|

市场调查报告书

商品编码

1740832

发电厂控制系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Power Plant Control System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

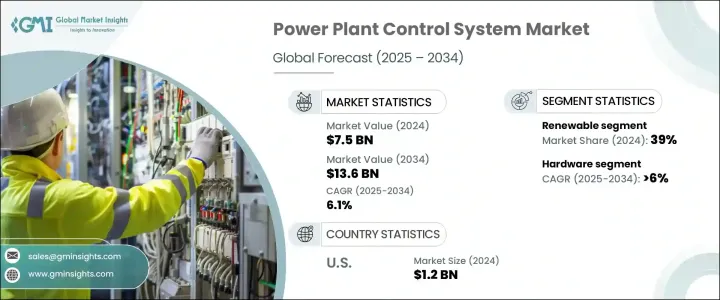

2024年,全球发电厂控制系统市场规模达75亿美元,预计到2034年将以6.1%的复合年增长率成长,达到136亿美元,这得益于能源产业快速迈向更智慧、更有效率的发电方式。随着世界面临着日益增长的能源基础设施现代化和向清洁能源转型的压力,控制系统在重新定义工厂运作方式方面发挥核心作用。电网正变得更加动态化,公用事业公司正在加大对智慧控制技术的投资,这些技术能够提供即时效能监控、无缝电网整合和增强的可靠性。随着再生能源和分散式发电的日益普及,对灵活、智慧自动化解决方案的需求比以往任何时候都更加强烈。老化的基础设施、不断增长的能源需求以及全球对碳中和的追求,正在推动控制平台的升级和更换浪潮。产业参与者正在利用数位孪生、预测分析和人工智慧解决方案来简化营运、最大限度地减少停机时间并提高营运效率。政府支持电网现代化、能源安全和减排目标的政策进一步增强了全球控制系统创新的势头。

随着网路安全问题日益严重,发电厂控制系统如今正采用内建安全协定、弹性通讯网路和先进的自动化框架进行设计。人工智慧、机器学习和即时诊断等技术正在重塑工厂的流程监控和管理方式,使营运更快、更安全、更可靠。预测性维护工具和先进的故障检测机制正在帮助公用事业公司减少计划外停机并提高工厂整体性能。随着全球製造商和政府机构将资源投入下一代自动化领域,可程式逻辑控制器 (PLC)、分散式控制系统 (DCS) 和 SCADA 平台正成为现代能源生态系统的支柱,推动能源效率的提升、负载优化和人工干预的减少。推动再生能源整合和碳中和营运的监管要求正促使公用事业公司彻底改造老化的控制系统,转而采用模组化、可扩展且适应性强的解决方案。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 75亿美元 |

| 预测值 | 136亿美元 |

| 复合年增长率 | 6.1% |

预计硬体市场将保持强劲成长,到2034年复合年增长率将达到6%。火力发电和核电设施的持续升级,以及新电厂的投产,正在推动对符合不断演变的监管标准的精密控制硬体的需求。天然气发电厂也高度依赖整合控制系统来管理涡轮机、优化负载响应并控制排放,尤其是在联合循环电厂加速部署的情况下。

到2034年,天然气发电厂控制系统市场可望以6%的复合年增长率成长,这得益于联合循环电厂的日益普及。联合循环电厂将燃气涡轮机和蒸汽涡轮机配对,以最大限度地提高效率并降低碳排放。这些先进的设施需要高效能的控制解决方案,能够管理从燃烧调节到热回收和排放控制等复杂的操作,确保在动态负载条件下保持最佳性能。天然气作为过渡燃料的日益普及,进一步推动了主要市场的基础设施投资。

2024年,美国发电厂控制系统市场规模达12亿美元,这得益于美国大力推动老化电网的现代化改造。分散式能源、再生能源发电的激增以及对智慧电网的需求,正推动联邦和州两级对先进自动化和即时控制技术进行大量投资。

全球发电厂控制系统市场的主要参与者包括ABB、西门子能源、施耐德电气、三菱重工、艾默生电气、罗克韦尔自动化、横河电机、日立能源、通用电气Vernova、WAGO等。各公司专注于持续创新、人工智慧驱动的自动化以及与公用事业公司建立策略合作伙伴关係,以扩大其市场份额。模组化设计、增强型HMI介面、强大的网路安全功能、远端诊断和全生命週期服务对于供应商保持竞争力并满足不断变化的市场需求至关重要。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依组件划分,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第六章:市场规模及预测:依解决方案,2021 - 2034 年

- 主要趋势

- 监控与资料采集 (SCADA)

- 分散式控制系统(DCS)

- 可程式逻辑控制器(PLC)

- 工厂资产管理(PAM)

- 工厂生命週期管理 (PLM)

第七章:市场规模及预测:依工厂类型,2021 - 2034

- 主要趋势

- 煤炭

- 天然气

- 核

- 水力发电

- 再生能源

第八章:市场规模及预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- ABB

- Bachmann electronic

- Emerson Electric

- GE Vernova

- Hitachi Energy

- Ingeteam

- Meteocontrol

- Mitsubishi Heavy Industries

- Motorola Solutions

- Nexus Integra

- OMRON Corporation

- Petrotech

- Rockwell Automation

- Schneider Electric

- Siemens Energy

- Toshiba Energy Systems & Solutions Corporation

- Valmet

- WAGO

- Yokogawa

The Global Power Plant Control System Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 13.6 billion by 2034, fueled by the energy sector's rapid move toward smarter, more efficient power generation. As the world faces mounting pressure to modernize energy infrastructure and transition toward cleaner power, control systems are playing a central role in redefining how plants operate. Power grids are becoming more dynamic, and utilities are stepping up investments in smart control technologies that deliver real-time performance monitoring, seamless grid integration, and enhanced reliability. With the growing adoption of renewable energy sources and decentralized generation, the need for flexible, intelligent automation solutions is stronger than ever. Aging infrastructure, rising energy demands, and the global push for carbon neutrality are driving a steady wave of upgrades and replacements in control platforms. Industry players are leveraging digital twins, predictive analytics, and AI-powered solutions to streamline operations, minimize downtime, and boost operational efficiency. Government policies supporting grid modernization, energy security, and emission reduction targets are further intensifying the momentum for control system innovation across the global landscape.

