|

市场调查报告书

商品编码

1740880

光子积体电路 (PIC) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Photonic Integrated Circuit (PIC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

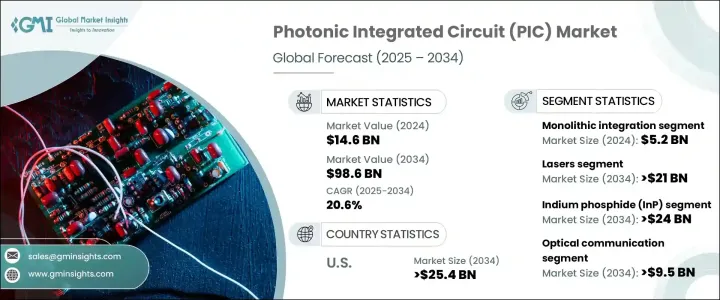

2024年,全球光子积体电路市场规模达146亿美元,预计2034年将以20.6%的复合年增长率成长,达到986亿美元。人工智慧 (AI) 和机器学习 (ML) 应用的爆炸性成长,尤其是在资料中心领域,持续推动市场扩张。高效能运算需求飙升至新高,传统电子元件的限制也逐渐显现。光子电路凭藉着卓越的频宽和能源效率,已成为满足这些新一代运算需求的理想解决方案。全球各国政府、科技公司和研究机构正在加大对光子学研发的投资,并意识到这项技术将在各行各业发挥的变革性作用。

在电信等领域,光子学正在实现更快的资料传输,并为超高效的网路系统奠定基础。在医疗保健领域,基于光子学的影像和诊断创新正在重塑病患照护和临床工作流程。人们对 5G 网路、量子运算、自动驾驶汽车和光学感测的日益关注,进一步拓宽了市场的应用格局,增强了全球对光子创新的推动。随着各行各业追求更快、更可靠、更节能的系统,光子装置 (PIC) 正处于技术发展的核心,为企业和消费者开启新的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 146亿美元 |

| 预测值 | 986亿美元 |

| 复合年增长率 | 20.6% |

光子积体电路市场按整合类型细分为单晶片整合、混合整合和模组整合。单晶片整合市场规模在2024年达到52亿美元,它能够将所有光子元件整合到磷化铟(InP)等单一基板上,从而推动产业重大进步。这种方法大幅降低了互连损耗,提升了系统整体效能,并降低了生产成本。单晶片PIC对于高速收发器和光处理器尤其重要,能够提供电信和资料通讯等产业所需的紧凑、可扩展的解决方案。随着对高效生产、最小空间要求和可靠高速性能的日益重视,预计单晶片整合将在预测期内保持强劲发展势头。

从组件角度来看,市场包括调製器、雷射、光电探测器、復用器/解復用器、波导、衰减器、光放大器和其他关键部件。其中,雷射器发挥关键作用,预计到2034年将创造210亿美元的市场价值。基于磷化铟(InP)的雷射在光子积体电路中正变得不可或缺,为高速光通讯、光纤和光达系统提供必要的相干光源。其无缝整合能力增强了系统的可扩展性和效能,帮助各行各业满足日益增长的高频宽应用需求。

美国光子积体电路市场预计在2034年达到254亿美元,这得益于强大的科技巨头生态系统、研究项目以及对硅光子学的深度投资。英特尔、思科和Rockley Photonics等公司正在引领光通讯、资料中心和医疗诊断领域的创新。国家光子学计画(NPI)等倡议正在进一步加速国防、航太和生物医学应用等关键领域的商业化。

全球光子积体电路产业的领导者包括英特尔公司、思科系统公司、英飞朗公司和博通公司。为了巩固市场地位,这些公司正在扩大产品组合,与科技公司和研究机构建立策略合作伙伴关係,并大力投资研发,以提升光子学在人工智慧和电信网路中的效能。许多公司也正在收购规模较小、专业的光子技术公司,以加快创新步伐,并在新兴市场中占据竞争优势。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 资料中心扩展和高速通讯需求

