|

市场调查报告书

商品编码

1740754

混合动力电动滑板车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Hybrid E-Scooter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

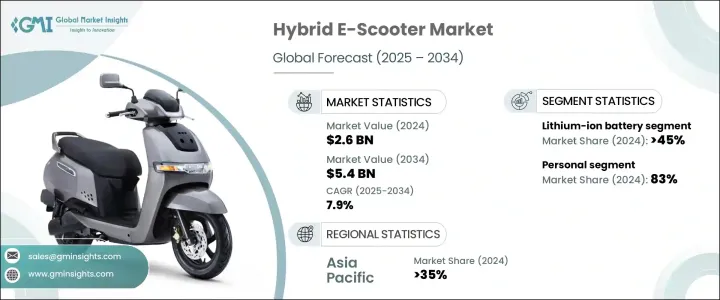

2024 年全球混合动力电动滑板车市场价值为 26 亿美元,预计到 2034 年将以 7.9% 的复合年增长率增长,达到 54 亿美元,这得益于电池技术的进步、电机效率的提高以及环保意识的增强。随着城市交通不断发展,越来越注重永续性和便利性,混合动力电动滑板车产业正在获得显着发展势头。随着城市交通日益拥堵,燃油价格持续波动,消费者正积极寻找更聪明、更环保的替代品,同时又不影响性能或续航里程。混合动力电动滑板车结合了电动和燃油技术,对于那些寻求延长出行距离而又不完全依赖充电基础设施的人来说,它正成为一种可靠的解决方案。这些双模滑板车为城市通勤者、送货人员以及追求高效、经济实惠和低碳足迹的日常用户提供了无与伦比的灵活性。

清洁交通领域投资的不断增加,加上政府对电动车的支持力度不断加大,正在塑造这个市场的未来。目前,许多州和联邦政府的政策都提供税收减免、激励措施和补贴,以减轻消费者和製造商的成本负担。与此同时,公共和私营部门的利益相关者正在加紧努力,打造一体化充电和加油基础设施,以支持混合动力出行。共享出行平台的成长以及最后一哩配送服务的日益普及,也在推动混合动力电动滑板车的销售方面发挥了关键作用。这一趋势在人口稠密的城市中心尤其明显,因为这些城市对快速、经济且符合排放标准的交通工具的需求很高。混合动力电动滑板车不仅是一种生活方式的升级,而且正迅速成为实现更智慧城市出行的策略工具。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 26亿美元 |

| 预测值 | 54亿美元 |

| 复合年增长率 | 7.9% |

混合动力电动滑板车的独特优势在于,它允许骑乘者在电动和燃油模式之间无缝切换。这种双重功能确保了更长的续航里程、更少的充电焦虑,并在交通拥堵区域提供更顺畅的骑乘体验。城市骑行者和零工经济工作者尤其被这些优势所吸引,因为他们需要低维护且高性能的车辆。锂离子电池的日益普及进一步刺激了这项需求。这些电池以其更高的能量密度、更快的充电时间和更长的使用寿命而闻名,显着提升了混合动力滑板车的实用性。其轻巧紧凑的设计改善了操控性并提升了能源效率,完美契合了现代通勤者的需求。

环境问题是另一个关键的成长动力。随着空气品质恶化和气候变迁加剧,世界各国政府正在实施更严格的排放标准,以遏制车辆污染。混合动力电动滑板车的排放量远低于纯汽油电动滑板车,正迅速成为注重环保的消费者的首选。这些滑板车满足了人们对清洁交通的需求,同时又不牺牲续航里程或动力,使其成为那些正在严厉打击高排放车辆的地区颇具吸引力的解决方案。越来越多的消费者选择混合动力电动滑板车作为中短途出行的经济实惠且环保的替代方案。

市场主要按电池类型细分,其中锂离子电池在2024年占据主导地位,创造10亿美元的收入。这类电池因其能源效率、耐用性和持续性能而备受青睐。它们将更大的能量融入更小、更轻的单元中,有助于提升整体续航里程并减轻车辆重量,从而提高燃油效率和机动性——这些特性对于城市道路行驶至关重要。

按最终用途划分,个人混合动力电动滑板车在2024年占据了83%的市场份额,占据了市场主导地位。都市化进程和对灵活通勤方式日益增长的需求,促使消费者寻求既经济高效又低排放的个人交通解决方案。这些滑板车短程行驶时提供电动辅助,长途行驶时提供燃油辅助,是日常城市出行的理想选择。与传统滑板车或汽车相比,它们更低的燃油和维护成本尤其受到注重预算的消费者的青睐。