With cybersecurity concerns rising, power plant control systems are now being designed with built-in security protocols, resilient communication networks, and advanced automation frameworks. Technologies such as artificial intelligence, machine learning, and real-time diagnostics are reshaping how plants monitor and manage processes, making operations faster, safer, and more reliable. Predictive maintenance tools and advanced fault detection mechanisms are helping utilities reduce unplanned outages and improve overall plant performance. As global manufacturers and government bodies pour resources into next-generation automation, programmable logic controllers (PLC), distributed control systems (DCS), and SCADA platforms are becoming the backbone of modern energy ecosystems, driving gains in energy efficiency, load optimization, and reduced manual interventions. Regulatory mandates promoting renewable energy integration and carbon-neutral operations are prompting utilities to overhaul aging control systems in favor of modular, scalable, and highly adaptable solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $13.6 Billion |

| CAGR | 6.1% |

The hardware segment is expected to maintain robust growth with a projected CAGR of 6% through 2034. Ongoing upgrades in thermal and nuclear power facilities, along with the commissioning of new plants, are fueling the demand for precision control hardware that meets evolving regulatory standards. Natural gas power plants are also leaning heavily on integrated control systems to manage turbines, optimize load response, and curb emissions, especially with the accelerating deployment of combined cycle plants.

The natural gas power plant control system segment is poised to grow at a CAGR of 6% through 2034, supported by the rising popularity of combined cycle plants that pair gas and steam turbines to maximize efficiency and lower carbon emissions. These sophisticated facilities demand high-performance control solutions capable of managing complex operations from combustion tuning to heat recovery and emissions control, ensuring peak performance under dynamic load conditions. The growing preference for natural gas as a transitional fuel is further boosting infrastructure investments across key markets.

The United States Power Plant Control System Market reached USD 1.2 billion in 2024, backed by aggressive initiatives to modernize the country's aging energy grid. A surge in distributed energy resources, renewable generation, and demand for smarter grids is driving heavy investment in advanced automation and real-time control technologies at both federal and state levels.

Key players active in the Global Power Plant Control System Market include ABB, Siemens Energy, Schneider Electric, Mitsubishi Heavy Industries, Emerson Electric, Rockwell Automation, Yokogawa, Hitachi Energy, GE Vernova, WAGO, and others. Companies are focusing on continuous innovation, AI-driven automation, and strategic partnerships with utilities to expand their market presence. Modular designs, enhanced HMI interfaces, strong cybersecurity features, remote diagnostics, and full lifecycle services are becoming critical for vendors to stay competitive and meet evolving market demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Size and Forecast, By Solution, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Supervisory Control & Data Acquisition (SCADA)

- 6.3 Distributed Control System (DCS)

- 6.4 Programmable Logic Controller (PLC)

- 6.5 Plant Asset Management (PAM)

- 6.6 Plant Lifecycle Management (PLM)

Chapter 7 Market Size and Forecast, By Plant Type, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Coal

- 7.3 Natural gas

- 7.4 Nuclear

- 7.5 Hydroelectric

- 7.6 Renewable

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bachmann electronic

- 9.3 Emerson Electric

- 9.4 GE Vernova

- 9.5 Hitachi Energy

- 9.6 Ingeteam

- 9.7 Meteocontrol

- 9.8 Mitsubishi Heavy Industries

- 9.9 Motorola Solutions

- 9.10 Nexus Integra

- 9.11 OMRON Corporation

- 9.12 Petrotech

- 9.13 Rockwell Automation

- 9.14 Schneider Electric

- 9.15 Siemens Energy

- 9.16 Toshiba Energy Systems & Solutions Corporation

- 9.17 Valmet

- 9.18 WAGO

- 9.19 Yokogawa

电厂控制系统市场:依组件、自动化程度、安装类型、电厂规模、电厂类型及应用划分-2026-2030年全球市场预测核能发电数位化仪表与控制系统市场(按组件、功能模组、运作类型、部署模式、安全等级和生命週期阶段划分),全球预测(2026-2032)

电厂控制系统市场:依组件、自动化程度、安装类型、电厂规模、电厂类型及应用划分-2026-2030年全球市场预测核能发电数位化仪表与控制系统市场(按组件、功能模组、运作类型、部署模式、安全等级和生命週期阶段划分),全球预测(2026-2032) 2026年全球电厂控制系统市场报告

2026年全球电厂控制系统市场报告 电厂控制系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、组件、最终用户、应用、地区和竞争格局划分),2021-2031年

电厂控制系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、组件、最终用户、应用、地区和竞争格局划分),2021-2031年 发电厂控制系统市场,按解决方案类型、按应用、按组件、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

发电厂控制系统市场,按解决方案类型、按应用、按组件、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测