- 硅光子学的进展

- 在医疗保健和生物感测领域的应用日益广泛

- 对 5G 和下一代电信基础设施的需求

- 政府和国防为光子学研发提供资金

- 产业陷阱与挑战

- 初始资本投资高且製造复杂

- PIC平台缺乏标准化

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按整合类型,2021 - 2034 年

- 单晶片集成

- 混合集成

- 模组集成

第六章:市场估计与预测:按组件,2021 - 2034 年

- 雷射器

- 调节剂

- 光电探测器

- 波导

- 多工器/多路分解器

- 衰减器

- 光放大器

- 其他的

第七章:市场估计与预测:依资料,2021 - 2034 年

- 磷化铟(InP)

- 绝缘体上硅(SOI)

- 硅光子学

- 砷化镓(GaAs)

- 铌酸锂

- 其他的

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 光通讯

- 感测

- 生物光子学

- 光讯号处理

- 量子计算

- 其他的

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 电信

- 资料中心

- 消费性电子产品

- 医疗保健与生命科学

- 国防与航太

- 工业的

- 汽车

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第 11 章:公司简介

- Intel Corporation

- Infinera Corporation

- Cisco Systems, Inc.

- Broadcom Inc.

- NeoPhotonics Corporation

- Lumentum Holdings Inc.

- II-VI Incorporated

- Coherent Corp.

- Acacia Communications

- Enablence Technologies Inc.

- HPE

- Mellanox Technologies

- Luxtera

- Rockley Photonics

- POET Technologies Inc.

- Ciena Corporation

- Alcatel-Lucent

- Fujitsu Optical Components

- IBM Corporation

- STMicroelectronics

- Hewlett Packard Labs

- TE Connectivity

- VLC Photonics (a Hitachi Group company)

- Effect Photonics

The Global Photonic Integrated Circuit Market was valued at USD 14.6 billion in 2024 and is estimated to grow at a CAGR of 20.6% to reach USD 98.6 billion by 2034. The explosive growth of artificial intelligence (AI) and machine learning (ML) applications, especially across data centers, continues to fuel market expansion. High-performance computing demands have surged to new heights, exposing the limitations of traditional electronic components. Photonic circuits, offering superior bandwidth and energy efficiency, have emerged as the ideal solution to address these next-generation computing requirements. Governments, tech companies, and research institutions worldwide are ramping up investments in photonics research and development, recognizing the transformative role this technology will play across industries.

In sectors like telecommunications, photonics is enabling faster data transmission and building the foundation for ultra-efficient networking systems. In healthcare, photonics-based innovations in imaging and diagnostics are reshaping patient care and clinical workflows. The growing focus on 5G networks, quantum computing, autonomous vehicles, and optical sensing is further broadening the market's application landscape, strengthening the global push toward photonic innovation. As industries aim for faster, more reliable, and energy-efficient systems, PICs are positioned at the heart of technological evolution, unlocking new possibilities for businesses and consumers alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.6 billion |

| Forecast Value | $98.6 billion |

| CAGR | 20.6% |

The photonic integrated circuit market is segmented by integration type into monolithic, hybrid, and module integration. Monolithic integration, valued at USD 5.2 billion in 2024, is driving major industry advancements by enabling the integration of all photonic components onto a single substrate like Indium Phosphide (InP). This approach drastically reduces interconnect losses, boosts overall system performance, and lowers production costs. Monolithic PICs are especially crucial for high-speed transceivers and optical processors, delivering the compact, scalable solutions demanded by industries such as telecommunications and data communications. With the growing emphasis on efficient production, minimal space requirements, and reliable high-speed performance, monolithic integration is expected to maintain strong momentum through the forecast period.

