|

市场调查报告书

商品编码

1740777

汽车控制电缆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Control Cables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

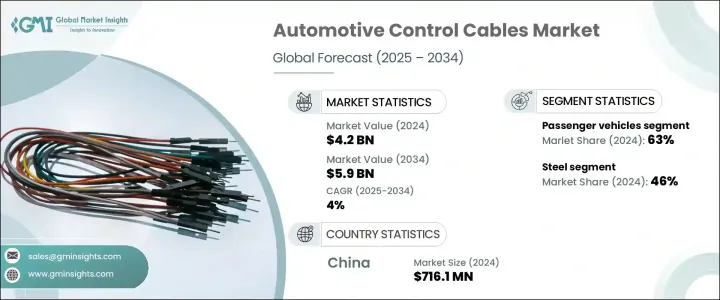

2024年,全球汽车控制拉索市场规模达42亿美元,预计到2034年将以4%的复合年增长率成长,达到59亿美元,这主要得益于汽车产量的成长,尤其是在亚太和拉丁美洲的新兴经济体。汽车控制拉索是车辆性能的重要组成部分,可确保离合器接合、煞车、换檔和油门控制的精确度。随着汽车产业的发展,对车辆效率、耐用性和使用者体验的高度重视持续推动拉索技术的创新。全球汽车产量正在迅速增长,尤其是在发展中地区,这些地区的经济状况改善和城市化进程推动了汽车销售的成长。同时,原始设备製造商正致力于透过先进的拉索系统来提高机械可靠性和反应能力。消费者对车辆安全性和性能的期望值不断提高,进一步刺激了对高品质控制拉索的需求。此外,全球日益严格的排放法规也促使汽车製造商优化车辆系统,包括控制拉索等机械零件,以提高能源效率。

产业向电动和混合动力汽车转型正在重塑控制电缆的应用。电动车 (EV) 虽然淘汰了内燃机中使用的一些传统机械部件,但也为控制电缆带来了全新且关键的应用。随着电动车设计日益复杂,控制电缆也需要进行调整以支援各种功能,例如暖通空调 (HVAC) 系统中的挡板控制和气流分配、电池仓通道装置、座椅移动以及充电介面控制。这些不断发展的应用案例为製造商带来了新的创新机会,使其能够满足新一代汽车的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 42亿美元 |

| 预测值 | 59亿美元 |

| 复合年增长率 | 4% |

在材料类型中,钢材继续主导汽车控制拉索市场,2024 年的市场份额为 46%。其卓越的耐用性、抗拉强度、成本效益和易于製造的特性使其成为离合器、煞车和油门应用的首选。即使业内人士正在探索铝或复合材料等更轻的材料以提高燃油经济性,钢材仍然因其在严苛条件下的韧性而不可或缺,尤其是在高性能和大众市场车型中。原始设备製造商和售后市场供应商青睐钢材,因为其价格实惠且供应广泛,确保了稳定的需求。

按车型划分,乘用车在市场中占据主导地位,2024 年占据 63% 的市场份额,并保持稳定成长趋势。这一领先地位反映了全球范围内紧凑型、中型和豪华汽车的高产量和消费者日益增长的需求。快速的城市化进程、不断增长的中产阶级收入以及印度和东南亚等国家汽车普及率的提高,是推动这一成长的主要因素。控制线在这些车辆中至关重要,它支援手动和自动功能,提升整体驾驶体验和安全性。

中国汽车控制电缆市场在2024年创造了7.161亿美元的市场规模,并有望在2034年占据39%的市场份额。中国强大的製造业基础、飙升的国内需求以及积极的电动车发展,正在巩固其领先地位。有利的政府政策和不断扩大的出口网路正在进一步推动汽车电缆系统的创新,巩固中国作为全球汽车控制电缆生产中心的地位。

全球汽车控制电缆市场的主要公司——Hi-Lex、矢崎、安波福、特瑞堡、Cablecraft Motion Controls、康斯伯格汽车、李尔、DURA Automotive Systems、泰科电子和古河电工——正更加重视拓展全球供应链,与原始设备製造商建立更深层的合作伙伴关係,投资于量化材料自动化。各公司也正在加强研发力度,以打造专为电动车和自动驾驶汽车系统量身订製的先进电缆解决方案。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件製造商

