|

市场调查报告书

商品编码

1740803

无水染色技术市场机会、成长动力、产业趋势分析及2025-2034年预测Waterless Dyeing Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

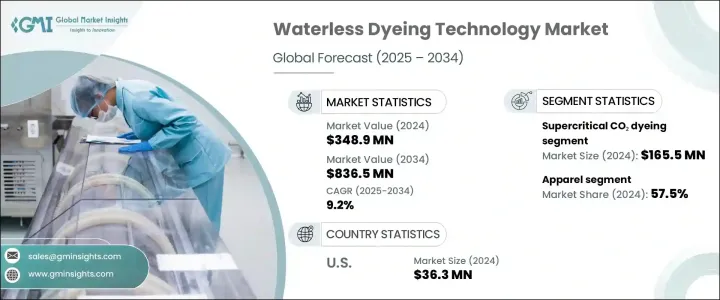

2024年,全球无水染色技术市场规模达3.489亿美元,预计2034年将以9.2%的复合年增长率成长至8.365亿美元。这项技术之所以受到广泛关注,与其环保特性密切相关,尤其是在以耗水量大、污染严重着称的纺织业。传统的纺织染色方法由于大量使用淡水并产生有毒废水,仍然是资源消耗最大、环境破坏最严重的方法之一。随着全球对水资源短缺、污染以及气候变迁更广泛影响的担忧日益加剧,纺织业正被迫转向更永续的替代方案。无水染色技术提供了一个前瞻性的解决方案,它不仅有助于减少环境影响,还能满足消费者和监管机构对清洁生产方法日益增长的需求。开发纺织製造业的清洁技术正成为一项策略要务。能够消除或大幅减少染色过程中用水量的创新技术正获得显着发展。为了应对日益增强的全球意识和监管压力,製造商正在采取更永续的做法,以降低排放、提高效率并减少水足迹。

无水染色技术市场按技术类型细分为超临界 CO2 染色、空气染色等。其中,超临界 CO2 染色占据主导地位,2024 年的市值为 1.655 亿美元,预计在预测期内的复合年增长率约为 9.9%。这种方法的特点是无需使用水或刺激性化学物质即可将染料带入纤维。它使用超临界状态的二氧化碳,可实现深层纤维渗透和有效颜色吸收。其吸引力在于其环保性、高染料吸收率、更低的能耗和二氧化碳的可回收性,这项工艺显着减少了废水排放并简化了染色操作。随着品牌致力于达到永续发展基准并减少其环境足迹,该技术正越来越多地被采用。随着企业追求符合绿色倡议的更有效率的製造流程,对先进染色系统的需求持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.489亿美元 |

| 预测值 | 8.365亿美元 |

| 复合年增长率 | 9.2% |

从应用角度来看,市场分为服装、家纺、工业用纺织品和技术用纺织品。服装领域占57.5%的市场份额,占据主导地位,预计2025年至2034年的复合年增长率为9.5%。时尚产业对环保生产的需求在这一成长中发挥关键作用。鑑于服装用纺织品的产量庞大以及减少污染的迫切性,无水染色是可行且有效的解决方案。时尚产业经常因其对环境的影响而受到批评,目前正积极寻求能够在其生产过程中减少用水量并减少有害物质含量的技术。以替代溶剂取代水或采用非液体方法的染色技术正日益受到青睐,尤其是在服装製造业。

依纤维类型细分,市场包括棉、聚酯纤维、尼龙、黏胶纤维、亚麻等。聚酯纤维在2024年成为主导纤维类型,预计在整个预测期内将保持领先地位。聚酯纤维以其价格实惠、弹性好和用途广泛而闻名,无水染色工艺将带来巨大优势。传统的聚酯染色需要高温、大量的水和各种有害物质。相较之下,无水染色——尤其是使用超临界二氧化碳——可有效渗透染料分子,提高色牢度,并最大限度地减少化学品用量。这些优势使其特别适合现代纺织製造流程。