2024年,亚太地区混合动力电动滑板车市场占据了35%的市场份额,这得益于该地区对两轮车的严重依赖以及人口密集的城市中心。随着交通拥堵日益加剧、停车位日益紧张,混合动力电动滑板车成为实用且环保的交通选择。中国凭藉其强大的本土製造能力、稳健的供应链以及优惠的政府法规,继续引领产业发展。

雅迪集团、雅马哈、光阳和小牛电动等主要参与者正在大力投资产品创新,扩大生产线,并强化分销管道。这些公司专注于打造节能、以用户为中心、功能先进的踏板车,以满足消费者日益增长的期望。与本地经销商和国际供应商建立策略合作伙伴关係,对于提升其全球市场份额并在竞争中保持领先地位至关重要。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件供应商

- 技术提供者

- 最终用途

- 利润率分析

- 川普政府关税的影响

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术与创新格局

- 专利分析

- 定价分析

- 地区

- 电池

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 配送和物流中的商业用途

- 里程焦虑和基础设施差距

- 环境法规和排放标准

- 电池和马达效率的技术进步

- 产业陷阱与挑战

- 初始成本高

- 维护问题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按电池,2021 - 2034 年

- 主要趋势

- 锂离子电池

- 铅酸电池

- 镍氢电池

- 固态电池

第六章:市场估计与预测:依航程容量,2021 年至 2034 年

- 主要趋势

- 短距离(15-30公里)

- 中距离(31-60公里)

- 长距离(60公里以上)

第七章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- 在线的

- 离线

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 个人的

- 商业的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Gogoro

- Green Tiger Mobility

- Honda

- Jiangsu Xinri E-Vehicle

- Kymco

- Meladath Auto Components

- NIU Technologies

- Okinawa Autotech

- Piaggio Group

- Sanyang Motor

- Silence Urban Ecomobility

- Sunra Electric Vehicle

- Verge Motors

- Yadea Group

- Yamaha

- Zhejiang Luyuan Electric Vehicle

The Global Hybrid E-Scooter Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 5.4 billion by 2034, driven by advancements in battery technology, improved motor efficiency, and rising environmental awareness. The hybrid e-scooter industry is gaining significant momentum as urban mobility continues to evolve with a strong focus on sustainability and convenience. With cities becoming more congested and fuel prices remaining volatile, consumers are actively looking for smarter, greener alternatives that do not compromise on performance or range. Hybrid e-scooters, which combine electric and fuel-powered technologies, are emerging as a reliable solution for individuals seeking extended travel distances without being entirely dependent on charging infrastructure. These dual-mode scooters provide unmatched flexibility for urban commuters, delivery personnel, and everyday users who demand efficiency, affordability, and a lower carbon footprint.

Rising investments in clean transportation, coupled with growing government support for electric mobility, are shaping the future of this market. Numerous state and federal policies now offer tax rebates, incentives, and subsidies that reduce the cost burden for consumers and manufacturers alike. At the same time, public and private stakeholders are ramping up efforts to create integrated charging and refueling infrastructure to support hybrid mobility. The growth of shared mobility platforms and the increasing adoption of last-mile delivery services have also played a pivotal role in driving hybrid e-scooter sales. This trend is particularly noticeable in densely populated urban hubs where quick, affordable, and emission-compliant transport is in high demand. Hybrid e-scooters are not just a lifestyle upgrade-they're fast becoming a strategic tool for achieving smarter urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 7.9% |

Hybrid e-scooters offer a distinct edge by allowing riders to switch seamlessly between electric and fuel modes. This dual functionality ensures a longer range, reduced charging anxiety, and a smoother riding experience in traffic-heavy zones. Urban riders and gig economy workers are especially drawn to these benefits, as they need vehicles that are low-maintenance yet high-performing. The rising use of lithium-ion batteries has further fueled the demand. Known for their higher energy density, faster charging time, and extended lifespan, these batteries significantly enhance the practicality of hybrid scooters. Their lightweight and compact design improves handling and boosts energy efficiency, aligning perfectly with the needs of modern-day commuters.

Environmental concerns are another key growth driver. As air quality worsens and climate change intensifies, governments worldwide are enforcing stricter emission norms to curb vehicular pollution. Hybrid e-scooters, which emit significantly less than their gasoline-only counterparts, are quickly becoming the go-to option for eco-conscious consumers. These scooters meet the demand for cleaner transport without compromising on range or power, making them an attractive solution in regions that are clamping down on high-emission vehicles. Consumers are increasingly choosing hybrid e-scooters as a cost-effective and environmentally friendly alternative for short to mid-range travel.

