public safety operations.

The demand for specialized vehicles continues to rise as investments pour into advanced emergency response systems, including next-generation ambulances and mobile healthcare units. Heightened awareness around public health, combined with a renewed push to deliver medical services to rural and hard-to-reach areas, is propelling the deployment of mobile ICU vans and paramedic vehicles. Infection control protocols and the growing adoption of telemedicine tools are further accelerating the demand for modern specialty vehicles across global markets. In parallel, the increasing frequency of natural disasters and climate-induced emergencies is driving nations to bolster their firefighting fleets and public safety vehicle infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $99.5 Billion |

| Forecast Value | $138.5 Billion |

| CAGR | 3.6% |

Ambulances accounted for a 40% share of the global market in 2024 and are projected to generate USD 45 billion by 2034. Governments and private healthcare operators are prioritizing shorter emergency response times and are outfitting vehicles with state-of-the-art communication systems, 5G connectivity, and real-time patient monitoring solutions. These innovations enable seamless hospital coordination and better patient outcomes during transport. As digital healthcare continues to evolve, smart ambulance technology is expected to play a critical role in next-gen emergency response strategies.

Law enforcement and public safety vehicles captured a 38% market share in 2024, fulfilling diverse roles from mobile diagnostic labs to treatment units in remote zones. As the healthcare delivery model becomes more decentralized, there is strong momentum behind mobile services offering diagnostics, outpatient care, and dialysis. These vehicles support home-based care delivery and enhance access in under-resourced areas, driving a new wave of innovation in specialty vehicle design.

Asia Pacific represented 30% of the global market in 2024, led by China's rapid infrastructure development and investment in smart mobility. Rising demand for ambulances, fire trucks, and utility vans in the region is backed by government incentives favoring clean, sustainable vehicle fleets.

Major players such as Farber Specialty Vehicles, Mercedes-Benz, Volvo, Isuzu, Traton, Pierce, REV, LDV, Oshkosh Corporation, and NFI are pushing the envelope through electrification, modular designs, and AI-powered diagnostics. Strategic collaborations with municipalities and healthcare providers are helping these companies strengthen local footprints and meet rising demand across regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Manufacturers

- 3.2.4 Service providers

- 3.2.5 Distributors

- 3.2.6 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade volume disruptions

- 3.3.2 Retaliatory measures

- 3.3.3 Impact on the industry

- 3.3.4 Supply-side impact

- 3.3.5 Demand-side impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Price trends

- 3.10 Cost breakdown analysis

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for emergency medical services across the globe

- 3.11.1.2 Increasing government investments in disaster response

- 3.11.1.3 Growing remote industrial activities

- 3.11.1.4 Surge in recreational travel

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial cost and long production lead times

- 3.11.2.2 Stringent regulatory and certification requirements

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter’s analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Ambulances

- 5.3 Fire extinguishing trucks

- 5.4 Mobile fuel carrying tankers

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.3.1 BEV

- 6.3.2 HEV

- 6.3.3 PHEV

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Medical & healthcare

- 7.3 Law enforcement & public safety

- 7.4 Recreational vehicles

- 7.5 Municipal services

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Arctic Cat

- 9.2 Cargotec

- 9.3 Case New Holland

- 9.4 Demers Ambulances

- 9.5 Eicher

- 9.6 Emergency One

- 9.7 Farber Specialty Vehicles

- 9.8 Hino Motors

- 9.9 Isuzu

- 9.10 LDV

- 9.11 Matthews Specialty Vehicles

- 9.12 Mercedes-Benz

- 9.13 NFI

- 9.14 Oshkosh Corporation

- 9.15 Pierce

- 9.16 REV

- 9.17 Rosenbauer International

- 9.18 Specialty Vehicles

- 9.19 Traton

- 9.20 Volvo

装甲巴士市场按防护等级、座位容量、动力类型、应用和销售管道,全球预测(2026-2032年)

装甲巴士市场按防护等级、座位容量、动力类型、应用和销售管道,全球预测(2026-2032年) 特种车辆:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)

特种车辆:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年) 2026-2034年全球特种商用车市场规模、份额、趋势和成长分析报告

2026-2034年全球特种商用车市场规模、份额、趋势和成长分析报告 专用车辆市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、车辆类型、地区和竞争细分,2020-2030 年)

专用车辆市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、车辆类型、地区和竞争细分,2020-2030 年) 专用车辆市场:依车辆类型和地区划分

专用车辆市场:依车辆类型和地区划分 全球专用车辆市场

全球专用车辆市场 特殊车辆的全球市场:各类型,各用途,推进系统,各地区,机会,预测,2018年~2032年

特殊车辆的全球市场:各类型,各用途,推进系统,各地区,机会,预测,2018年~2032年 2030 年特种车辆市场预测:按车辆类型、推进类型、应用和地区分類的全球分析

2030 年特种车辆市场预测:按车辆类型、推进类型、应用和地区分類的全球分析 特种车辆市场,按车辆类型、燃料类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

特种车辆市场,按车辆类型、燃料类型、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测 全球特种车辆市场:按类型、应用、推进领域、电池化学、最终用途产业、地区 - 预测(至 2030 年)

全球特种车辆市场:按类型、应用、推进领域、电池化学、最终用途产业、地区 - 预测(至 2030 年)