|

市场调查报告书

商品编码

1740787

健康与卫生包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Health and Hygiene Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

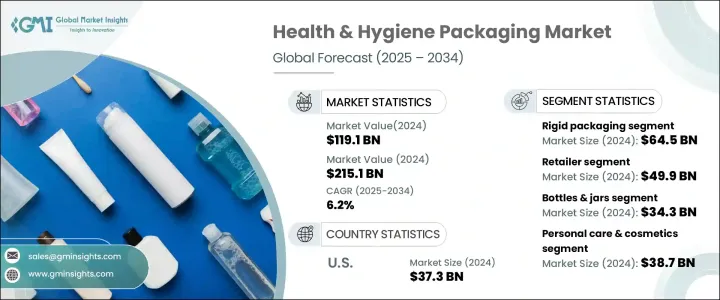

2024 年全球健康与卫生包装市场价值为 1,191 亿美元,预计到 2034 年将以 6.2% 的强劲复合年增长率成长,达到 2,151 亿美元。这一增长主要源于个人护理和卫生产品需求的不断增长、安全法规的日益严格以及消费者对优质和可持续包装的日益偏好。随着个人护理行业变得更加复杂和规范化,包装解决方案必须不断发展以满足功能性和合规性要求。注重健康的消费者正在推动向提供安全性、便利性和环境责任的包装转变。随着永续性成为主要关注点,品牌正在采用环保设计和材料,确保包装行业拥有更绿色的未来。包装设计和材料科学的创新预计将进一步推动市场成长,公司将投资技术以满足消费者对更安全、更永续包装的需求。

原料成本上涨对健康和卫生包装产业构成重大挑战,尤其是因为进口塑胶材料、薄膜和机械设备被征收关税。这些关税推高了成本结构,製造商面临着在价格上涨和维持获利之间取得平衡的压力。为此,许多公司正在重新思考其供应链策略,投资自动化,并转向本地采购,以减轻关税的影响。这些变化预计将重塑营运模式,确保公司在面临财务压力的情况下仍能保持竞争力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1191亿美元 |

| 预测值 | 2151亿美元 |

| 复合年增长率 | 6.2% |

硬质包装持续占据市场主导地位,2024 年市场规模将达到 645 亿美元。其在个人护理、医疗级和保健产品中的广泛应用归功于其耐用性、卓越的阻隔保护和高端吸引力。瓶装、罐装和泵式包装等硬质包装不仅能够提供结构完整性,还能延长产品保质期并增强防篡改性能,这在对卫生和安全标准要求极高的行业中至关重要。此外,硬质包装凭藉其客製化形状、表面处理和标籤,能够提供强大的品牌推广机会,使其成为高端保健产品的首选。

零售仍然是主要的配销通路,2024 年市场价值将达到 499 亿美元。店内销售模式透过醒目的包装、便利的货架设计和多件装优惠,使产品脱颖而出,满足了追求便利性的消费者的需求。零售商越来越重视经济高效、易于备货且外观精美的包装,以激发衝动购买,并提升品牌在实体零售环境中的知名度。

2024年,美国健康与卫生包装市场规模达373亿美元,这得益于消费者对清洁度日益重视、人口老化以及个人保健产品需求的上升等多种因素。美国品牌正在创新抗菌涂层、可回收材料和防篡改密封,以满足不断变化的消费者偏好和监管要求。

全球健康与卫生包装市场的关键参与者包括 Quadpack、Alpla Group、DS Smith、Napco National、Amcor Plc、Huhtamaki、Rieke Packaging、Glenroy、JohnsByrne、Ball Corporation、Stora Enso、Crown Holdings, Inc.、Constan下来 flexibles、Greiner Packaging Global Gmbn、Bet 和 Aterry。为了巩固市场地位,各公司正专注于永续材料创新、区域製造中心和包装生产线自动化。随着品牌致力于实现环保目标,对可回收和可生物降解包装解决方案的投资正在增加。此外,与医疗保健和个人护理品牌的策略合作伙伴关係正在促进客製化的高性能包装解决方案。数位设计工具和智慧包装技术的整合正在促进消费者互动并提高供应链透明度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 一次性包装和抗菌包装的需求不断增长

- 医疗保健和製药业的成长

- 人口老化和慢性病盛行率上升

- 可支配所得增加和都市化

- 法规遵从性和严格的安全标准

- 产业陷阱与挑战

- 先进且可持续的包装成本高昂

- 仿冒和劣质包装替代品

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 薄膜和片材

- 包包和小袋

- 罐头

- 小袋

- 瓶子和罐子

- 管

- 盒子和纸箱

- 其他的

第六章:市场估计与预测:依包装类型,2021-2034

- 主要趋势

- 硬质包装

- 软包装

第七章:市场估计与预测:按配销通路,2021-2034

- 主要趋势

- 零售商

- 在线的

- 直销

- 其他的

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 营养保健品和食品补充剂

- 个人护理和化妆品

- 功能性/保健饮料

- 医疗保健

- 居家护理和盥洗用品

- 其他的

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Alpla Group

- Amcor Plc

- Amerplast Ltd.

- Ball Corporation

- Berry Global

- Constantia Flexibles

- Crown Holdings, Inc.