- 控制电缆组装商/製造商

- 一级汽车供应商

- 原始设备製造商 (OEM) 和售后市场分销商

- 利润率分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 其他国家的报復措施

- 对产业的影响

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 展望与未来考虑

- 对贸易的影响

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 全球乘用车和商用车产量不断增加

- 向电动车和混合动力车的转变

- 控制电缆定期维护和更换的必要性

- 电缆设计和材料的不断创新

- 产业陷阱与挑战

- 越来越多地转向线控驱动技术

- 严格且不断发展的环境法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按电缆,2021 - 2034 年

- 主要趋势

- 离合器线

- 加速器电缆

- 煞车线

- 变速线

- 手煞车线

- 油门线

- 其他的

第六章:市场估计与预测:依资料,2021 - 2034 年

- 主要趋势

- 钢

- PVC(聚氯乙烯)

- 尼龙

- 橡胶涂层

- 其他的

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 两轮车

- 商用车

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 引擎控制

- 传动控制

- 煞车系统

- 暖通空调系统

- 其他的

第九章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Aptiv

- Bergen Cable Technology

- Cablecraft Motion Controls

- Conwire

- DURA Automotive Systems

- Furukawa Electric

- Hi-Lex

- Kongsberg Automotive

- Kuster Holding

- Lear

- Lexco Cable

- Orscheln Products

- Sila Group

- Sumitomo Electric Industries

- Suprajit Engineering

- TE Connectivity

- Trelleborg

- Triumph Group

- Venus Industrial

- Yazaki

The Global Automotive Control Cables Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 5.9 billion by 2034, driven by rising vehicle production, particularly across emerging economies in Asia-Pacific and Latin America. Automotive control cables form a vital part of vehicular performance, ensuring precision in clutch engagement, braking, gear shifting, and throttle control. As the automotive sector evolves, a strong emphasis on vehicle efficiency, durability, and user experience continues to fuel innovation in cable technologies. Global automotive production is scaling up rapidly, especially in developing regions where improving economic conditions and urbanization drive automobile sales. Meanwhile, OEMs are focusing on enhancing mechanical reliability and responsiveness through advanced cable systems. Increasing consumer expectations around vehicle safety and performance further boosts demand for high-quality control cables. Additionally, stricter emissions regulations globally are pushing automakers to optimize vehicle systems, including mechanical components like control cables, to achieve better energy efficiency.

The industry's pivot to electric and hybrid vehicles is reshaping control cable applications. While electric vehicles (EVs) eliminate some traditional mechanical parts used in internal combustion engines, they introduce new and critical applications for control cables. As EV designs grow more complex, control cables are adapted to support various functions, such as flap control and air distribution in HVAC systems, battery compartment access mechanisms, seat movement, and charging interface controls. These evolving use cases are unlocking fresh opportunities for manufacturers to innovate and meet the demands of a new generation of vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 4% |

Among material types, steel continues to dominate the automotive control cables market, accounting for a 46% share in 2024. Its exceptional durability, tensile strength, cost-efficiency, and manufacturing ease make it the preferred choice for clutch, brake, and throttle applications. Even as industry players explore lighter materials like aluminum or composites to boost fuel economy, steel remains indispensable for its resilience under demanding conditions, especially in high-performance and mass-market models. OEMs and aftermarket suppliers favor steel for its affordability and widespread availability, ensuring a steady demand.

Passenger vehicles lead the market by vehicle type, securing a 63% share in 2024 and maintaining a steady growth trend. This leadership reflects high production volumes and a surging consumer appetite for compact, mid-size, and luxury vehicles worldwide. Rapid urbanization, expanding middle-class income, and better automotive access in countries like India and throughout Southeast Asia are major factors fueling this growth. Control cables are essential across these vehicles for supporting both manual and automated functions, enhancing the overall driving experience and safety.

China Automotive Control Cables Market generated USD 716.1 million in 2024 and captured a commanding 39% share through 2034. The country's strong manufacturing base, soaring domestic demand, and aggressive EV push are strengthening its leadership. Favorable government policies and an expanding export network are further propelling innovation in automotive cable systems, solidifying China's role as a global hub for automotive control cable production.