Component-wise, the market includes modulators, lasers, photodetectors, multiplexers/demultiplexers, waveguides, attenuators, optical amplifiers, and other critical parts. Among these, lasers play a pivotal role and are expected to generate USD 21 billion by 2034. Lasers based on InP are becoming indispensable across photonic integrated circuits, offering essential coherent light sources needed for high-speed optical communications, fiber optics, and LIDAR systems. Their seamless integration capabilities enhance system scalability and performance, helping industries meet the increasing demand for high-bandwidth applications.

The U.S. photonic integrated circuit market is on track to reach USD 25.4 billion by 2034, powered by a strong ecosystem of technology giants, research initiatives, and deep investments in silicon photonics. Companies like Intel, Cisco, and Rockley Photonics are leading innovations across optical communication, data centers, and healthcare diagnostics. Initiatives like the National Photonics Initiative (NPI) are further accelerating commercialization efforts in critical sectors such as defense, aerospace, and biomedical applications.

Leading players in the global photonic integrated circuit industry include Intel Corporation, Cisco Systems, Inc., Infinera Corporation, and Broadcom Inc. To strengthen their market presence, these companies are expanding product portfolios, forming strategic partnerships with tech firms and research bodies, and investing heavily in RandD to push photonics performance in AI and telecom networks. Many are also acquiring smaller, specialized photonic technology firms to fast-track innovation and secure a competitive edge in emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Data center expansion & high speed communication demand

- 3.3.1.2 Advancements in silicon photonics

- 3.3.1.3 Growing use in healthcare & biosensing

- 3.3.1.4 Demand for 5g & next-gen telecom infrastructure

- 3.3.1.5 Government & defense funding for photonics R&D

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial capital investment & fabrication complexity

- 3.3.2.2 Lack of standardization across PIC platforms

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Integration Type, 2021 - 2034 (USD Million and Units)

- 5.1 Monolithic integration

- 5.2 Hybrid integration

- 5.3 Module integration

Chapter 6 Market estimates & forecast, By Component, 2021 - 2034 (USD Million and Units)

- 6.1 Lasers

- 6.2 Modulators

- 6.3 Photodetectors

- 6.4 Waveguides

- 6.5 Multiplexers/demultiplexers

- 6.6 Attenuators

- 6.7 Optical amplifiers

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million and Units)

- 7.1 Indium phosphide (InP)

- 7.2 Silicon-on-insulator (SOI)

- 7.3 Silicon photonics

- 7.4 Gallium arsenide (GaAs)

- 7.5 Lithium niobate

- 7.6 Others

Chapter 8 Market estimates & forecast, By Application, 2021 - 2034 (USD Million and Units)

- 8.1 Optical communication

- 8.2 Sensing

- 8.3 Biophotonics

- 8.4 Optical signal processing

- 8.5 Quantum computing

- 8.6 Others

Chapter 9 Market estimates & forecast, By End Use, 2021 - 2034 (USD Million and Units)

- 9.1 Telecommunications

- 9.2 Data centers

- 9.3 Consumer electronics

- 9.4 Healthcare & life sciences

- 9.5 Defense & aerospace

- 9.6 Industrial

- 9.7 Automotive

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Intel Corporation

- 11.2 Infinera Corporation

- 11.3 Cisco Systems, Inc.

- 11.4 Broadcom Inc.

- 11.5 NeoPhotonics Corporation

- 11.6 Lumentum Holdings Inc.

- 11.7 II-VI Incorporated

- 11.8 Coherent Corp.

- 11.9 Acacia Communications

- 11.10 Enablence Technologies Inc.

- 11.11 HPE

- 11.12 Mellanox Technologies

- 11.13 Luxtera

- 11.14 Rockley Photonics

- 11.15 POET Technologies Inc.

- 11.16 Ciena Corporation

- 11.17 Alcatel-Lucent

- 11.18 Fujitsu Optical Components

- 11.19 IBM Corporation

- 11.20 STMicroelectronics

- 11.21 Hewlett Packard Labs

- 11.22 TE Connectivity

- 11.23 VLC Photonics (a Hitachi Group company)

- 11.24 Effect Photonics