从地区来看,美国在北美市场处于领先地位,2024 年估值达 3,630 万美元,预计预测期内复合年增长率将达到 9.8%。这一增长主要得益于日益严格的环境法规以及传统纺织染色製程的改革。随着永续性成为纺织政策的核心内容,製造商面临越来越大的压力,需要采用减少用水量、减少排放并遵守更严格标准的解决方案。这促使全国的纺织业转向更清洁的技术和循环经济模式。

无水染色技术产业正透过超临界二氧化碳染色和等离子处理等创新技术不断发展,这些技术减少了用水量和有毒废物的产生。 DyeCO2 等领先公司正在推动环保解决方案,以降低废水处理成本。随着产业向循环经济实践转型,节能模组化染色、可回收材料和碳中和等趋势日益显现。日益增长的道德时尚需求、更严格的法规以及加强的合作正在加速永续实践的实施,并推动整个纺织供应链采用无水染色技术。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(销售价格)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 供应商格局

- 交易分析

- 利润率分析

- 技术概述

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 环境永续性议题

- 监管压力和合规性

- 消费者对永续产品的需求

- 全球伙伴关係和产业合作

- 产业陷阱与挑战

- 初始资本投入高

- 织物相容性有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依技术类型,2021 - 2034 年

- 主要趋势

- 超临界CO2染色

- 空气染色

- 其他的

第六章:市场估计与预测:依纤维类型,2021 - 2034 年

- 主要趋势

- 棉布

- 聚酯纤维

- 尼龙

- 黏胶纤维

- 亚麻布

- 其他的

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 服饰

- 家纺

- 工业纺织品

- 技术纺织品

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 纺织品製造商

- 时尚品牌

- 化学品和染料生产商

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直接的

- 间接

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- AirDye

- Alchemie Technology

- Archroma

- Deven Supercriticals Pvt. Ltd

- DMS Dilmenler Makina ve Tekstil San. Tic. AS.

- DyeCoo

- eCO2Dye

- Guangdong Exponent Envirotech Ltd.

- HISAKA WORKS, LTD

- Kingfull Machinery CO2 Ltd

- Kornit Digital

- NTX

- Shanghai Singularity Imp&exp Company Limited

- Twine Solutions

- Xefco Pty Ltd

The Global Waterless Dyeing Technology Market was valued at USD 348.9 million in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 836.5 million by 2034. The surge in interest surrounding this technology is strongly linked to its environmentally conscious attributes, especially in an industry notorious for its excessive water consumption and pollution. Conventional textile dyeing methods continue to be among the most resource-intensive and environmentally damaging due to the heavy use of freshwater and the toxic wastewater they produce. As global concerns over water scarcity, pollution, and the broader implications of climate change intensify, the textile industry is being pushed to shift toward more sustainable alternatives. Waterless dyeing technology offers a forward-looking solution that not only helps reduce environmental impact but also meets the growing demand from both consumers and regulators for cleaner production methods. The development of cleaner technologies in textile manufacturing is becoming a strategic imperative. Innovations that eliminate or drastically reduce the need for water during dyeing are gaining significant traction. In response to increasing global awareness and regulatory pressure, manufacturers are embracing more sustainable practices that promise lower emissions, higher efficiency, and reduced water footprints.

The waterless dyeing technology market is segmented by technology type into supercritical CO2 dyeing, air dyeing, and others. Among these, supercritical CO2 dyeing dominated the segment with a market value of USD 165.5 million in 2024 and is expected to grow at a CAGR of approximately 9.9% during the forecast period. This method stands out for its ability to carry dyes into fibers without using water or harsh chemicals. It employs carbon dioxide in its supercritical state, which allows for deep fiber penetration and efficient color absorption. The appeal lies in its eco-friendly nature, high dye uptake, lower energy use, and recyclability of CO2 ,This process significantly cuts down on wastewater discharge and streamlines dyeing operations. The technology is increasingly being adopted as brands aim to meet sustainability benchmarks and reduce their environmental footprints. As companies aim for more efficient manufacturing processes that align with green initiatives, the demand for advanced dyeing systems continues to grow.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $348.9 Million |

| Forecast Value | $836.5 Million |

| CAGR | 9.2% |

In terms of application, the market is divided into apparel, home textiles, industrial textiles, and technical textiles. The apparel segment led the market with a 57.5% share and is projected to grow at a CAGR of 9.5% from 2025 to 2034. The need for eco-conscious production in the fashion sector is playing a key role in this growth. Given the massive volume of textiles produced for clothing and the urgency to reduce pollution, waterless dyeing presents a viable and impactful solution. The fashion industry, often criticized for its environmental impact, is now actively seeking technologies that eliminate the use of water and reduce the presence of hazardous substances in its processes. Dyeing techniques that replace water with alternative solvents or rely on non-liquid approaches are gaining preference, particularly in apparel manufacturing.