Key companies operating in the Global Automotive Control Cables Market-Hi-Lex, Yazaki, Aptiv, Trelleborg, Cablecraft Motion Controls, Kongsberg Automotive, Lear, DURA Automotive Systems, TE Connectivity, and Furukawa Electric-are sharpening their focus on expanding global supply chains, forging deeper partnerships with OEMs, investing in lightweight material technologies, and automating manufacturing processes. Companies are also ramping up R&D efforts to engineer advanced cable solutions tailored for EVs and autonomous vehicle systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Control cable assemblers/manufacturers

- 3.2.4 Tier 1 automotive suppliers

- 3.2.5 Original equipment manufacturers (OEMs) & aftermarket distributors

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Increasing global production of passenger and commercial vehicles

- 3.9.1.2 The shift toward EVs and hybrid vehicles

- 3.9.1.3 The need for regular maintenance and replacement of control cables

- 3.9.1.4 Continuous innovation in cable design and materials

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Increasing shift towards drive-by-wire technology

- 3.9.2.2 Stringent and evolving environmental regulations

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Cable, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Clutch cables

- 5.3 Accelerator cables

- 5.4 Brake cables

- 5.5 Gear shift cables

- 5.6 Handbrake cables

- 5.7 Throttle cables

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 PVC (Polyvinyl Chloride)

- 6.4 Nylon

- 6.5 Rubber coated

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Two-wheelers

- 7.4 Commercial vehicles

- 7.4.1 Light Commercial Vehicles (LCV)

- 7.4.2 Medium Commercial Vehicles (MCV)

- 7.4.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Engine control

- 8.3 Transmission control

- 8.4 Braking system

- 8.5 HVAC system

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bergen Cable Technology

- 11.3 Cablecraft Motion Controls

- 11.4 Conwire

- 11.5 DURA Automotive Systems

- 11.6 Furukawa Electric

- 11.7 Hi-Lex

- 11.8 Kongsberg Automotive

- 11.9 Kuster Holding

- 11.10 Lear

- 11.11 Lexco Cable

- 11.12 Orscheln Products

- 11.13 Sila Group

- 11.14 Sumitomo Electric Industries

- 11.15 Suprajit Engineering

- 11.16 TE Connectivity

- 11.17 Trelleborg

- 11.18 Triumph Group

- 11.19 Venus Industrial

- 11.20 Yazaki

高压汽车市场:按组件类型、推进系统、车辆类型、应用、应用领域和最终用户划分-2026年至2032年全球预测

高压汽车市场:按组件类型、推进系统、车辆类型、应用、应用领域和最终用户划分-2026年至2032年全球预测 2026年全球汽车电缆市场报告2026年全球高清多媒体介面(HDMI)汽车线市场报告

2026年全球汽车电缆市场报告2026年全球高清多媒体介面(HDMI)汽车线市场报告 中重型商用车点火电缆市场-全球产业规模、份额、趋势、机会及预测(依燃料类型、需求类别、地区及竞争格局划分,2021-2031年)乘用车点火电缆市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)摩托车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)汽车油门拉索市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、销售管道类型、地区和竞争格局划分,2021-2031年汽车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、燃料类型、需求类别、地区和竞争格局划分,2021-2031年)单端线市场按连接器类型、线材长度、绝缘材料、应用和分销通路划分-2026年至2032年全球预测汽车高压直流继电器市场:按继电器类型、接点配置、线圈电压和应用划分-2026年至2032年全球预测

中重型商用车点火电缆市场-全球产业规模、份额、趋势、机会及预测(依燃料类型、需求类别、地区及竞争格局划分,2021-2031年)乘用车点火电缆市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)摩托车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按燃料类型、需求类别、地区和竞争格局划分,2021-2031年)汽车油门拉索市场 - 全球产业规模、份额、趋势、机会、预测:按类型、车辆类型、销售管道类型、地区和竞争格局划分,2021-2031年汽车点火线市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、燃料类型、需求类别、地区和竞争格局划分,2021-2031年)单端线市场按连接器类型、线材长度、绝缘材料、应用和分销通路划分-2026年至2032年全球预测汽车高压直流继电器市场:按继电器类型、接点配置、线圈电压和应用划分-2026年至2032年全球预测