- DS Smith

- Glenroy

- Greiner Packaging GmbH

- Huhtamaki

- JohnsByrne

- Napco National

- Quadpack

- Rieke Packaging

- Sonoco Products Company

- Stora Enso

The Global Health and Hygiene Packaging Market was valued at USD 119.1 billion in 2024 and is estimated to grow at a robust CAGR of 6.2% to reach USD 215.1 billion by 2034. This growth is primarily driven by the rising demand for personal care and hygiene products, stricter safety regulations, and an increasing consumer preference for premium and sustainable packaging.and As the personal care industry becomes more sophisticated and regulated, packaging solutions must evolve to meet both functional and compliance requirements. Health-conscious consumers are driving the shift toward packaging that offers safety, convenience, and environmental responsibility. With sustainability becoming a major focus, brands are incorporating eco-friendly designs and materials, ensuring a greener future for the packaging industry. Innovations in packaging design and material science are expected to further propel market growth, with companies investing in technology to meet consumer demands for safer, more sustainable packaging.

The rising cost of raw materials is a significant challenge for the health and hygiene packaging sector, particularly due to tariffs on imported plastic materials, films, and machinery. These tariffs are pushing up the cost structure, and manufacturers are feeling the pressure to balance price hikes with the need to maintain profitability. In response, many companies are rethinking their supply chain strategies, investing in automation, and shifting towards local sourcing to mitigate the effects of these tariffs. Such changes are anticipated to reshape operational models, ensuring companies remain competitive despite the financial pressures.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $119.1 Billion |

| Forecast Value | $215.1 Billion |

| CAGR | 6.2% |

Rigid packaging continues to dominate the market, accounting for USD 64.5 billion in 2024. Its widespread use in personal care, medical-grade, and wellness products is attributed to its durability, excellent barrier protection, and premium appeal. Rigid packaging options, such as bottles, jars, and pump dispensers, not only provide structural integrity but also enhance product shelf life and tamper resistance, which are crucial in sectors demanding high hygiene and safety standards. Furthermore, rigid packaging enables strong branding opportunities with custom shapes, finishes, and labels, making it a preferred choice for premium health and wellness products.

Retail remains the leading distribution channel, contributing USD 49.9 billion in market value in 2024. In-store formats allow products to stand out through eye-catching packaging, shelf-ready designs, and multi-pack offers, catering to convenience-driven consumers. Retailers are increasingly prioritizing cost-effective, easy-to-stock, and visually appealing packaging that can drive impulse purchases and elevate brand visibility in physical retail environments.

The U.S. Health and Hygiene Packaging Market generated USD 37.3 billion in 2024, driven by multiple factors such as the growing emphasis on cleanliness, an aging population, and a rise in personal wellness products. U.S. brands are innovating with antimicrobial coatings, recyclable materials, and tamper-evident seals to meet evolving consumer preferences and regulatory requirements.

Key players in the Global Health and Hygiene Packaging Market include Quadpack, Alpla Group, DS Smith, Napco National, Amcor Plc, Huhtamaki, Rieke Packaging, Glenroy, JohnsByrne, Ball Corporation, Stora Enso, Crown Holdings, Inc., Constantia Flexibles, Greiner Packaging GmbH, Berry Global, Sonoco Products Company, and Amerplast Ltd. To strengthen their market position, companies are focusing on sustainable material innovations, regional manufacturing hubs, and automation in packaging lines. Investments in recyclable and biodegradable packaging solutions are rising as brands aim to meet environmental goals. Furthermore, strategic partnerships with healthcare and personal care brands are fostering tailored, high-performance packaging solutions. The integration of digital design tools and smart packaging technologies is boosting consumer interaction and enhancing supply chain transparency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for single-use and antimicrobial packaging

- 3.3.1.2 Growth in the healthcare and pharmaceutical sectors

- 3.3.1.3 Aging population and growing chronic disease prevalence

- 3.3.1.4 Rising disposable income and urbanization

- 3.3.1.5 Regulatory compliance and stringent safety standards

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of advanced and sustainable packaging

- 3.3.2.2 Counterfeit and low-quality packaging alternatives

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Films & sheets

- 5.3 Bags & pouches

- 5.4 Cans

- 5.5 Sachets

- 5.6 Bottles & jars

- 5.7 Tubes

- 5.8 Boxes & cartons

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Rigid packaging

- 6.3 Flexible packaging

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Retailers

- 7.3 Online

- 7.4 Direct sales

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Nutraceuticals & food supplements

- 8.3 Personal care & cosmetics

- 8.4 Functional/health beverage

- 8.5 Medical & healthcare

- 8.6 Home care & toiletries

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alpla Group

- 10.2 Amcor Plc

- 10.3 Amerplast Ltd.

- 10.4 Ball Corporation

- 10.5 Berry Global

- 10.6 Constantia Flexibles

- 10.7 Crown Holdings, Inc.

- 10.8 DS Smith

- 10.9 Glenroy

- 10.10 Greiner Packaging GmbH

- 10.11 Huhtamaki

- 10.12 JohnsByrne

- 10.13 Napco National

- 10.14 Quadpack

- 10.15 Rieke Packaging

- 10.16 Sonoco Products Company

- 10.17 Stora Enso