The market is primarily segmented by battery type, with lithium-ion batteries taking the lead in 2024, generating USD 1 billion in revenue. These batteries are favored for their energy efficiency, durability, and ability to deliver consistent performance. They pack more power into a smaller, lighter unit, helping boost the overall range and reducing the vehicle's weight, which in turn improves fuel efficiency and maneuverability-critical features for urban use.

By end-use, personal hybrid e-scooters dominated the market with an 83% share in 2024. Urbanization and rising demand for flexible commuting options are pushing consumers toward personal transport solutions that are both cost-efficient and low-emission. These scooters offer electric riding for short distances and fuel-powered assistance for longer routes, making them ideal for daily city travel. Budget-conscious consumers are especially drawn to them due to their lower fuel and maintenance costs compared to traditional scooters or cars.

The Asia Pacific Hybrid E-Scooter Market accounted for 35% share in 2024, thanks to the region's heavy reliance on two-wheelers and its densely populated urban centers. With increasing traffic congestion and limited parking availability, hybrid e-scooters present a highly practical and eco-friendly transport alternative. China, in particular, continues to lead the way due to its strong local manufacturing capabilities, robust supply chain, and favorable government regulations.

Key players such as Yadea Group, Yamaha, Kymco, and NIU Technologies are investing heavily in product innovation, expanding their production lines, and strengthening distribution channels. These companies focus on creating energy-efficient, user-centric scooters with advanced features, aiming to meet rising consumer expectations. Strategic partnerships with both local distributors and international suppliers are central to boosting their global market presence and staying ahead in the competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component suppliers

- 3.2.3 Technology providers

- 3.2.4 End-use

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Pricing analysis

- 3.7.1 Region

- 3.7.2 Battery

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Commercial use in delivery & logistics

- 3.10.1.2 Range anxiety & infrastructure gaps

- 3.10.1.3 Environmental regulations & emission norms

- 3.10.1.4 Technological advancements in battery and motor efficiency

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 Maintenance issues

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lithium-ion battery

- 5.3 Lead-acid batter

- 5.4 Nickel-metal hydride

- 5.5 Solid-state battery

Chapter 6 Market Estimates & Forecast, By Range Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short range (15-30 km)

- 6.3 Medium range (31-60 km)

- 6.4 Long range (above 60 km)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Online

- 7.3 Offline

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Personal

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Gogoro

- 10.2 Green Tiger Mobility

- 10.3 Honda

- 10.4 Jiangsu Xinri E-Vehicle

- 10.5 Kymco

- 10.6 Meladath Auto Components

- 10.7 NIU Technologies

- 10.8 Okinawa Autotech

- 10.9 Piaggio Group

- 10.10 Sanyang Motor

- 10.11 Silence Urban Ecomobility

- 10.12 Sunra Electric Vehicle

- 10.13 Verge Motors

- 10.14 Yadea Group

- 10.15 Yamaha

- 10.16 Zhejiang Luyuan Electric Vehicle

全球电动Scooter市场(按产品类型、电池类型、电池容量、马达功率和分销管道划分)—2025-2032 年全球预测电动Scooter和摩托车市场:2025-2030 年全球预测,按车辆类型、电池类型、马达类型、输出功率、每次充电的行驶里程、最终用户和分销管道划分电动摩托车市场(按摩托车、电池类型、驱动类型、功率容量、技术、充电范围、电压、最终用户和分销管道划分)—2025-2030 年全球预测

全球电动Scooter市场(按产品类型、电池类型、电池容量、马达功率和分销管道划分)—2025-2032 年全球预测电动Scooter和摩托车市场:2025-2030 年全球预测,按车辆类型、电池类型、马达类型、输出功率、每次充电的行驶里程、最终用户和分销管道划分电动摩托车市场(按摩托车、电池类型、驱动类型、功率容量、技术、充电范围、电压、最终用户和分销管道划分)—2025-2030 年全球预测 全球高性能电动摩托车市场全球电动Scooter升降机与托架市场

全球高性能电动摩托车市场全球电动Scooter升降机与托架市场 电动摩托车和踏板车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

电动摩托车和踏板车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球电动机车和Scooter市场:2025 年至 2030 年预测全球低功率电动机车和Scooter市场

全球电动机车和Scooter市场:2025 年至 2030 年预测全球低功率电动机车和Scooter市场 2025年电动Scooter共享全球市场报告全球电动机车和Scooter市场

2025年电动Scooter共享全球市场报告全球电动机车和Scooter市场