|

市场调查报告书

商品编码

1740940

Cerakote(陶瓷基涂层)市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cerakote (Ceramic-Based Coating) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

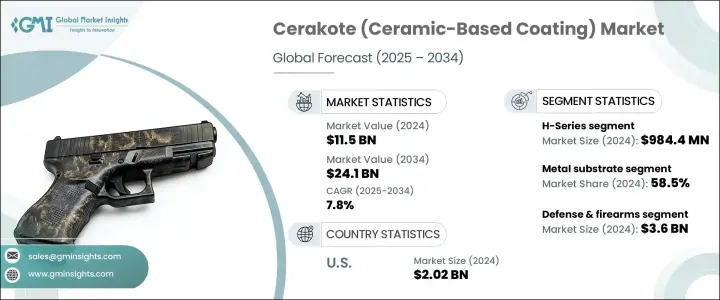

2024年,全球Cerakote(陶瓷基涂层)市场价值达115亿美元,预计到2034年将以7.8%的复合年增长率成长,达到241亿美元。由于各行各业对涂层的需求日益增长,市场正经历强劲增长。这些涂层不仅需要满足技术标准,还需要提供客製化功能。这种成长主要源自于对兼具耐用性、耐腐蚀性和美观性的高性能涂层日益增长的需求。随着製造流程日益专业化,符合行业特定要求和环境适应性的陶瓷基涂层的应用日益广泛。 Cerakote兼具功能性与美观性,使其成为各终端应用领域的首选。其中,由于消费者群体的不断扩大以及对耐用涂层(这些涂层可在设备和配件上提供耐热性、耐磨性和高端饰面)的需求不断增长,电子产品市场正经历显着增长。这些特性使得 Cerakote 成为在严苛条件下涂覆基材的顶级解决方案。

H系列在该产品领域处于领先地位,2024年价值达9.844亿美元。预计该系列在2025年至2034年期间的复合年增长率将达到8.4%。凭藉其强大的耐化学性、防腐蚀性和耐磨性,它仍然是商业上最成功的产品系列。其有效性已在众多兼顾性能和外观的工业应用中得到证实。市场还涵盖其他产品系列,例如C系列、Elite系列、Glacier系列和Clear Coats系列,每个系列都根据不同的应用需求,开发以满足特定的性能基准。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 115亿美元 |

| 预测值 | 241亿美元 |

| 复合年增长率 | 7.8% |

Cerakote涂料根据基材相容性进行分类,主要材料类别包括金属、聚合物和塑胶、复合材料以及木材。 2024年,金属在该领域占据主导地位,占据全球市场份额的58.5%。这种主导地位源自于金属零件在环境暴露、耐磨性和使用寿命至关重要的行业中的广泛使用。该涂料对黑色金属和有色金属均具有优异的附着力,这使其在高应力环境中更具吸引力。 Cerakote的分子键结能力在製造业和重型应用中增强金属性能方面发挥重要作用。

聚合物和塑胶通常采用 C 系列涂料,该涂料在室温下固化,以保持基材的结构完整性。相较之下,木质基材则受益于该涂料的防潮和防刮擦性能,尤其是在註重美观且注重表面设计的应用中。这些涂料提供的不仅是保护,它们还能实现创意定制,而不会牺牲材料的耐久性。

就终端应用产业而言,国防和枪械产业成为最大的贡献者,2024 年市场价值达 36 亿美元,预计到 2034 年复合年增长率为 6.7%。该领域占据了整体市场的 31%,这得益于对在极端条件下性能可靠的涂层的需求不断增长。 Cerakote 的热稳定性和耐磨性使其特别适用于战术装备和武器,因为这些装备的性能和表面完整性至关重要。

陶瓷涂层市场的应用方法主要分为喷涂、热固化和风干。喷涂因其高效、均匀、薄层涂层的优势而继续保持领先地位,这对于注重外观和光滑表面的应用至关重要。热固化主要用于对耐久性和耐化学性有较高要求的应用,而风干则较适用于热敏性基材,例如塑胶、复合材料和木材。

2024年,美国占据了全球陶瓷市场相当大的份额,估值达20.2亿美元。预计2025年至2034年期间,美国国内陶瓷市场将以7.8%的复合年增长率成长。汽车、军事和消费品等高性能产业的需求成长持续推动陶瓷市场的成长。客製化的美观饰面和更长的组件生命週期是市场扩张的关键驱动力。对耐用涂层和行业标准的监管意识的提高也推动了陶瓷基解决方案的采用。

随着领先製造商大力投资创新、策略合作和全球分销网络的扩张,竞争环境日益激烈。顶级公司专注于优化生产技术,保持产品品质的一致性,并加强其在OEM和售后市场管道的影响力。主要参与者也优先考虑认证、内部测试能力和技术服务,以建立品牌信任和客户忠诚度。随着对高性能和美观涂料的需求不断增长,製造商正竞相透过先进的研发和製程开发来满足客户期望。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 主要出口国