When segmented by fiber type, the market includes cotton, polyester, nylon, viscose, linen, and others. Polyester emerged as the dominant fiber type in 2024 and is expected to maintain its leading position throughout the forecast period. Known for its affordability, resilience, and widespread usage, polyester benefits immensely from waterless dyeing methods. Traditional polyester dyeing requires high temperatures, large volumes of water, and various harmful substances. In contrast, waterless dyeing-especially using supercritical CO2-allows for efficient penetration of dye molecules, better color fastness, and minimal chemical usage. These advantages make it particularly well-suited for modern textile manufacturing processes.

Regionally, the United States led the North American market with a valuation of USD 36.3 million in 2024 and is anticipated to grow at a CAGR of 9.8% during the forecast period. This growth is largely driven by mounting environmental regulations and efforts to reform conventional textile dyeing practices. As sustainability becomes a core aspect of textile policies, manufacturers are under increasing pressure to adopt solutions that reduce water usage, minimize emissions, and comply with stricter standards. This has encouraged a nationwide shift toward cleaner technologies and a circular economy approach within the textile sector.

The waterless dyeing technology industry is advancing through innovations like supercritical CO2 dyeing and plasma treatments, which reduce water usage and toxic waste. Leading companies such as DyeCO2 drive eco-friendly solutions that cut wastewater treatment costs. As the industry shifts toward circular economy practices, trends include energy-efficient modular dyeing, recyclable materials, and carbon neutrality. Growing ethical fashion demand, stricter regulations, and enhanced collaboration are accelerating sustainable practices and boosting adoption of waterless dyeing technologies across the textile supply chain.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-Side impact (Raw Materials)

- 3.2.2.2 Price volatility in key materials

- 3.2.2.3 Supply chain restructuring

- 3.2.2.4 Production cost implications

- 3.2.2.5 Demand-Side impact (Selling Price)

- 3.2.2.6 Price transmission to end markets

- 3.2.2.7 Market share dynamics

- 3.2.2.8 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Trade analysis

- 3.5 Profit margin analysis

- 3.6 Technological overview

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Environmental sustainability concerns

- 3.9.1.2 Regulatory pressures and compliance

- 3.9.1.3 Consumer demand for sustainable products

- 3.9.1.4 Global partnerships & industry collaboration

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial capital investment

- 3.9.2.2 Limited fabric compatibility

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Technology Type, 2021 - 2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Supercritical CO2 dyeing

- 5.3 Air dyeing

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Fiber Type, 2021 - 2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Cotton

- 6.3 Polyester

- 6.4 Nylon

- 6.5 Viscose

- 6.6 Linen

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Apparel

- 7.3 Home textiles

- 7.4 Industrial textiles

- 7.5 Technical textiles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Textile manufacturers

- 8.3 Fashion brands

- 8.4 Chemical & dye producers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AirDye

- 11.2 Alchemie Technology

- 11.3 Archroma

- 11.4 Deven Supercriticals Pvt. Ltd

- 11.5 DMS Dilmenler Makina ve Tekstil San. Tic. A.S..

- 11.6 DyeCoo

- 11.7 eCO2Dye

- 11.8 Guangdong Exponent Envirotech Ltd.

- 11.9 HISAKA WORKS, LTD

- 11.10 Kingfull Machinery CO2 Ltd

- 11.11 Kornit Digital

- 11.12 NTX

- 11.13 Shanghai Singularity Imp&exp Company Limited

- 11.14 Twine Solutions

- 11.15 Xefco Pty Ltd