- 主要进口国

註:以上贸易统计仅针对重点国家。

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 枪械和国防对高性能涂料的需求不断增长。

- 增加汽车客製化和售后服务。

- 轻质、耐高温零件在航太的应用日益广泛。

- 工业设备高温涂料需求激增

- 产业陷阱与挑战

- 与传统涂料相比,应用和固化成本较高。

- 品牌供应有限。

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- H系列

- C系列

- 精英系列

- 冰川系列

- 透明涂层

第六章:市场估计与预测:依基材相容性,2021-2034

- 主要趋势

- 金属

- 钢

- 铝

- 钛

- 聚合物和塑料

- 复合材料

- 木头

第七章:市场估计与预测:按应用产业,2021-2034 年

- 主要趋势

- 防御与枪支

- 汽车与运输

- 航太航太

- 消费性电子产品

- 医疗器材

- 工业设备

- 体育和户外用品

第八章:市场估计与预测:依应用方法,2021-2034 年

- 主要趋势

- 喷涂

- 热固化

- 空气干燥

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Arrow Finishing

- Cerakote

- KECO Coatings

- KOTEC Ceramic Coatings

- MSP Manufacturing

- Mueller Coatings

- NIC Industries

- Spectrum Coating

- Sun Coating Company

- Tanury Industries

The Global Cerakote (Ceramic-Based Coating) Market was valued at USD 11.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 24.1 billion by 2034. The market is experiencing robust growth due to the increasing demand for coatings that not only fulfill technical standards but also deliver tailored functionality across different industries. This surge is primarily driven by the rising need for high-performance coatings that offer durability, corrosion resistance, and aesthetic appeal. As manufacturing processes become more specialized, there's growing adoption of ceramic-based coatings that align with industry-specific requirements and environmental resilience. Cerakote's ability to combine functionality with visual sophistication makes it a preferred choice across various end-use sectors. Among these, electronics are witnessing notable traction due to the expanding consumer base and the growing demand for durable coatings that offer heat resistance, wear protection, and a premium finish on devices and accessories. These qualities have positioned cerakote as a top-tier solution for coating substrates exposed to demanding conditions.

The H-Series led the product segment and was valued at USD 984.4 million in 2024. This series is anticipated to witness a CAGR of 8.4% between 2025 and 2034. It remains the most commercially successful product line due to its strong combination of chemical resistance, corrosion protection, and wear durability. Its effectiveness has proven reliable across numerous industrial uses where both performance and appearance matter. The market comprises other product lines as well, such as the C-Series, Elite Series, Glacier Series, and Clear Coats, each developed to meet specific performance benchmarks in line with various application needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $24.1 Billion |

| CAGR | 7.8% |

Cerakote coatings are classified based on substrate compatibility, with metals, polymers & plastics, composites, and wood serving as the primary material categories. Metals dominated the segment in 2024, accounting for 58.5% of the global market share. This dominance stems from the widespread use of metallic components in industries where environmental exposure, wear resistance, and longevity are essential. The coating's superior adhesion to both ferrous and non-ferrous metals adds to its attractiveness in high-stress environments. Cerakote's molecular bonding capability plays a significant role in reinforcing metals used in manufacturing and heavy-duty applications.

Polymers and plastics are typically coated with C-Series formulations, which cure at ambient temperatures to maintain the structural integrity of the base materials. In contrast, wood substrates benefit from the coating's moisture resistance and scratch protection, especially in aesthetic-focused uses where surface design matters. These coatings offer more than just protection; they allow for creative customization without sacrificing material durability.

In terms of end-use industries, the defense and firearms sector emerged as the largest contributor, with a market value of USD 3.6 billion in 2024 and an expected CAGR of 6.7% through 2034. This segment represented 31% of the overall market, driven by growing demand for coatings that perform reliably under extreme conditions. The thermal stability and abrasion resistance of cerakote make it particularly suitable for tactical equipment and weaponry, where performance and surface integrity are critical.

Application methods in the cerakote market are primarily segmented into spray coating, heat curing, and air drying. Spray coating continues to lead due to its efficiency in producing even, thin layers, which is critical for applications where visual appeal and smooth finishes are essential. Heat curing is mainly applied in situations that demand peak durability and chemical resistance, whereas air drying is more appropriate for heat-sensitive substrates, including plastics, composites, and wood.

In 2024, the United States held a significant share of the global market, with a valuation of USD 2.02 billion. The domestic market is forecasted to grow at a 7.8% CAGR between 2025 and 2034. Increased demand from high-performance industries such as automotive, military, and consumer goods continues to boost growth. Customized aesthetic finishes and extended component lifecycles are key drivers for market expansion. Regulatory awareness around durable coatings and industry standards has also led to increased adoption of ceramic-based solutions.

The competitive environment is intensifying as leading manufacturers invest heavily in innovation, strategic collaborations, and expansion of global distribution networks. Top-tier companies are focusing on optimizing production techniques, maintaining consistency in product quality, and strengthening their presence across OEM and aftermarket channels. Key players are also prioritizing certifications, in-house testing capabilities, and technical services to build brand trust and customer loyalty. As demand for high-performance and visually appealing coatings grows, manufacturers are racing to meet expectations through advanced R&D and process development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for high-performance coatings in firearms and defense.

- 3.7.1.2 Increasing automotive customization and aftermarket services.

- 3.7.1.3 Growing use in aerospace for lightweight, high-heat components.

- 3.7.1.4 Surge in demand for high-temperature coatings in industrial equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High application and curing costs compared to traditional coatings.

- 3.7.2.2 Limited brand availability.

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 H-series

- 5.3 C-series

- 5.4 Elite series

- 5.5 Glacier series

- 5.6 Clear coats

Chapter 6 Market Estimates & Forecast, By Substrate Compatibility, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Metals

- 6.2.1 Steel

- 6.2.2 Aluminum

- 6.2.3 Titanium

- 6.3 Polymers & plastics

- 6.4 Composites

- 6.5 Wood

Chapter 7 Market Estimates & Forecast, By Application Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Defense & firearms

- 7.3 Automotive & transportation

- 7.4 Aerospace & aviation

- 7.5 Consumer electronics

- 7.6 Medical devices

- 7.7 Industrial equipment

- 7.8 Sporting & outdoor goods

Chapter 8 Market Estimates & Forecast, By Application Method, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Spray coating

- 8.3 Heat curing

- 8.4 Air drying

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Arrow Finishing

- 10.2 Cerakote

- 10.3 KECO Coatings

- 10.4 KOTEC Ceramic Coatings

- 10.5 MSP Manufacturing

- 10.6 Mueller Coatings

- 10.7 NIC Industries

- 10.8 Spectrum Coating

- 10.9 Sun Coating Company

- 10.10 Tanury Industries

LATP涂层隔膜市场按应用、隔膜结构、涂层材料和分销管道划分,全球预测,2026-2032年等离子喷涂陶瓷涂层材料市场:依材料类型、应用、製程类型及最终用途产业划分,全球预测(2026-2032)高纯度、高密度氧化钇市场依应用、终端用户产业、产品等级、形态、销售管道及合成製程划分,全球预测,2026-2032年全球地下搪瓷板市场(按产品类型、安装类型、应用、分销管道和最终用户产业划分)预测(2026-2032年)无机陶瓷涂料市场按树脂类型、技术、产品形式、固化方法、终端用户产业和应用划分-2026-2032年全球预测水性陶瓷涂料市场:依树脂类型、技术、应用、终端用户产业及通路划分-2026-2032年全球预测等离子体耐受氧化钇涂层市场:按涂层类型、沉积方法、应用、最终用户和分销管道划分 - 全球预测(2026-2032 年)陶瓷涂层市场按产品类型、技术、价格范围、应用和分销管道划分,全球预测(2026-2032年)

LATP涂层隔膜市场按应用、隔膜结构、涂层材料和分销管道划分,全球预测,2026-2032年等离子喷涂陶瓷涂层材料市场:依材料类型、应用、製程类型及最终用途产业划分,全球预测(2026-2032)高纯度、高密度氧化钇市场依应用、终端用户产业、产品等级、形态、销售管道及合成製程划分,全球预测,2026-2032年全球地下搪瓷板市场(按产品类型、安装类型、应用、分销管道和最终用户产业划分)预测(2026-2032年)无机陶瓷涂料市场按树脂类型、技术、产品形式、固化方法、终端用户产业和应用划分-2026-2032年全球预测水性陶瓷涂料市场:依树脂类型、技术、应用、终端用户产业及通路划分-2026-2032年全球预测等离子体耐受氧化钇涂层市场:按涂层类型、沉积方法、应用、最终用户和分销管道划分 - 全球预测(2026-2032 年)陶瓷涂层市场按产品类型、技术、价格范围、应用和分销管道划分,全球预测(2026-2032年) 陶瓷涂层市场-全球产业规模、份额、趋势、机会及预测,依产品、应用、技术、地区及竞争格局划分,2020-2030年预测

陶瓷涂层市场-全球产业规模、份额、趋势、机会及预测,依产品、应用、技术、地区及竞争格局划分,2020-2030年预测 陶瓷涂层市场-2025-2030年预测

陶瓷涂层市场-2025-2030年预测